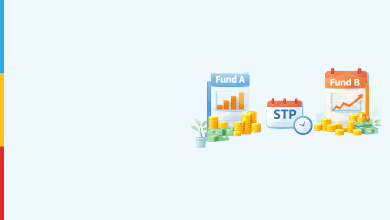

- Systematic Transfer Plan: A facility to transfer money periodically from one mutual fund scheme to another

- Source Fund: The mutual fund scheme from which money is transferred under an STP

- Target Fund: The mutual fund scheme that receives money through the STP transfer

- Rupee Cost Averaging: Investing at regular intervals to average purchase cost across market levels

- Capital Gains Tax: Tax levied on profit earned when mutual fund units are redeemed or transferred

Written by : Knowledge Centre Team

2026-02-28

80 Views

7 minutes read

Share