Written by : Knowledge Centre Team

2025-11-22

1293 Views

11 minutes read

Share

Financial planning and wealth management are both a part of personal financial management. Financial planning and wealth management are both related to money, but they’re vastly different. Understanding the differences between these two different financial approaches are important. Knowing the difference between financial planning and wealth management will help you choose the right one.

Financial management helps you in budgeting your income and expenses. You can plan your investments, keep track of money spent and do course corrections when needed.

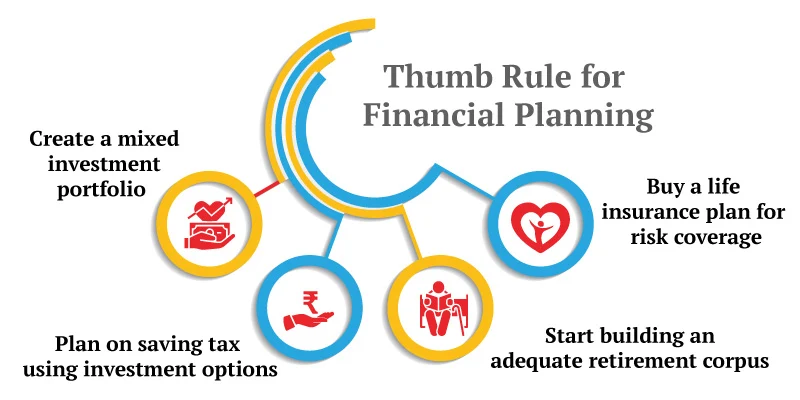

Financial planning is the process of developing a strategy for managing your financial goals. This typically involves taking into account factors such as

Financial planning is often thought of as a one-time process. It is often linked to investing. You may implement financial planning to help meet long-term goals, such as retirement or include short-term goals, such as saving for a down payment on a home.

Wealth management is a term that is used to describe the management of assets to help you reach your financial goals. Wealth management strategies may include investing in stocks and bonds, real estate, or other types of assets.

It may also include financial advising and other advice designed to help you maximize your assets.

Many people confuse financial planning and wealth management . However, there are some key differences between the two disciplines. Financial planning is often a one-time process that is used to create a financial plan to help achieve short and long-term financial goals.

| Financial Planning | Wealth Management |

| You only need an income for financial planning | You need a large pool of funds for wealth management |

| Meet short- and long-term financial goals | Manages assets to increase or preserve the value |

| Focuses on planning | Focuses on execution |

| Manages cash flow | Creates or preserves money and assets |

| Decisions based on financial goals | Decisions focus on wealth goals, i.e., creation or preservation |

| Gives a comprehensive roadmap for financial life | Focuses on immediate portfolio strategy |

Financial planning revolves around how you will manage your finances and the process involves assessing your current financial situation, identifying your goals and then developing a strategy:

Many different strategies can be employed in wealth management. Some common ones include investing in stocks and bonds, real estate, and commodities. Wealth management broadly focuses on accumulation, preservation and distribution which includes managing a portfolio of different assets.

Each of the strategies described above requires investment in an appropriate asset class or financial instrument. Some examples of popular instruments are listed below:

Financial planners help you develop a financial plan to meet your short- and long-term financial goals whereas wealth managers help you manage your assets to increase their value. Financial planning often focuses on asset accumulation whereas wealth management typically focuses on asset allocation.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.