Written by : Knowledge Centre Team

2025-12-07

1087 Views

8 minutes read

Share

ULIP is a type of life insurance which along with life cover, also provides you the opportunity to invest in the market and earn returns. Thus, ULIP is a combination of both insurance and investment.

But just Investing in ULIP is not enough, you have to also see how your investment is performing from time to time.

If you haven't purchased ULIP and are looking to buy, then also investment’s performance tends to be a major factor.

When you are looking to invest in ULIPs and are confused about the options to buy, then you are most likely to look at the performance of various ULIPs before buying.

But how will you do that? One of the most popular ways you can do this is via NAV. To assess the performance of your ULIP, NAV must be tracked. It is what determines how your funds are doing.

Before moving forward, let’s look at what NAV means.

In ULIPs your money is invested in a fund. This fund is created from a pool of investments. This pool of investments is then broken down into parts or ‘units’.

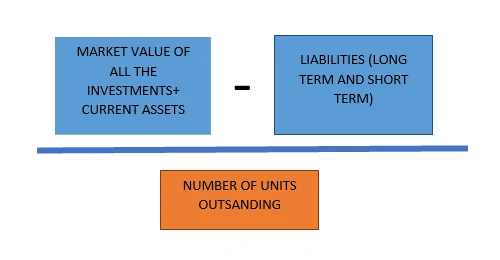

Net Asset Value, popularly abbreviated as NAV is the value of the total assets held by a fund after reducing the short-term and long-term liabilities from it.

After the fund is created from the pool of investments, the fund manager decides the number of units. This unit is then divided by the total value to arrive at the ‘unit’ NAV.

This is the value with which performances of 2 ULIPs can be compared.

Here is how it works

Every fund has a NAV value. Here is how NAV is calculated in ULIPs

Here are the steps summarized in a formula:

The NAV plays a major role in determining how the assets involved in a fund have performed over the years.

Assets of the company, both liquid and non-liquid are included while calculating the NAV. It helps you give an idea about the total worth of the company which becomes important to consider while you decide which fund to invest in.

Here is how you can track NAV so that you have a better idea of an investment.

Let us understand this with a scenario

Now if the value of the fund increases the NPV will also increase and vice versa. The higher the NPV gets after buying, the better the performance of your fund.

Continuing with the same example, Suppose the value of your fund increases to Rs 1.1 cr.

Now the NPV becomes 11 (1.1 cr/10 lakh share). Since you have brought at Rs 10, the value of the fund is now increased.

To calculate the value of the investment, you multiply the current nav per unit with the number of

units you own.

In the above case, your market value would be, 11 X 9800 = Rs 1,07,800

Though an important one, NAV is not the only factor that you need to check while buying a ULIP. Here are the other factors you should consider.

Every ULIP has some costs associated with it. These are referred to as ULIP ‘charges’. These charges are deducted from your premium and prior to calculating your fund’s NAV.

Charges involved in ULIPs are

What and how much charges will be incurred will depend on the plan you choose. For example, policies such as Canara HSBC Life Insurance Company only included Fund management and surrender charges, the rest all the charges are waived off.

Also, the mortality charges are returned to you after maturity.

Read about all the charges that your policy incurs before deciding to go ahead.

Some ULIPs involve strategies in which your fund is automatically rebalanced according to the allocation that you have set. This ensures that you do not have to get much involved.

Check that this facility is available in your ULIP. In Invest 4G, there is Auto Fund Rebalancing (AFR) which maintains your allocation of funds in a specific ratio, that you decide.

Your funds are rebalanced to your desired ratio every 3 months.

Your policy stays with you till you are alive. If you die during the policy, your family receives the sum assured, and then it ceases. But what if you have planned a goal years from now and want your policy to continue even if you die? This problem is solved by the premium protection feature.

Under this plan, if you die within the policy, then the remaining premiums are paid by the insurance company and the policy continues as intended. All the benefits will be receivable at maturity. This helps to ensure that your family can achieve their goals.

ULIP investments are perfect for meeting important goals for your family. As ULIPs can ensure that their goals will be looked after even when you can’t be there. Simultaneously, ULIPs give you the advantage of aggressive growth, which you can track with fund NAVs before investing.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online ULIP plans that blend life insurance protection with investment growth, helping you build wealth while securing your family's future.