Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

You need all the control over your life you can get, once you hang your hat after work. The ideal retirement is that one event in life that allows you to be yourself after you decide not to work. To have such a retirement, your investments play the most significant role. Smart investors consider buying the best retirement plans to fund their retirement dreams.

Plan your estate to ensure your assets are passed on smoothly and legally.

Some other investors also consider putting their money in a mix of assets to enjoy significant returns. While some othersother consider playing it safe by parking their money in government schemes. So, where can you invest your money for a great and comfortable retirementretired life?

Here are five investments you should have in your retirement investment portfolio:

Retirement is not just about stopping work. It is also about sustaining the lifestyle you’ve worked hard to build. The right investments can help turn your savings into a dependable income and safeguard your future against rising costs.

Guaranteed Investment Plans

These are some of the safest long-term investment plans in the country. If you want to preserve your financial wealth for a long time against both inflation and taxes, these are the plans you should look for.

Such plans are particularly useful when you want to avoid the unpredictability of markets during your retirement years. They also offer peace of mind for those who prefer predictability over high-risk, high-reward investments.

These are the features and benefits of guaranteed investment plans:

Fixed maturity value: Know exactly how much you'll get at the end

Long-term option: Usually 10-20 years tenure for optimal returns

Stable income: Useful for planning retirement cash flow

Risk-free: Not impacted by market volatility

Pension Plans

Pension plans help you convert your wealth into a regular and reliable stream of income. They are a key component of a retirement strategy, especially when you're looking for predictable, lifelong payouts. Thus, they should be an inseparable part of your retirement plan.

You can invest a lump sum amount and choose when the income should begin, making them flexible based on your retirement timeline.

Types of Pension Plans:

Immediate Annuity: Income starts at the end of the income period. For example, if you chose the monthly income mode, your income would start at the end of the first month after the investment.

Deferred Annuity: You can defer the income for a few years. For example, you can invest the lump sum money at the age of 55 and want the income to start at 60. Thus, the first payment will arrive after 5 years and one month in the case of the monthly mode.

Pension 4life by Canara HSBC Life Insurance is an investment plan that allows you to invest the lump sum money received from other long-term investment plans to create a pension income. You can invest in the following options depending on when you want your income to start:

1. Guaranteed Investment Plans

Guaranteed investment plans are some of the safest long-term investment plans in the country. If you want to preserve your financial wealth for a long time against both inflation and taxes these are the plans you should look for.

Here are two guaranteed investment plans from Canara HSBC Life Insurance for you:

2. Pension Plans

Pension plans help you convert your wealth into regular and reliable stream of income. Thus, they are an inseparable part of your retirement plan.

Pension 4life: This is an investment plan where you can invest the lump sum money received from other long-term investment plans to create pension income. You can invest in the following options depending on when you want your income to start:

Immediate Annuity: Income starts at the end of the income period. For example, if you chose monthly income mode, your income would start at the end of the first month after investment.

Deferred Annuity: You can defer the income for a few years. For example, you can invest the lump-sum money at the age of 55 and want the income to start at 60. Thus, the first payment will arrive after 5 years and one month in the case of monthly mode.

3. Fixed Deposits:

Fixed deposits are one of the most popular and perhaps one of the easiest to use investment options. Especially if you have little time to look at where your money is going. Fixed deposits offer the following features, benefits, and limitations to your money:

Fixed Rate of Return: Once you deposit the money the rate of interest or growth rate of your money is set and will remain unchanged for the entire deposit period.

Defined Tenure: The deposit’s tenure is defined clearly. So, you can plan your FDs in ways to either enjoy a long-term growth or regular income.

High Safety: Fixed deposits of scheduled national banks and Post Office are insured up to Rs. 5 lakhs.

Good Liquidity: You can break the FDs any time in case you need money in emergencies. However, you end up losing a part of the interest.

Online Start-Stop Renew: If you operate your savings account online opening, closing, and renewing fixed deposits will be a matter of just a few clicks.

Taxation: Fixed deposit interest is taxable in the year it accrues and is added to your taxable income.

4. National Pension Scheme

This is a perfect retirement investment solution that you must have in your retirement portfolio. The major advantage that NPS has over other investments is that you can keep increasing your regular savings in NPS along with your income growth.

Thus, your retirement savings keep up with your income growth without having to buy a new plan now and then. However, the maturity value of NPS is not entirely tax-exempt, unless you follow the withdrawal rules:

40% must be invested for pension in an annuity plan

60% of the maturity proceeds you can withdraw tax-free

You can also continue the NPS account up to the age of 70

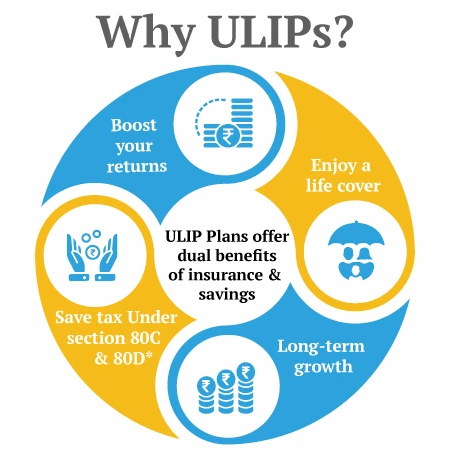

5. Unit Linked Insurance Plans (ULIPs)

These are a versatile investment option from the life insurer’s portfolio. This is one investment plan which offers a complete portfolio management platform for your investment. You can invest in multiple funds with different risk-return profiles and manage your portfolio like a professional. As a young investor, when you start investing for a long-term goal such as retirement, you want to invest aggressively to maximise growth. However, as time passes, you need to reduce your investment risks so that you can preserve the growth.

A ULIP is perfect for a dynamic risk investment for the following reasons:

Invest different types of fund options based on your comfort with returns and stability.

Switch between these fund options during the policy term without incurring capital gains tax.

Invest additional money if your annual premium is less than 10% of the sum assured or after your premium payment term in the policy.

Smart Investment Strategies within ULIPs

ULIPs go beyond traditional investments by offering strategic tools that automate, protect, and optimise your retirement corpus.

Automate portfolio management

Managing your investments manually can be overwhelming, especially over long periods. Some retirement plans offer built-in strategies to help you adjust and balance your funds automatically based on your chosen preferences.

Maintain risk-return profile: You can fix a preferred allocation between different types of fund options at the beginning of your investment period, and the plan will rebalance your funds regularly.

Dynamic Shifts: For example, you want to maintain a 50:50 ratio of two types of options, one focused on growth and the other on stability. The plan will move your money between them as needed. These automatic adjustments ensure that your allocation remains aligned with your original choice, without requiring manual intervention.

Stay consistent: This feature helps you stay committed to your long-term investment goals, even when you're not actively managing your plan.

Gradual Risk Reduction Over Time

ULIPs allow you to reduce exposure to high-risk assets as you near retirement.

Lower the risk with time: You can also choose a strategy where the growth of your investments by gradually shifting it to more stable fund options. .

For example, you want to safeguard your returns that exceed a certain percentage, say 5%, the plan can automatically move that portion to a more conservative fund. This helps in preserving your gains while reducing the risk of future fluctuations.

Preserve your capital: Imagine investing for 20 or 30 years. Your portfolio growth will be huge, provided you have been consistent with your investments. To do this, some plans allow you to gradually shift your funds to more stable options during the final few years, helping reduce potential risks and secure your returns before retirement.

Bonus Additions: Staying invested over the long term comes with extra perks. Additional units added to your portfolio for investing over a long period. More additions for a longer period. Additional units for staying invested for more than 10 years.

Tax-Free Withdrawals

ULIP plans carry a mandatory lock-in period of five years. But, after five years any withdrawals from the plan are completely tax-free. If you have bought a ULIP plan after 1st Feb 2021, complete tax exemption will only apply to the withdrawals if your total annual investments in the plan have been Rs. 2.5 lakhs or less. If the premium crosses this limit, the maturity amount will be taxed as capital gains from FY 2026-27 onwards.

The tax-free withdrawals are very convenient when you are close to retirement or after retirement.

You can ensure a financially independent life post-retirement by investing appropriately in a couple of these plans. Also, these investments would offer tax relief which means additional savings. Remember that every investment plan will allow you specific benefits. So, invest as per your needs.

Secure Your Retirement with Guaranteed Income Plans

Enter OTP

An OTP has been sent to your mobile number

Didn’t receive OTP?

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder as on

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Sorry ! No records Found

. Please use this ID for all future communications regarding this concern.

Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Conclusion

Retirement planning involves shaping an investment approach that aligns with your future lifestyle goals, rather than simply accumulating savings. Whether you prefer fixed returns, regular income, or flexible long-term options, each of these plans can play a role in securing your post-retirement life.

Start early, stay consistent, and choose investments that align with your comfort level with risk and income needs. With the right approach, you can establish a solid financial foundation and experience the freedom that retirement should truly provide.

Glossary

Diversified Investment: Way to reduce risk and increase profit is to diversify investment by putting funds in different asset classes.

Assets under management (AUM): The total value of assets that an investment company manages for its clients.

National Pension Scheme (NPS): A market-linked, voluntary, and tax-efficient scheme that helps you to save for your future.

Retirement Portfolio: Sum of all your investments in various accounts, which is to provide you with a stable income after retirement.

ETF (Exchange-Traded Fund): Pooling of funds in one place from where investors can easily invest in stocks, bonds, or other assets.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.