2022-10-04

1087 Views

4 minutes read

Share

An OTP has been sent to your mobile number

Sorry! No records Found

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

No one can plan for your finances in a way that you can do. This is why every person needs to have a solid financial plan that can help you save money and fulfil your set short and long term financial objectives. Apart from this, having a set financial plan can also help you create a better projection of your income and expenses. Financial planning is a step by step process that acts as a guide and helps you reach all your set monetary objectives. It further helps assess all your income and expenditure, so you are always aware of where you stand financially. Also, effective financial planning must include everything concerning your savings, investments, fund flow, debt, insurance and any other components of your economic life.

To help you create a sound financial plan according to your distinct monetary needs and requirements, here is a six-step financial plan that you can consider.

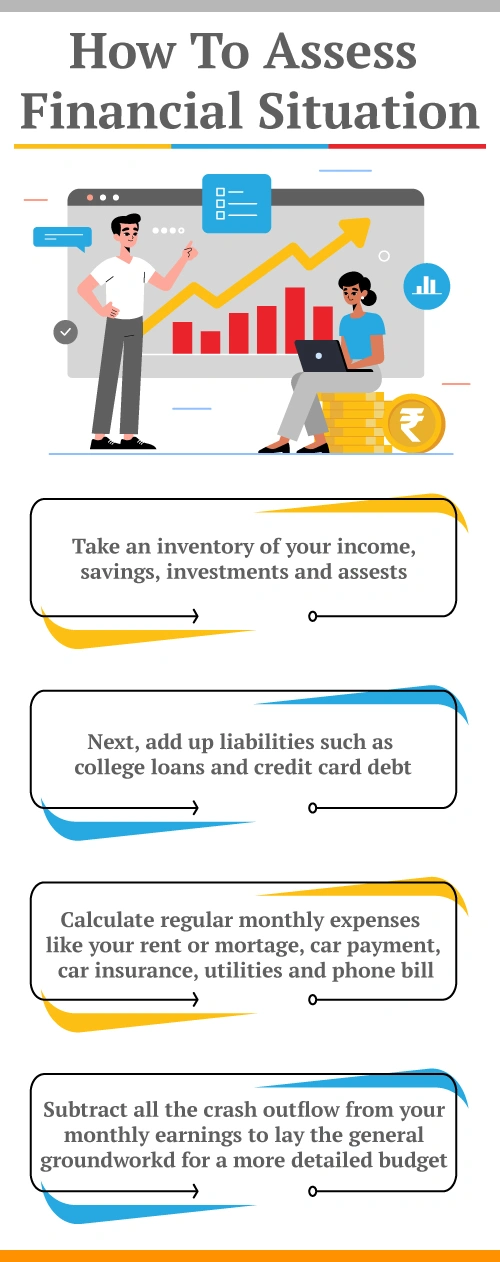

In this initial step of the financial planning process, you should determine your existing financial condition to understand your expense capacity, investment amount, daily expenses, and obligations. Setting up a rundown of current assets and debts and sums spent for different things gives you an endowment for financial planning exercises.

Before creating a financial plan, you should timely monitor your monetary conditions and objectives. This includes getting a solid understanding of your short and long term financial goals after separating your needs from your wants. In addition, explicit financial objectives are fundamental to financial planning. Hence, before creating a solid financial plan, consider your earnings and create a reserve fund that can help you invest your funds properly to meet all your set goals.

Creating alternatives is vital for using sound judgment. Though numerous components will impact the available other investment options, the possible course of action, for the most part, fall into these classes:

1. Proceed with a similar plan of action for your investment

2. Improve your current course of action

3. Switch the prevailing course of action

4. Embrace a new course of action

Not all of these classifications will apply to each of your decisions. However, creativity in financial planning is essential to make rational decisions. Thinking about the entirety of the potential alternatives will help you settle on more fulfilling and feasible choices while creating a financial plan.

In this step, you must evaluate all the available investment options according to your risk-taking capacity and earnings to get higher returns for a long time.

Each financial choice cancels out other alternatives. For instance, an option to invest your entire funds into stock may mean you cannot invest in other saving plans. Opportunity cost is what you surrender here by settling on a decision.

This opportunity cost is usually identified as the trade-off of a decision and cannot get measured in terms of rupees. The Decision-making process will be a continuous segment of your personal as well as economic situation. Hence, you will have to consider the lost opportunities that will occur due to your selected decision.

Risk is a part of every financial decision. However, defining and assessing your risk can be a challenging task. Hence, an ideal approach to consider risk is to accumulate data that project your earnings and risk-taking capacity to create a secured financial plan well-suited to fulfil all your monetary obligations.

Once you get this, you need to make an action plan that can pave the way to accomplish your goals. As you succeed in your immediate or momentary pursuits, the goals next in line will come into the picture.

To execute your financial action plan, you may require assistance from others. For instance, you may utilize the administrations of an insurance company to purchase an insurance plan or services of an investment broker to invest in stocks.

Financial planning is a robust process that doesn't end when you create a specific plan of action. You need to assess your financial choices periodically. Also, your individual, social, and economic-financial components may require more frequent assessment.

When life contingencies influence your financial obligations, this financial plan will work wonders to adjust to those changes. Periodically evaluating this dynamic process will help you make necessary changes to align your financial objectives and activities with your existing life situation.

Click to use : Compound Interest Calculator

A comprehensive financial plan can increase your mental peace by reducing vulnerability about your future monetary requirements and assets. Mentioned here are some significant benefits of financial planning.

To sum up, we can conclude that a solid financial plan can always help you create a better corpus and gain higher earnings on all your made investments. If you are looking for comprehensive investment plans to park your excess funds, take a look at the wide variety of insurance and savings plans available at Canara HSBC Life Insurance. You can do your financial planning with a life insurance plan– that will help you to protect the dreams and aspirations of your loved ones. Along with that it will also assist you to attain your financial milestones on time and effortlessly.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.