Written by : Knowledge Centre Team

2025-11-02

1192 Views

10 minutes read

Share

Gold is regarded by a majority of the Indian populace as one of the top investment possibilities in India. Gold is not only seen as a reliable long-term wealth generator but also as good fortune and an emblem of social rank in this country. Due to the stock market's significant swings this year as a result of the pandemic's financial consequences, several investors felt compelled to discover ways to safeguard their holdings. During this time, one asset, in particular, began to gain momentum: gold.

Interestingly, a few years ago, fixed deposits were thought to be more attractive financial possibilities for Indians in the middle class. However, because the interest generated on Fixed Deposits has decreased significantly in recent years, FDs no longer appear to be a viable wealth-generating alternative as they once were. People are showing a resurgence of interest in gold investment these days.

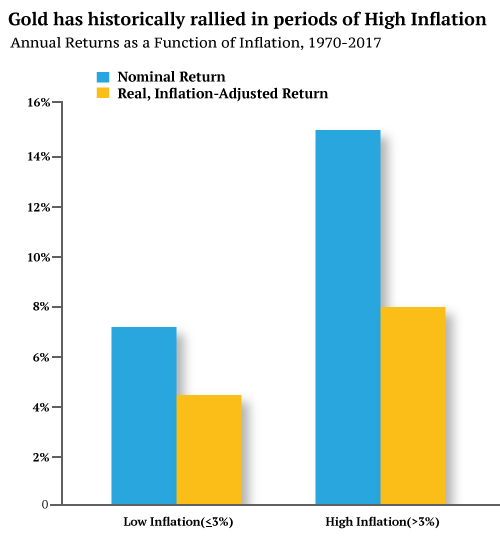

Gold, on the other hand, is a long-term asset that is not ideal for short-term gains. Furthermore, gold prices move in a cyclical pattern. As a result, one cannot expect gold to perform consistently well.

Must Read - What is Investment?

For centuries, Indians were already dealing in gold, and it has shown to be a sound investment. Here are some of the best reasons to invest in gold:

So, purchasing from institutions can be a little complicated because when you're about to sell it, you'll have to go to a jeweler, who likes buying from fellow jewelers due to the way gold trading in India is structured.

If you're considering adding gold to your asset base, we hope this article has given you a better understanding of gold investing. Remember to examine your financial goals, investor's risk, and asset allocation before making any investment.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.