Written by : Knowledge Centre Team

2025-08-02

882 Views

Share

As you balance work, children, school events, bond obligations, house maintenance, and potentially caring for your elderly parents, your 40s can be a hectic time. Most people in this period of life feel like they are being tugged in every direction and never know what to tackle first. When all of these aspects of your financial life come together, careful planning and strategic investing are required.

Now that you're in your forties, the financial planning actions that enabled you to create a framework or take care of your family a few years ago may not be adequate. Financial planning is crucial for people of all ages, but it is especially important for those in their forties.

This decade may be the first time you feel the strain of impending retirement, sending your children off to college, or debating downsizing your family home.

Not everything will go according to how you planned it 20 years ago. Maybe you have a bigger family and more responsibilities. Your financial situation could shift drastically, and here's where most people struggle with finding the balance between spending and saving.

You've reached the point in your life when you need to restructure your portfolio towards financial instruments to protect your money from economic uncertainty. Instead of generating profits, your priority should be to protect your money.

For instance, you may have participated in stock funds. Now, you should switch to balanced funds in your mid-forties and debt funds. This technique not only protects your investment from price volatility but also ensures consistent and predictable profits.

You must save more or alter your savings rate to account for inflation so that you never run out of money in retirement.

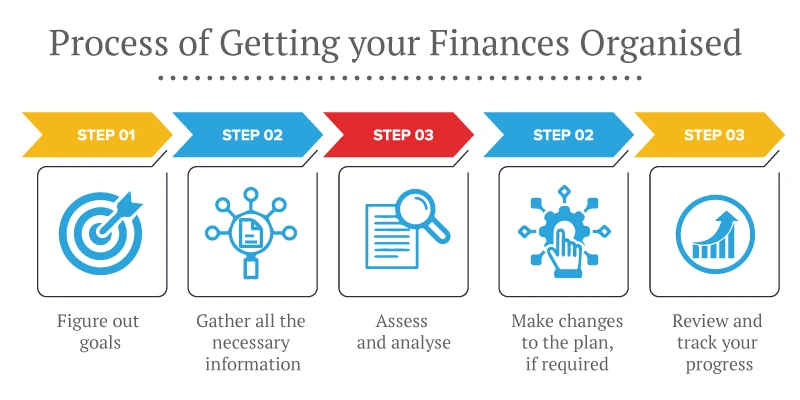

The majority of people live day to day, saving money where they can. They're hoping it'll pile up to enough for them to retire comfortably. Do you realise how much money you've saved? What about the amount you require? When you're immersed in day-to-day bills and unforeseen expenses, it's easy to overlook the long-term. It's better to conduct a route to your goals when you're aware of them. So, disintegrate your retirement requirements into precise figures.

If you're having trouble deciding on a goal number or your next financial steps, try using a retirement calculator. Even if it's a small step at a time that awareness will help you get closer to your objective.

Clearing off any high-interest consumer debt will increase your financial stability better than nearly any other financial activity. It is related to savings or investment because the equilibrium price direct debit charges more than 15% in interest each year. Student debt can be a high-cost burden, especially if you took out the loan when interest rates were higher.

Yet, there is one type of debt that you don't have to pay off right away: your mortgage. It is because mortgages are often lower than credit card interest rates, and you may be eligible for tax relief. You may be eligible to deduct mortgage payments from your tax liability if you itemize deductions. When it comes to tax time, consult with a good accountant to see what benefits may apply to your circumstances.

Doing your homework pays off. Be knowledgeable of the various retirement plan options available. Consult your HR department to learn more about what your firm has to offer.

Is your company offering a retirement referral bonus? If they've committed to match a portion of your retirement savings (typically up to 5%), make that your minimal investment. In the longer term, that added level will make a sizable impact.

If you've worked multiple jobs, you may have multiple retirement plans. Now seems to be a perfect opportunity to organise and review all of your investments.

Canara HSBC offers several retirement plans that allow you to monitor how much you're spending in asset management fees, invest any spare funds, and see how your investments are allocated.

You must also monitor the recommendations individualised for you in a Canara HSBC retirement plan because it's far simpler to get on the schedule in your 40s than it is in your 50s. After all, you have more resources to concentrate on.

Every retirement goal allows you to create a personalised retirement plan to help you figure out just how much you'll want to save for retirement depending on when and where you want to retire.

One of the most significant advantages of being in your forties is the increased financial security. You're probably making a decent living. In addition to your essential needs, you can afford a variety of desires.

However, avoiding lifestyle inflation is recommended for a solid financial plan. Certain things, like a family vacation, can still be enjoyed. However, you should not spend all of your money on improving your lifestyle or keeping up with the Sharma's in your neighbourhood. Lifestyle inflation prohibits you from saving as much as you would like in your 40s.

Learn why should you consider inflation when planning your retirement.

It's great to pamper yourself and your family but do so with intention. Keep it inside the bounds of your primary financial objectives. Allowing your costs to spiral out of control is a bad idea.

Life may toss you changeups at any time, so it's best to be prepared. You probably have a more stable income and aren't dealing with the huge family and work changes that occur in your twenties and thirties. You also have plenty of time before retiring to make some sensible financial decisions.

If needed, hire an independent financial planner with expertise in wealth planning to help you and your family navigate the process.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.