Written by : Knowledge Centre Team

2025-11-18

1207 Views

11 minutes read

Share

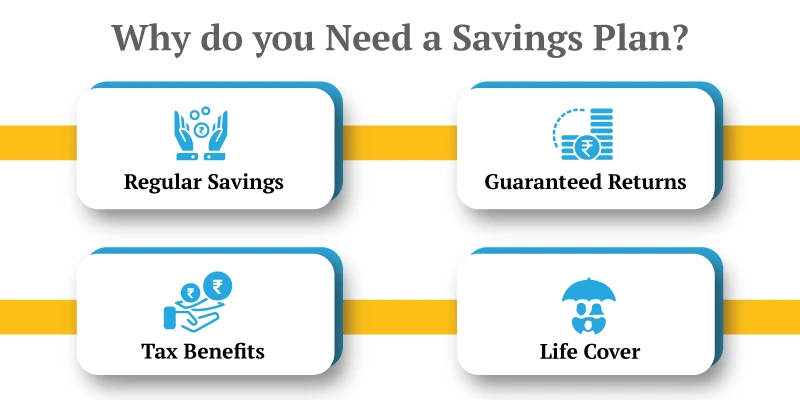

Savings plans are a great idea to secure the future of your family. Throughout the years in which you earn, preferably at the peak of your career, you try putting aside a certain amount of money and pay premiums for a savings plan so that you and your family can enjoy the benefits after the maturity period is reached.

With the rising rates of inflation and increasing costs of healthcare, education and lifestyle, this plan ensures your family receives a fixed amount of allowance after your death. Therefore, a guaranteed savings plan is essential for the breadwinner of any family so that they will be well-off in your absence.

But with the diversification of the demographic that goes for savings plans these days, insurance companies and banks have rolled a variety of options. It may be difficult for an average Indian to discern the differences between all of these savings plans and determine the best for you.

Canara HSBC Life Insurance offers various guaranteed savings plans from which you can pick and choose the best according to your economic circumstances. The ideal savings plan should help you grow your investment through regular investments through disciplined premiums paid throughout a specific period. You will be eligible for certain benefits and allowances until the policy’s termination.

Let us take a look at the variety of guaranteed savings plans offered by Canara HSBC :

This unit-linked individual life insurance savings plan is highly customizable, non-participating and provides complete control over all your savings and insurance needs. You can choose from three cover options – Life Option, Care Option and Century Option, which all cater to different needs. The century option will provide you with coverage for a hundred years. Additional benefits include:

Designed to boost savings, this plan combines investment and protection. There is also higher customizability, allowing you to modify the asset investment based on the current market conditions and your economic status. There is a choice between single, limited and regular premium payment options. To effectively manage risk, there are a variety of strategies for portfolio management.

The guaranteed savings plan allows you to save up for the future, especially for additional costs that may occur in your family’s posterity. This will allow you to pay off the premiums in a traditional, affordable payment set-up, ensuring an excellent assured sum at the end of your policy term.

This unit-linked insurance plan was created with the idea that wealth creation should go hand in hand with whole life coverage. Combining the idea of a century plan with a wealth-oriented savings plan will allow you to fulfil financial needs at various points of your life so that there is a stable income source after the policy period is over. Also, the premium paying mode can be changed anytime during the policy term. You can choose to invest in multiple investment funds whose equity exposure ranges from 0% to 100%:

The smart future income plan offers life coverage with an assured sum that is a hundred times the chosen monthly income, an income benefit that will be paid to the policyholder on a chosen monthly basis for the last fifteen years of the plan till the end of the policy term.

It also provides a maturity benefit, added with annual bonuses and a final bonus if the policyholder survives till maturity. Added benefits include a premium benefit to which you are entitled to if your sum assured is seven lakhs or more, as well as a loan facility that can help you with your liquidity needs, provided the policy has acquired a surrender value.

This unit-linked plan is for parents who want to secure a bright future for your child. With the increasing costs of education and possibilities of education in international universities, you may want to save up quite a large amount for your child’s future. This plan offers a comprehensive insurance cover that includes a sum assured on death and a premium funding in disability or untimely death.

This premium retirement plan allows parents to secure a death benefit for their descendants, where they will be paid the higher of the following:

There is also the additional option of choosing between five different investment funds based on your specific needs.

This plan involves a one-time investment that will ensure a lifetime of regular income for your loved ones. The sum assured on death will be the higher of ten times the annualized premium, the guaranteed sum assured on maturity or the absolute amount assured to be paid to death (which will be equal to sum assured). This plan is perfect for those who earn sporadically and want to secure an income for your child’s future – especially if you do not have a stable income in which case you can pay for disciplined premiums. The plan also offers a rebate on the payable premium if the assured sum is four lakhs or above, as well as a loan facility to meet your liquidity needs if you have reached the surrender value for your policy.

This plan offers a guarantee money back pay out at regular intervals as specified below, provided all premiums have been paid, along with a maturity benefit and a death benefit. Money back plans are one of the popular options for investors.

| Guaranteed Money Back payouts payable at the end of the Policy Year | Guaranteed Money Back payouts payable(as a Percentage of the Sum Assured) |

| 5th | 15% |

| 9th | 15% |

| 13th | 15% |

Once the payment of benefits has been concluded, the policy will be terminated. Additional advantages include a simple reversionary bonus that will be declared at the end of every financial year and is usually a percentage of the sum assured and a terminal bonus depending on the profits emerging from the company’s profit fund, paid at the maturity of the plan.

This plan provides a maturity benefit that will be 100% of sum assured for an endowment option or 70% of sum assured if you go for the money-back option. There will be a death benefit which will be the higher of either the 11 times the annualized premium, 105% of total premiums paid as on death date, the guaranteed sum assured on maturity or the absolute sum assured. There will also be an annualized premium payable in a year of your choice, exclusive of taxes, rider premiums of modal premium loadings (if any). This plan allows you to save large amounts of money quickly, hence the name.

The Canara HSBC Life Insurance offers many more plans and combinations of saving plans, allowing you to secure a future for your family. Signing up for a guaranteed savings plan is usually a lifelong commitment that will pay off towards the end, but you must choose one that will not add on to your family’s financial burdens if any.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.