Written by : Knowledge Center Team

2025-11-16

1102 Views

6 minutes read

Share

As a human being, it is natural to strive to achieve Roti, Kapda, and Makaan, the basic tenets of life that give security and sustenance. Buying roti is essential but do you have to buy a home? And even if you do, will it be a good investment?

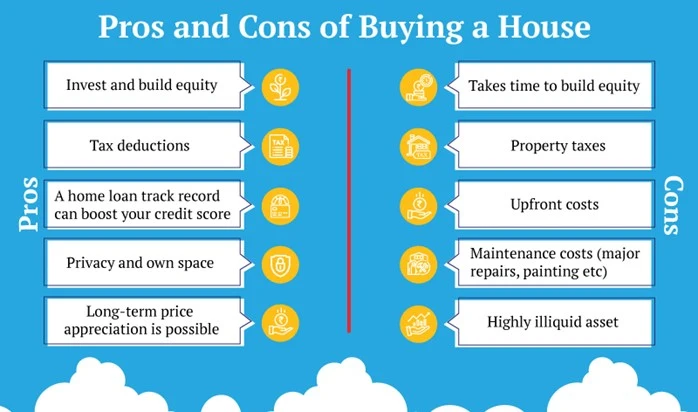

Buying a house has its pros and cons. You may have your own wealth goals and objectives for buying a house. Listed below are a few top reasons why people buy houses:

You have dreamt of buying a home on turning 30, apart from reaching other goals such as getting married and saving for retirement. The Indian government has taken several concrete steps in the last 3 decades to make home-buying an easier and more affordable process.

Home loan applications are now processed in a jiffy and lenders offer attractive payment options for properties under construction. A home loan is typically availed for tenures ranging from 20 years to 30 years. Longer the tenure, the smaller the EMI. However, the longer the tenure, more the interest you end up paying on the loan.

For example:

Here is a look at EMIs and applicable interests for different tenures.

| Years | EMI | Principal | Total Interest | Total Repayment |

|---|---|---|---|---|

| 15 | 44,941 | 50,00,000 | 30,89,454 | 80,89,454 |

| 20 | 38,765 | 43,03,587 | 93,03,587 | |

| 25 | 35,339 | 56,01,688 | 1,06,01,688 | |

| 30 | 33,265 | 69,75,445 | 1,19,75,448 |

Lenders rarely finance 100% of the cost of the property. You will have to pay a margin amount upfront (commonly termed as a “down payment”). Therefore, you must also factor in the opportunity cost of the down payment amount.

When you invest in a property, the total cost incurred is much higher than the price advertised. For example, if you are buying a flat worth Rs.1.5Crores, you must factor in the property tax, maintenance, association/society charges, costs involved in transferring meter, khatha, etc. to your name. If you are availing of a home loan, factor in the interest and one-time charges.

Learn how to plan for your dream house at retirement.

Example: Ramesh bought a flat, from a prominent builder, in 2013 in west Bangalore. The advertised price was Rs. 27 lakhs. Ramesh had enough savings to buy this flat without a home loan. He ended up paying Rs. 35 lakhs that included stamp duty, advance corpus for maintenance, covered car parking etc.

Fortunately, the much-hyped metro line came up close by and the nearest station was 2 KM away. Property prices shot up and Ramesh’s flat was worth 65 lakhs by the end of 2021. What if Ramesh had let out his flat between 2013 and 2021. Look at the rental yield:

| Year | Value of Flat (in Rs Lakhs) | Rent/Month | Yield |

|---|---|---|---|

| 2013 | 35.00 | 10,000 | 3.43% |

| 2014 | 37.80 | 10,500 | 3.33% |

| 2015 | 40.82 | 11,025 | 3.24% |

| 2016 | 44.09 | 11,576 | 3.15% |

| 2017 | 47.60 | 12,155 | 3.06% |

| 2018 | 51.40 | 12,763 | 2.98% |

| 2019 | 55.54 | 13,401 | 2.90% |

| 2020 | 59.98 | 14,071 | 2.81% |

| 2021 | 64.78 | 14,775 | 2.74% |

The assumption above is that rents increased by 5% each year. The rental yield is clearly showing a downward trend. The net rental yield would be much lower if you factor in other recurring costs.

EMI is a good example of a recurring cost to calculate net yield. If Ramesh had availed of a home loan of about Rs. 22 lakhs in 2013 and paid an EMI of Rs. 21,000 each month:

| Year | Value of Flat (in Rs Lakhs) | Rent | EMI | Yield |

|---|---|---|---|---|

| 2013 | 35.00 | 10,000 | 21,000 | -3.77% |

| 2014 | 37.80 | 10,500 | 21,000 | -3.33% |

| 2015 | 40.82 | 11,025 | 21,000 | -2.93% |

| 2016 | 44.10 | 11,576 | 21,000 | -2.56% |

| 2017 | 47.62 | 12,155 | 21,000 | -2.23% |

| 2018 | 51.43 | 12,763 | 21,000 | -1.92% |

| 2019 | 55.54 | 13,401 | 21,000 | -1.64% |

| 2020 | 59.98 | 14,071 | 21,000 | -1.39% |

| 2021 | 64.78 | 14,775 | 21,000 | -1.15% |

The net yield turns negative when you factor in the EMI. The only consoling factor is that EMI remains flat and rents may increase, thus improving the yield over some time.

Real estate has been a long-term investment. It may take up to 20 years for property prices to double except in exceptional cases, which are usually rare. If we take that scenario and assume rentals increase by 5% every year, the yield from a property is less than 8%. That is when you have bought the property without a loan.

However, in the example shown above, the property price has appreciated at an average annual rate of 8%. Other than that you cannot dispose of real estate properties whenever you please and rarely in pieces. Finding a buyer can be cumbersome.

On the other hand, if you can invest the amount equal to EMIs in a ULIP with a mix of debt and equity for 20 years and have a yield of 8% p.a. you can easily make Rs 1.4 crores. That too without considering the bonus additions. Not to mention that:

To sum up, real estate is a highly illiquid asset and your returns depend on the city, locality, employment opportunities in the vicinity etc. Equity investments are more flexible and you can allocate your money across different funds in ULIPs. Both investment and returns from ULIPs have tax benefits.

Thus, purchasing a home, whether for residing or rentals, will make more sense after you are retired. You can easily afford the property, save money buying it, and rentals will provide you with an inflation-adjusted income. Even if not, you still have enough corpus left to ensure a lifetime pension.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.