Written by : Knowledge Center Team

2025-11-10

1185 Views

8 minutes read

Share

Your child is one of the greatest blessings you receive in your life. But with all the joys comes a huge responsibility as well. Your child is dependent on you and you have to ensure that they have all that is needed.

With the costs ever-increasing due to inflation and other policies, only savings is not enough. You have to make sure that your corpus grows steadily and is enough till your child attains the age where this money is needed.

Also, life is so uncertain, it is impossible to predict what may happen to you. You need to be prepared for every outcome, even for the time you are not present with your family.

Child insurance plans are the type of life insurance plans that also offer you an opportunity to invest in the market. These plans are also referred to as child investment plans and help in financially securing your child’s future by enabling you to create a sufficient corpus that can be used to meet your child’s goals.

You must have a lot of dreams regarding your child’s future. Every parent wants to do the best that they can to help their child achieve their goals. Some of these goals are:

For example, currently, if your child wants to pursue MBA from a reputed college, it will cost you around 20-25 lakhs. This cost is expected to further surge.

These can include things like school fees, daily expenses, health expenditures of a child, travelling, clothes, etc.

A child insurance plan includes the benefit of both investment and insurance. Thus, the best investment plans for a child can assist you in meeting all the above-stated goals. Here’s how:

This is one of the major benefits of a child insurance plan. It allows you to invest in market securities and grow your corpus. Through your child investment plan, you can invest in various asset classes as per your preference and risk-taking ability.

The various classes you can invest in this plan include:

Plans such as Canara HSBC Life Insurance ULIP, Promise4Growth Plus offers you multiple portfolio management strategies. Portfolio management includes some pre-defined rules that work in a set manner. Opting for this helps you to manage your fund easily without too much intervention.

Choosing which fund to invest in and answering questions such as when to get in the fund, when to exit, requires a lot of knowledge and thus can be a time-consuming process. However, portfolio management removes this trouble from your life and takes care of your investments.

This refers to withdrawing a certain sum from your accumulated corpus. A child insurance plan allows you to withdraw a part of your money from the fund. This can help you a lot in times of financial emergency. With the help of a partial withdrawal facility, you do not have to ask for loans, you can just use your policy.

A child insurance plan involves both maturity and death benefits as the need arises. If you die during your child investment plan, a sum assured that you decide at the time of purchasing is given to your family.

If you survive the policy, the value of your fund along with the bonuses (if any) will be given so that you can help your child in achieving his goals.

With child insurance plans, you have the freedom to choose the choice of your pay-out. A pay-out is the amount you will receive after the maturity of the policy. You have the following two options to choose from

Here are some child insurance plans from Canara HSBC Life insurance that can help you do the best for your child.

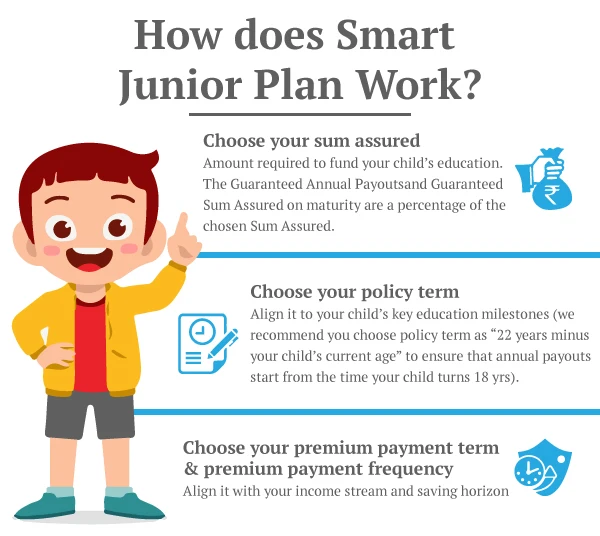

There is no set period at which you should start planning. The only answer is to start planning as early as you can. That is, as soon as you become a father, you should start planning for your child. With long-term investment plans like Promise4Growth Plus and Smart Junior Plan, you may not even have to worry about changing your investment for the next 15-20 years.

This is a long enough period for you to build a huge corpus with your small regular savings for your child.

An OTP has been sent to your mobile number

Sorry! No records Found

Thank You for submitting the response, will get back with you.

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.