Written by : Knowledge Centre Team

2025-08-02

889 Views

6 minutes read

Share

Indian parents are considerably protective when it comes to their children. However, this protectiveness can sometimes get too much and hinder children from growing into fully independent and self-sufficient individuals. It is imperative to make Indian parents aware of their financial mistakes so they can plan in a better way to guard the economic future of their children. From sending your kids to the best schools and colleges to buying the best child insurance plan, you do everything to shield their future. However, there are some common mistakes that you make as a parent.

As parents, when it comes to your children, all you think about is how you can help them grow into healthy and educated individuals. In addition to this, every parent tends to fret the most about the financial practices of their children.

However, as a parent, you need to understand that your children pick up their financial habits according to their requirements. Hence, instead of being over-protective of the financial position of your grown-up or growing children, you must try and rectify some of the common financial mistakes mentioned here that you make as parents.

This usually happens with all parents, and almost every Indian parent is guilty of this. As soon as a kid comes into your life, all your material choices, especially money-related ones, spin around your children.

Yet, it would help if you remembered to put something aside for your future. Not putting something aside for your retirement today can cause problems later.

Relying on your children to help you through your old age is not a good plan as it can create an additional burden on their finances. Hence, it is advisable to start investing some funds in a retirement or pension plan from an early age that help you remain financially independent once you retire. Apart from this, investing funds in a retirement plan also allows you to build a corpus and remain financially guarded against unforeseen monetary risks.

Learn how to start your retirement plan.

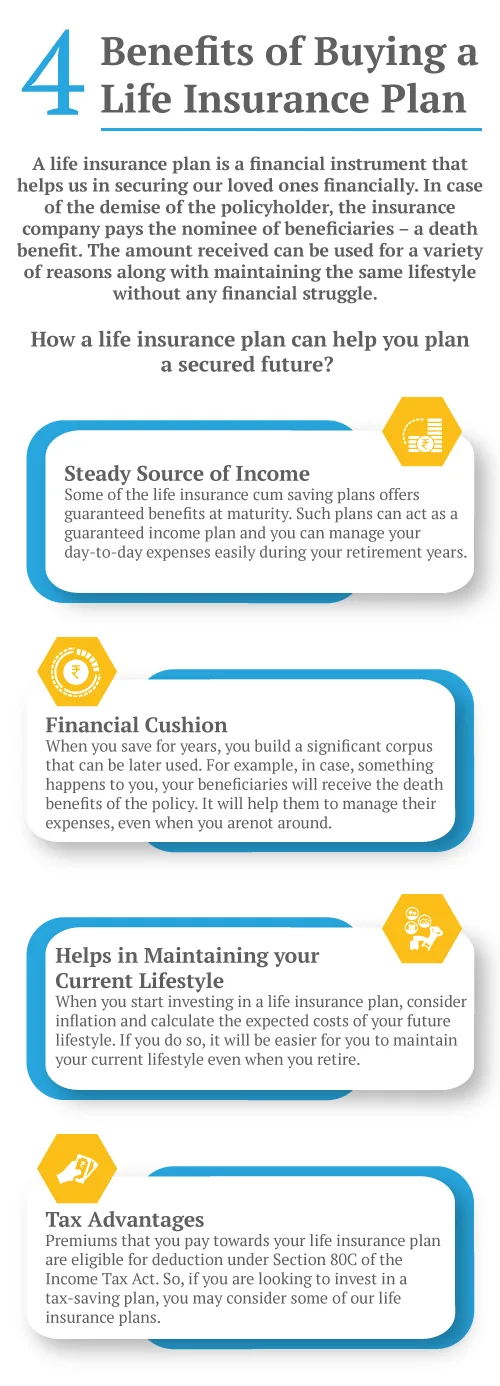

You never understand what might happen the next moment, and it is wise of you to remain prepared for it. A life insurance plan is one such step that can ensure your family against the vulnerabilities of life.

When it comes to life insurance, you can choose the time limit you want, your immediate beneficiary, and how much you will deposit in the insurance. The objective of life insurance plans is to give monetary support to your family if there should be an unanticipated occasion.

Life insurance also gives you the benefit of paying off pending expenses or debts after you are gone so children do not get burdened with your monetary obligations. To top that, you also have the choice of planning your life insurance as an inheritance. Talk to your bank about a life insurance policy now.

No matter how young your kid is, it is always best to start saving early for their education. The more you delay saving for their future, the more it will snowball. Also, the fundamental justification for the downfall is the high levels of non-performing assets (NPAs). Hence, to avoid all the last minute hassle, it is advised that you start saving for your child's higher education from the time your kid is born.

Learn why new parents should buy a life insurance plan.

While growing up, it is normal for kids to gain from their parents and emulate their habits. Nonetheless, in an ordinary Indian family, children are not involved in monetary matters. Usually, guardians teach their kids not to stress over cash. This practice or perspective won’t help out children much when they grow up.

If you don’t teach children to save cash, spend it carefully and set something aside for the future, they’ll face troubles later. Educating your children about finances is of great importance. Without basic knowledge about responsibly handling money, your children might not be prepared for the real world. They may find it difficult to adjust cheque books, plan their budgets, and obviously, save money.

Also, when your children reach the appropriate age, you should tell them how different ways of saving money can help them out if they keep investing and have patience. Remember not to overwhelm them with knowledge because they may get confused. Make sure that they understand the significance of money and don’t make financial mistakes you have made. Also, this is a way to guarantee that your children do not feel lost when it comes to savings, taxes, planning monthly budgets, or investing in savings plans.

Now that you have understood what mistakes you are making as a parent, it is better to start working on rectifying your mistakes to create a strong financial net for your children. If you are looking for some comprehensive savings, retirement or plans to remain financially guarded, look no further than Canara HSBC Life Insurance. Here you can get the most extensive saving plans tailored as per your distinct monetary needs that yield the highest return on your investments.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.