2025-05-28

897 Views

4 minutes read

Share

We all dream of living a comfortable, worry-free life with the ones we love. And to ensure all you dreams and your family’s long-term wishes are fulfilled, you need to build a comprehensive financial planning portfolio. Choose from the various tax saving schemes options available to secure your family’s financial future, while earning you a significant tax deduction every year.

While you work hard to earn for your family all your life, making thoughtful investments can help you get tax benefits and save your money. Tax-saving plans and investment schemes are instrumental in effectively achieving your financial goals. Depending on your needs and financial capabilities, choose a mix of long-term and short-term financial instruments and save your money in different avenues to gain maximum returns. Consider factors like safety, liquidity, and returns. While you are at it, you can reduce your tax burden by choosing tax saving plans to claim tax deductions under section 80C or Section 80CCC of the Income Tax Act, 1961.

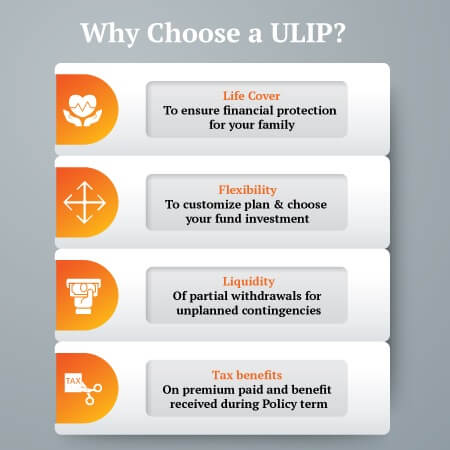

ULIPs are popular because they offer dual benefits of life insurance and investment. ULIP Plans have a lock-in of 5 years with a minimum premium amount that may vary but typically starts from as low as Rs. 5,000. The payouts under a ULIP, including the death benefits received as well as any partial withdrawals made from the policy are exempt from taxation under Section 10(10D) of the Income Tax Act subject to conditions provided therein.

An OTP has been sent to your mobile number

Sorry! No records Found

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

PPF is a government guaranteed investment option that provides tax benefits under section 80C of Income tax act , 1961 with fixed returns on minimum premium of Rs.500. PPF deposits have a lock-in period of 15 years and its interest rate is fixed for the fund’s term but reviewed by the government every quarter. PPF investments come under Exempt-Exempt-Exempt (EEE) category which means that apart from the principal investment, interest and maturity value is also tax-free.

ELSS offers returns with a lock-in period of just 3 years. A type of mutual fund, ELSS primarily invests in equity and can offer returns up to 12-15% along with added tax benefits. The minimum investment amount for ELSS may differ from one fund to another, but mostly can start as low as Rs. 500. The returns on ELSS funds are taxable under Long Term Capital Gains Tax above Rs. 1 lakh in a financial year.

NPS contributions can be invested in equities (stocks), corporate bonds and government bonds, entitling you to tax deduction under Section 80CCD. The aggregate amount of deductions under section 80C, section 80CCC and 80CCD (1) shall not, in any case, exceed ₹1,50,000. The NPS account matures at the age of 60 and you can withdraw 60% of the accumulated corpus tax-free before the maturity period. The minimum NPS annual contribution is Rs. 1,000.

You can avail tax benefit from premiums paid towards a health insurance policy or home loan. Under Section 80D of the Income Tax Act, you can claim a deduction of up to 25,000 on premiums paid towards your health insurance policy.Also, deduction up to 50,000 can be claimed on home loan interest under Section 80EE of the Income Tax Act,1961 subject to conditions provided therein.

To conclude, there are several options for you to save taxes in India. However, your investment strategy must involve the tax benefit aspect along with specific financial goals you wish to accomplish. Only thorough planning and research will help you generate and maintain wealth in the long-run. Talk to our insurance experts at Canara HSBC Life Insurance for guidance and information on various investment opportunities that also helps secure your family’s future interests.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.