Table Of Content:

Medical emergencies can come unannounced to anybody, and with them come the required medical expenses. With Canara HSBC Life Insurance health plans, one can be prepared for such medical expenses and ensure financial security.

Get a Call Back

Get a Call Back

Enter OTP

An OTP has been sent to your mobile number

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder as on

Name of the policy holder

Policy Holder NamePolicy No.

Policy NumberAddress of the Policyholder as per records

AddressUnclaimed Amount

Unclaimed Amount

Sorry ! No records Found

Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

What is Health Insurance?

Health insurance is a type of insurance whereby the insurance company reimburses the policyholder in case he/she falls ill and has to be hospitalised or undergo any other type of treatment. Some health insurance plans also pay out a predetermined amount in case of injury or disease which are called fixed benefit health plans. Insurance companies have tie-ups with a wide range of hospitals and the insurance amount is directly transferred to the hospital in case of a health insurance claim is filed. If the insurer does not have a tie-up with a certain hospital, the cost of treatment is reimbursed to the policyholder. The government promotes health insurance through tax deductions, as it is an important tool for maintaining public health.

Why Do You Need Health Insurance?

- Changing lifestyle: Our ancestors had a healthier lifestyle. However, daily life has drastically changed in the last few decades, giving rise to a plethora of new diseases. A sedentary lifestyle, bad eating habits, and dangerous levels of pollution have made the current generation more prone to health risks.

- Rising medical costs: Various reports and surveys have highlighted two key findings which could be a reason to worry for people without health insurance. The cost of healthcare is rising faster than other services and products and Indians primarily dip into their savings to take care of medical emergencies. Therefore, the chances of exhausting your entire savings in case of a medical emergency cannot be ruled out.

- Coverage of related costs: When you opt for a treatment, hospitalisation is just a part of the overall costs. Out-patient expenses, diagnostic tests and other related activities account for a substantial part of the overall expenses. The cost of related activities is also rising with the cost of hospitalisation. Health insurance covers pre and post-hospitalisation charges along with the cost of hospitalisation.

Types of Health Insurance Plans

Health insurance plans come in various forms to meet different needs, whether for individuals, families, or groups. Choosing the right plan depends on factors like age, health conditions, family size, and specific medical concerns.

- Cancer Insurance Plans: Cancer insurance plans offer financial coverage specifically for the diagnosis and treatment of cancer. These plans cover expenses like chemotherapy, radiation, surgery, and hospitalisation. The payout is usually a lump sum upon diagnosis, helping policyholders manage treatment costs without depleting their savings.

- Critical Illness Plans: Critical illness plans provide coverage for life-threatening conditions such as heart attacks, strokes, kidney failure, and more. Upon diagnosis of a covered illness, the insurer pays a lump sum that can be used for medical treatment, post-treatment care, or managing day-to-day expenses during recovery.

- Individual Health Insurance Plan: An individual health insurance plan covers the medical expenses of a single policyholder. It includes hospitalisation, pre- and post-hospitalisation costs, and other healthcare-related expenses. This type of plan is ideal for those who want personalised coverage and benefits.

- Family Floater Health Insurance Plan: A family floater health insurance plan covers the entire family under one policy. The sum insured is shared among all family members, meaning any member can use the full coverage amount. This plan is cost-effective for families as it eliminates the need for separate policies for each individual.

- Group Health Insurance Plan: Group health insurance plans are offered by employers to their employees. They provide health coverage to a group of individuals under a single policy. These plans are generally more affordable than individual plans and sometimes extend coverage to the employee's family members.

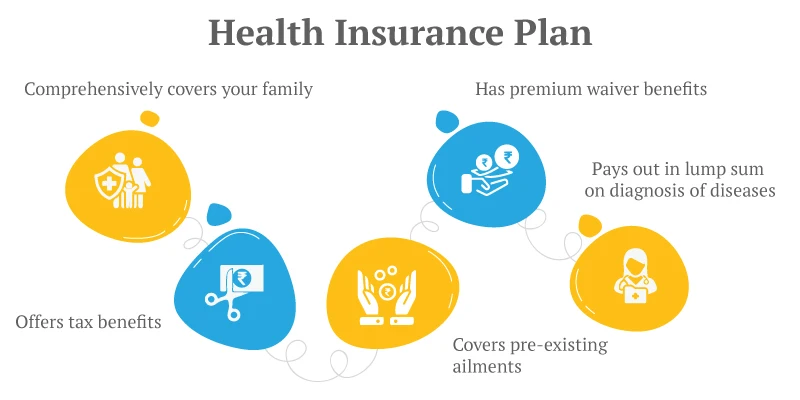

Key Benefits of Health Insurance Plans

With a fixed benefit health insurance plan you get the flexibility to choose the utilisation of the sum assured. Critical illnesses like heart and kidney diseases can take a heavy financial and mental toll on the family. The overall expenses could be substantial ranging from treatment cost to the loss of livelihood in some cases. The payout of fixed benefit health insurance does not depend on the actual cost of treatment. It can help you take care of the different costs related to a critical illness.

You do not have to produce hundreds of bills and documents to claim the sum assured. The claim process of fixed-benefit health insurance is simple and hassle-free. Just a report from the doctor specifying the condition is enough to receive the payout.

The diagnosis of a critical illness is a difficult situation for all family members. Health insurance cover continues even after a minor claim is made, but the insured is not required to pay the premiums. With the premium waiver, the insured’s family does not have to worry about losing the health insurance cover.

The cost of healthcare is on the rise, but a good health insurance policy takes care of inflation. Canara HSBC Life Insurance Health Plan comes with an increasing cover option, which helps the insured take care of the rising cost of medical care. With the option, the sum assured increases at a pre-defined rate nullifying the impact of healthcare inflation.

Eligibility Criteria for Health Insurance Plans

Best health insurance plans come with specific eligibility criteria that individuals must meet to avail of coverage. These criteria vary across insurers and policies but generally include factors such as age, pre-existing conditions, and medical history. Understanding these requirements can help you choose the right policy and avoid claim rejections later.

- Age of Entry: Most health insurance plans have a minimum and maximum entry age for policyholders. Generally, individual health plans allow entry from 18 years onward, while family floater plans cover children as young as 90 days. Senior citizen health insurance plans usually have a minimum entry age of 60 years, while some policies have an upper age limit of 65 to 80 years.

- Pre-Existing Conditions: Pre-existing conditions, such as diabetes, hypertension, or heart disease, impact eligibility for health insurance. Most insurers have a waiting period ranging from 2 to 4 years before covering pre-existing illnesses, though some policies offer shorter waiting periods with an extra premium. Individuals with severe health conditions may be required to undergo medical tests before approval.

Things to Consider Before You Pick a Health Insurance Plan

Claim Process: The claim process is an important factor for all insurance products as no one wants to run from pillar to post when the need arises. You should choose a health insurance plan with a simple and fast claim process. A helpful customer support system would be an additional advantage.

The insurance amount: The amount of cover is one of the most critical components of a health insurance plan as an inadequate amount will not be of much help. While choosing the insurance amount, take into consideration your age and history of diseases.. You should also keep in mind your income while choosing the premiums. Essentially, you should try to strike a balance between the insurance amount and the premiums.

Family health insurance: The health of your family members is as important as yours while taking a health insurance plan. Take into account the existing ailments and the age of your family members while choosing a health insurance plan.

Pre/post hospitalisation: There are several costs related to hospitalisation. Ideally, one should choose medical insurance that covers pre and post hospitalisation charges. The pre and post hospitalisation expenses include the cost of consultation and diagnostic tests.

Many people hesitate to buy health insurance due to common misconceptions. This can lead to financial setbacks during medical emergencies. Understanding the truth behind these myths can help you make better decisions and ensure you are adequately protected.

Who Should Buy a Health Insurance Plan?

- Young Professionals and Individuals: Young professionals often overlook health insurance, assuming they are healthy and do not need it. However, buying a health insurance plan early in life offers several benefits, such as lower premiums, access to better coverage, and no waiting periods when they actually need the policy. Additionally, it helps in saving taxes under Section 80D of the Income Tax Act.

- Families with Dependents: A family health insurance plan is crucial for those who have dependents, including a spouse, children, or elderly parents. A family floater policy provides coverage for all members under one plan, ensuring medical expenses are covered in case of sudden illness, hospitalisation, or accident.

- Senior Citizens and Retired Individuals: Older adults are more prone to health issues, making health insurance a necessity. With rising medical costs, a dedicated senior citizen health insurance plan ensures they receive the best treatment without financial strain.

- Self-Employed and Business Owners: Unlike salaried employees who may receive corporate health insurance, self-employed individuals and business owners need to arrange their own coverage. Since they do not have employer-sponsored benefits, an individual or family health insurance plan provides a financial cushion against unexpected medical expenses.

- Individuals with Pre-Existing Conditions: People with pre-existing conditions such as diabetes, hypertension, or heart disease should invest in a health insurance policy tailored to their medical needs. While pre-existing conditions typically have waiting periods before coverage begins, purchasing a policy early ensures they are covered when needed. Some insurers offer disease-specific plans that provide better benefits for chronic illnesses.

- Employees with Limited or No Corporate Insurance: While many employers offer the best health insurance plan, the coverage may not always be sufficient. Corporate health plans often have limited sum insured amounts, exclusions, and restrictions on family members. Employees should consider purchasing an additional personal health insurance plan to supplement their coverage and avoid out-of-pocket expenses during medical emergencies.

Canara HSBC Life Insurance

We have over 15 years of experience in delivering exceptional value to our customers through our range of individual and group insurance solutions, designed to meet their various needs, including savings and investment, retirement, protection, and more.

15,700+ Partner Branches

15,700+ Partner Branches

Canara Bank, HSBC India, Other Alternate Channels

₹436,385 Mn Assets Managed

₹436,385 Mn Assets Managed

Assets Managed as of Jun' 25

99.43% Claims Settled

99.43% Claims Settled

Individual Death Claims settled for FY 2024 - 2025

200.42% Solvency Ratio

200.42% Solvency Ratio

Way Above the IRDAI Mandate

Benefits of Buying Health Insurance Plan Early

Health emergency can strike anyone and with the change in lifestyles, diseases are affecting people at a very young age. Being young is not a protection against disease. It is advisable to get adequate insurance cover.

The cost of a policy should not be the only guiding principle while buying a health insurance plan. You should also take into consideration the suitability, the benefits and the other features while buying insurance.

Health insurance policies have a mandatory waiting period, which means you cannot ask for benefits for certain treatments before a specified period of time. It is better to buy health insurance when you are young so that the waiting period gets over when the chances of illness are low.

Even though a minimum hospitalisation of 24 hours was mandatory for insurance benefits to kick in, with an advancement in technology many procedures require much less time. Considering the changing dynamics of treatment, many insurance companies have started accepting claims for hospitalisations of less than 24 hours.

Why Get Health Insurance While You Are Young?

These are two plan options that offer fixed-term coverage. A customer may choose any one of them basis their protection needs.

1. Cheaper when younger Getting health insurance while you are young could help you reduce the premium amount significantly. A critical illness policy with a sum assured of Rs. 5 Lakhs and tenure of 35 years for a 25-year-old non-smoking male will cost around Rs. 826 per year. But the same policy will cost a 45-year-old non-smoking male Rs. 2,559 per year. |

2. Group insurance is not sufficient Many people believe that having group insurance is sufficient to take care of their health needs. With the rise in the cost of medical care, group insurance cover may not be enough to cover all your medical bills. |

3. Better financial planning Buying a health insurance policy at a young age is not only cheap but also helps you plan for the long-term without worrying about emergencies. It is not possible to predict accidents, but with a health insurance plan, you can live a secure life with the assurance that medical emergencies will not derail your finances. |

4. Increase in lifestyle diseases Due to a tectonic change in the way people live nowadays, the incidence of lifestyle diseases has increased. It is not rare to hear about individuals in their 20s suffering from diseases, which were unheard of in the age group a few decades ago. The increase in pollution and sedentary lifestyles have given rise to a host of diseases related to the heart and lungs, which primarily affect younger people. Therefore, with the rising incidence of lifestyle diseases, it is pertinent to have a health insurance plan. |

5. Better deals The premiums are higher for people with pre-existing diseases. When you are young, the chances of having pre-existing diseases is very low, which helps you get a better deal. The diseases that are diagnosed as you grow older are automatically covered by the policy. |

6. Receive full benefits When you buy a health insurance policy, there is a waiting list for certain surgeries, special treatments or pre-existing conditions. If you buy a health insurance plan early, you are less likely to be impacted by the waiting period, as the incidence of diseases is low when one is young. Insurance companies also offer sum insured indexation benefit when you continue with the same policy for a certain number of years every claim-free year. If you buy a policy early, you can earn a higher sum insured, which reduces the cost of the policy. |

A Guide to Health Insurance Portability

- The application for portability has to be made 45 days before the existing policy expires.

- The portability of health insurance plan is not guaranteed, and the new insurance company may reject the request if the risk is not acceptable.

- The new insurance company has to respond to your portability request within 15 days. If you are due to renew the existing policy and the new insurer delays your request, the onus is on the insurer to request the existing insurance company for a short extension of your policy.

- The new insurer may accept your request considering your claims history and the pre-existing diseases. A policyholder with low claims and no pre-existing diseases has a higher chance of acceptance.

- An individual can opt to continue with the existing insurance company midway through the portability process.

- While opting for portability, you do not have to sit out waiting periods all over again. The waiting period seamlessly continues with the new health insurance plan.

- Insurance companies deny portability to individuals with a break in the policy tenure, which means you have to apply for portability before the existing policy expires.

How to File a Health Insurance Claim?

Filing a health insurance claim ensures you receive the financial support needed for medical expenses covered under your policy.

There are two main types of claims you can file, depending on your situation:

- Reimbursement Claims: In a reimbursement claim, you pay the medical expenses upfront and later submit the bills and necessary documents to the insurance provider for repayment. The insurer verifies the documents before processing the reimbursement.

- Cashless Claims: In a cashless claim, the insurer directly settles the medical bills with the network hospital. You need to seek treatment at a hospital that has a tie-up with your insurance company and get pre-authorisation for planned procedures.

- Planned Hospitalisation Process: For planned treatments, inform your insurer and the network hospital in advance. Submit the required documents and obtain pre-authorisation before the hospitalisation to avail of cashless treatment smoothly.

- Emergency Hospitalisation Process: In emergencies, inform your insurance provider within the stipulated time after admission. If the hospital is part of the insurer’s network, you can opt for cashless treatment; otherwise, you can later file for reimbursement by submitting all necessary documents and medical bills.

Key Factors to Consider Before Buying Health Insurance Plans

Choosing the best health insurance plan requires careful evaluation of various factors to ensure you get the best coverage for your needs.

Coverage & Sum Insured: Ensure the plan provides adequate coverage for hospitalisation, critical illnesses, pre- and post-hospitalisation expenses, and daycare procedures.

Waiting Period: Check the waiting period for pre-existing diseases and specific treatments to avoid surprises during claims.

Network Hospitals: A wide network of cashless hospitals ensures you can get treatment without financial stress.

Premium & Affordability: Compare premium costs with benefits to find a plan that fits your budget without compromising on coverage.

Exclusions & Limitations: Read the policy terms carefully to understand what is not covered, such as specific diseases, waiting periods, and sub-limits.

Claim Settlement Process: A smooth and quick claim process ensures hassle-free access to medical benefits when needed.

Additional Benefits & Riders: Look for features like maternity coverage, critical illness riders, and wellness benefits for added protection.

Coverage and Exclusions

Understanding what your best health insurance policy covers and excludes is essential to avoid surprises during claims. Here is a breakdown of common inclusions and exclusions:

What is Covered?

Hospitalisation Expenses: Costs related to room rent, ICU charges, doctor’s fees, and nursing expenses.

Pre- and Post-Hospitalisation: Medical expenses incurred before and after hospitalisation, generally for a specific period (e.g., 30 days before and 60 days after).

Daycare Procedures: Treatments that don’t require 24-hour hospitalisation, such as cataract surgery or chemotherapy.

Ambulance Charges: Expenses related to emergency transportation to the hospital.

Critical Illness Coverage: Lump-sum payment upon diagnosis of specific critical illnesses like cancer, heart attack, or stroke.

Maternity Benefits: Coverage for delivery expenses and newborn care (depending on the policy).

What is Not Covered?

Pre-existing Diseases: Medical conditions that exist before buying the policy. They are usually covered after a waiting period.

Cosmetic Treatments: Procedures done for aesthetic reasons, like plastic surgery, unless medically necessary due to injury.

Dental and Vision Expenses: Unless specified, most policies don’t cover routine dental or vision care.

Self-Inflicted Injuries: Injuries caused by intentional self-harm or suicide attempts.

Alternative Treatments: Unless explicitly mentioned, treatments like naturopathy or acupuncture are usually excluded.

Non-Medical Expenses: Charges for items like food, toiletries, or administrative fees during hospitalisation.

Reading your policy document carefully helps you understand the full extent of coverage and avoid claim rejections later.

Documents Required for Health Insurance Claim Reimbursement

When filing a health insurance claim, submitting the correct documents ensures a smooth and hassle-free process. Make sure to submit the following documents within the insurer’s specified timeline to avoid delays or claim rejections.

Duly Filled Claim Form: A completed and signed form provided by the insurer.

Health Card Copy: A copy of your insurance card issued by the provider.

Hospital Discharge Summary: Detailed documentation of your treatment and discharge from the hospital.

Original Hospital Bills & Receipts: Bills, payment receipts, and invoices for all medical expenses.

Doctor’s Prescription: A copy of the prescription advising hospitalisation or treatment.

Investigation Reports: Lab tests, X-rays, MRI reports, or any diagnostic tests conducted during treatment.

Pharmacy Bills: Original bills and prescriptions for medicines purchased.

Bank Account Details: A cancelled cheque or bank passbook copy for the reimbursement transfer.

Valid ID Proof: A copy of a government-issued ID, such as an Aadhaar card or passport.

Frequently Asked Questions (FAQs) for Health Insurance

Buying health insurance online is cheaper and more convenient than getting a policy through an agent. Insurance companies work on the premise that people who have access to the internet and are willing to buy policies online are more likely to be better-off and healthy. Moreover, online plans save a lot of money for the companies as the administrative costs such as documentation and office space get eliminated. The insurance companies pass on the savings to the customer and offer lower premiums on online health insurance plans. With online plans, you do not have to visit the bank of the insurer’s branch and can buy the policy sitting in the comfort of your home.

Canara HSBC Life Insurance provides a comprehensive health insurance plan named Health First Plan. It is a fixed benefit plan that provides a lump-sum amount on the occurrence of heart or cancer-related conditions, besides 26 other major critical illnesses. It is a flexible plan that gives you the freedom to choose the cover you need along with various options to customize the plan according to your requirements.

Diseases can strike without any warnings. Having a health plan protects you from unforeseen financial hardships and helps you lead a stress-free life. A health plan also ensures that you receive quality treatment in case you are diagnosed with a serious illness. A health plan creates a buffer around your savings, which remains unscathed even in cases of substantial treatment costs.

There are no uniform rules to select an insurance policy as the needs and medical history of people vary. However, Health First plan from Canara HSBC Life Insurance offers comprehensive coverage, which could be adequate to take care of all your health insurance needs.

The health insurance premium depends on a variety of factors such as age, geographical location, lifestyle habits and occupation. The best way to calculate health insurance premiums is to use a good online premium calculator which is easily available.

With the change in lifestyles, the incidence of diseases has increased drastically. Health insurance is necessary to cover against lifestyle diseases, which are on the rise due to poor nutrition, lack of physical activity and pollution.

A health insurance policy ensures that you and your loved ones do not have to think about the finances while opting for treatment. In the event of hospitalisation, a knowledge of the claim process saves the policyholder from undue hassles. A hospitalisation can generate reams of bills and documents. The claim process of fixed-benefit health insurance is very simple as the payout does not depend on the cost of treatment. In case a critical illness is diagnosed you just have to intimate the insurance company. The insured just has to fill a claims form and attach the doctor’s report on the illness. One doesn’t need detailed bills and prescriptions to claim the sum assured. The entire process is very simple and hassle-free.

Health insurance premiums can help you in reducing tax outgo, as it is eligible for tax deduction under Section 80D of the Indian Income Tax Act, 1961. If you choose a health insurance plan for parents aged 60 years and above, you can claim Rs. 50,000 as a tax deduction. Senior citizens up to 60 years can also claim up to Rs 25,000 as a deduction for the health insurance premiums paid for themselves, or for their spouse or children. This deduction will be available with respect to payments towards annual premium on a health insurance policy, or preventive health check-up of a senior citizen. It is also available for any other medical expenses related to senior citizens. In such a case, if you are paying the health insurance premiums for your senior citizen parents, the total deduction you can avail is Rs. 75,000 per year.

There are no fixed guidelines for choosing adequate health insurance cover, but the cover should depend on factors such as income, family history of diseases and geographical location. Considering the high cost of medical care in metro cities, one should have a minimum cover of Rs 10 lakhs. The cost of hospitalisation and associated costs are higher in large cities. Smaller cities have lower cost of living and a cover of Rs 4-5 lakhs would suffice.

Health insurance plans do not cover all the diseases and certain conditions are excluded from the cover. Some of the common exclusions are:

- 1.Pre-existing medical conditions

- 2.Alternative therapies

- 3.Cosmetic treatments

- 4.Pregnancy and child birth

- 5.Diagnostic expenses

- 6.Dental

- 7.Injuries caused due to a suicide attempt

- 8.Waiting period clause

- 9.Permanent exclusions: Injuries due to war, HIV, intentional injuries, congenital diseases, and others are permanent exclusions

Diseases can strike without any warnings. Having a health plan protects you from unforeseen financial hardships and helps you lead a stress-free life. A health plan also ensures that you receive quality treatment in case you are diagnosed with a serious illness. A health plan creates a buffer around your savings, which remains unscathed even in cases of substantial treatment costs.

Hear From Our Happy Customers

Popular Searches

- Family Health Insurance Plan

- What is Health Insurance?

- Health Insurance For Parents

- Health Insurance Tax Benefit Under 80-D

- Health Insurance Facts

- Difference Between Life and Health Insurance

- Difference Between Life and Health Insurance

- Incurred Claim Ratio

- What is Copay in Health Insurance?

- What is Cashless Treatment?

- Accidental Cover in Saral Jeevan Bima

- Accidental Cover in Saral Jeevan Bima

- Tips to Buy Health Insurance

- Short Term Health Insurance Plan

- When Should You Buy Health Insurance?