Five Components of a Financial Plan

Financial planning is an important aspect of our lives. Buying the best savings plan to boost your financial planning is not the only solution. Here are five components of a financial plan:

1. Goal Identification

You must understand and identify your desires and goals. The efficiency of the plan depends on the clarity of your aims. Listing down your goals might assist you in getting clarity.

- Short-term: Goals that you want to achieve in the next 5 years are considered short-term goals. Settlement of antecedent debts, purchasing luxury or small assets.

- Medium-term: Become an entrepreneur, purchasing property and other goals with a high investment amount that you plan to fulfil in 5-10 years.

- Long-term goals: The period of long-term goals is considered to be more than 10 years. Retirement, education are some of the basic long-term goals.

Goals often sometimes appear to be unachievable. It requires strong planning and clarity to minimize the gap between your goals.

2. Listing Assets and Liabilities

Listing down assets and liabilities gives a clear picture of your current financial value. Products or materials you possess and could bargain to raise capital are considered assets. The property, stocks, jewellery, vehicle, machinery, etc., you own are your assets.

Note that vehicles and machinery are examples of depreciating assets. Liabilities are the debts, mortgage property, and unpaid loans. The three different types of Liabilities are:

- Current liabilities: Debts that are to be settled in a short period, i.e. one year in most cases.

- Non-current liabilities: These are long-term liabilities that are to be paid over a few years.

- Contingent liabilities: Occurring of liabilities depends on the outcomes of events that are to be held in the future. Also, there is an equal probability of the liability to arise depending on the circumstances.

3. Cash Flow and Expense Monitoring

An income statement or bank account statement gives a complete overview of your income as well as your expenses. Cash flow is the amount of money ingressing and egressing your bank account. Salary, return on investment, etc., are some of the permanent forms of income. Temporary or unstructured income are bonuses, rewards, dividends on stocks.

Expense is the amount you are bound to spend; expense can be grouped as necessity and luxury. Setting up the ratio of needs, wants and savings might help you plan structure or cash flow. 5:3:2 is the widely accepted ratio.

Needs include monthly rent, EMI’s, grains and groceries, fuel or travel expenses, repairs, etc. Luxuries are resources that are not on the top of your priority list and are less essential are called luxury. Some of the best examples are dining out, cinema halls, subscription plans.

4. Insurance Planning

A fixed amount of your salary might be considered investment money or an emergency fund. Insurance policies could be the potential assets that would support you in unfortunate and tough times. Selecting the type of insurance policies depends on the goals you are planning to achieve. The most common and popular insurance plans are:

- Term Life Insurance Plan- Term life insurance plans are one of the simplest and affordable insurance plans that you can purchase. The policy covers death risk, and the maturity amount is transferred to the nominee in case of the applicant’s death. The benefits of the term insurance can be stretched via purchasing add-ons.

- ULIP- Unit-linked insurance plans are abbreviated as ULIP. This policy comes with three levels of benefits: insurance coverage, wealth expansion, tax-saving. ULIPs are customizable according to your investment and insurance requirements.

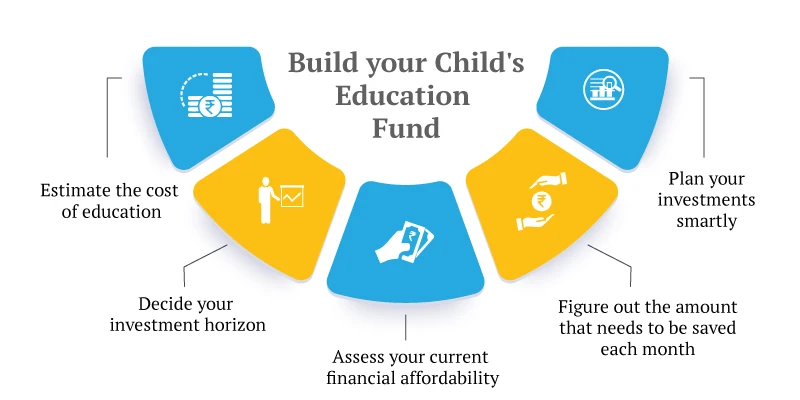

- Child Plan- Being a parent, you might be under constant stress worrying about your child’s future. Child insurance plans cover every stage of your child’s life, from higher studies, foreign studies, weddings, etc.

- Retirement Plan-These insurance policies are your income source after your retirement. They are long-term policies and mature after the age of 65 in India. The payouts of retirement plans can be one time or in parts, i.e. monthly or quarterly. A retirement plan gives you the security to live independently.