Written by : Knowledge Centre Team

2026-02-25

1150 Views

7 minutes read

Share

Life insurance is one of the most effective instruments of financial risk management. It covers you or your business from various financial risks arising due to any unforeseen event.

But how is the cost of this protection determined?

Key Takeaways

|

Like all insurance products, life insurance premiums are based on risk. Specifically, they are influenced by the likelihood of the insured event occurring, in this case, death.

Life insurance policies work on the factor which determines the possibility of demise, also called ‘Mortality Rate’.

The life insurance premium will change as the mortality rate changes, and age is one of the most natural factors to affect this change.

So, yes, with age, the premium of a life insurance policy will also change. However, this increase applies only when purchasing a new policy. Once you buy a life insurance policy, the premium remains level throughout the term.

Mortality rate refers to the rate of deaths taking place at a certain age in a defined population during a specific period. This is generally used as a basis for determining the amount of premium to be charged to an insured person. The premium charged by an insurance company is thus referred to as the mortality premium.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

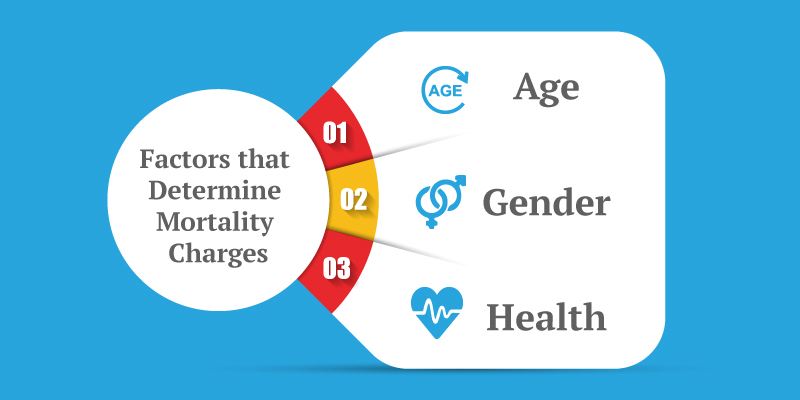

Mortality premium is basically the fee charged by an insurer to provide life coverage to the insured. It’s calculated based on mortality tables, which are actuarial tables detailing the probability of death based on age, gender, and other factors.

A mortality charge is the amount charged for the financial risk that an insurance company may suffer because of so many policyholders dying a premature death (i.e. numerous death claims at a time).

Key Points About Mortality Premium:

The insurance companies calculate the mortality premium with the help of the mortality table. Here’s how the process works:

The mortality table displays the death rate for a defined population within a specific period.

| COMMISSIONERS 2001 STANDARD ORDINARY MORTALITY TABLE | ||||

| MALE AND FEMALE | ||||

| AGE LAST BIRTHDAY | ||||

| AGE LAST BIRTHDAY | MALE 1000gx | MALE LIFE EXPECTATION | FEMALE 1000x | FEMALE LIFE EXPECTATION |

|---|---|---|---|---|

| 45 | 2.77 | 32.73 | 1.96 | 36.33 |

| 46 | 3.03 | 31.82 | 2.16 | 35.40 |

| 47 | 3.25 | 30.92 | 2.38 | 34.48 |

| 48 | 3.42 | 30.02 | 2.64 | 33.56 |

| 49 | 3.64 | 29.13 | 2.93 | 32.65 |

| 50 | 3.91 | 28.23 | 3.24 | 31.74 |

| 51 | 4.26 | 27.34 | 3.60 | 30.85 |

| 52 | 4.70 | 26.46 | 3.99 | 29.96 |

| 49 | 3.64 | 29.13 | 2.93 | 32.65 |

| 50 | 3.91 | 28.23 | 3.24 | 31.74 |

| 51 | 4.26 | 27.34 | 3.60 | 30.85 |

| 52 | 4.70 | 26.46 | 3.99 | 29.96 |

| 53 | 5.21 | 25.58 | 4.41 | 29.08 |

| 54 | 5.83 | 24.72 | 4.86 | 28.21 |

| 55 | 6.52 | 23.86 | 5.36 | 27.34 |

| 56 | 7.26 | 23.02 | 5.91 | 26.49 |

| 57 | 7.95 | 22.19 | 6.49 | 25.65 |

| 58 | 8.63 | 21.37 | 7.09 | 24.82 |

| 59 | 9.42 | 20.55 | 7.70 | 23.99 |

| 60 | 10.40 | 19.75 | 8.34 | 23.18 |

| COMMISSIONERS 2001 STANDARD ORDINARY MORTALITY TABLE | ||||

| MALE AND FEMALE | ||||

| AGE LAST BIRTHDAY | ||||

AGE LAST BIRTHDAY | MALE 1000gx | MALE LIFE EXPECTATION | FEMALE 1000x | FEMALE LIFE EXPECTATION |

|---|---|---|---|---|

| 45 | 2.77 | 32.73 | 1.96 | 36.33 |

| 46 | 3.03 | 31.82 | 2.16 | 35.40 |

| 47 | 3.25 | 30.92 | 2.38 | 34.48 |

| 48 | 3.42 | 30.02 | 2.64 | 33.56 |

| 49 | 3.64 | 29.13 | 2.93 | 32.65 |

| 50 | 3.91 | 28.23 | 3.24 | 31.74 |

| 51 | 4.26 | 27.34 | 3.60 | 30.85 |

| 52 | 4.70 | 26.46 | 3.99 | 29.96 |

| 49 | 3.64 | 29.13 | 2.93 | 32.65 |

| 50 | 3.91 | 28.23 | 3.24 | 31.74 |

| 51 | 4.26 | 27.34 | 3.60 | 30.85 |

| 52 | 4.70 | 26.46 | 3.99 | 29.96 |

| 53 | 5.21 | 25.58 | 4.41 | 29.08 |

| 54 | 5.83 | 24.72 | 4.86 | 28.21 |

| 55 | 6.52 | 23.86 | 5.36 | 27.34 |

| 56 | 7.26 | 23.02 | 5.91 | 26.49 |

| 57 | 7.95 | 22.19 | 6.49 | 25.65 |

| 58 | 8.63 | 21.37 | 7.09 | 24.82 |

| 59 | 9.42 | 20.55 | 7.70 | 23.99 |

| 60 | 10.40 | 19.75 | 8.34 | 23.18 |

The insurers take the mortality charge from the policyholder and keep it safe as the “Life Fund”.

This life fund is used to pay out the Gross Death Benefit in case of your early demise during the policy term. It is important to note that the Life Fund is never invested anywhere else. The insurers will always deduct it and save it only to pay the Sum Assured to your family in case you don’t survive the policy.

Click to use : Term Insurance Calculator

Besides mortality, many other factors decide the amount of premium you will have to pay. Apart from the health factor, these factors affect your mortality rate. This will impact the cost of your insurance, i.e. the premium to be paid by you.

So, these are various factors that decide the amount of premium you have to pay for your term life insurance.

The mortality premium is the insurance company’s way to account for the financial risk it takes by insuring your life. It is based on life expectancy and the estimated likelihood of death during the policy term. By charging this, insurers ensure they can cover the guaranteed death benefit payout if needed.

In simpler terms, it’s a cost that helps insurers prepare for the financial responsibility they undertake on your behalf.

Term life insurance provides you with a degree of certainty about the future of your family after your death. However, there's some uncertainty for the insurance company due to your risk of death.

That's why an insurance company charges the mortality premium and expense risk for the life cover they provide. The earlier you buy, the lower your mortality rate and premium. Once locked in, the premium stays the same for the entire policy term, offering peace of mind and financial security to your loved ones.

So, don’t delay. Buy early, save more, and secure your family’s future with confidence.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.