Written by : Knowledge Centre Team

2026-01-10

1089 Views

6 minutes read

Share

As a working professional, you likely dream of enjoying a comfortable and secure life after retirement. You may even have specific goals, like owning a second home or travelling the world.

All such goals require significant financial resources, making retirement planning essential. A sizeable savings corpus is key to knowing you’re financially prepared.

If you’re unsure about how much money you’ll actually need after retirement, this 10-step checklist will help you calculate it with clarity.

Key Takeaways

|

No doubt, retirement planning involves more than just saving regularly. It requires tracking the gap between what you’ll need after retirement and what you’ve already saved.

If you are confused by the difficult calculations of retirement planning, here’s a comprehensive ready-to-retire checklist. This checklist will help you estimate your financial needs and calculate the monthly investment required to meet your long-term goals.

The first step is to categorise all your monthly expenses into two different heads:

Recurring expenses that continue post-retirement, like groceries, utility bills, home maintenance, and healthcare.

Expenses that end with retirement, such as office commuting costs, formal wear, children’s education, and home loan EMIs.

This exercise helps you understand which costs will stay and which will drop off, so you can plan more accurately, especially for rising post-retirement medical expenses.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Knowing your post-retirement income helps estimate how much you’ll actually need to bridge any financial gap. So, list all the income sources you expect to have after retirement. These could include:

Maturity proceeds from insurance or pension plans

Income from rental properties or real estate

Capital gains from mutual funds, stocks, or other investments

Subtract your expected monthly income (Step 2) from your projected monthly expenses (Step 1). The result is your net monthly requirement, the income shortfall you need to plan and invest for.

Your current income will rise eventually with inflation. Use a conservative long-term inflation rate of around 5% to adjust your monthly retirement requirement from Step 3. This gives you a more realistic target for how much income you’ll actually need in the future.

To estimate your total retirement corpus, consider factors such as your expected lifespan, projected expenses, and average investment returns. Multiply your inflation-adjusted monthly income need (from Step 4) by the number of months you expect to be retired. Younger individuals may need a larger corpus due to a longer retirement horizon, but they also have more time to build it gradually.

Next, calculate the total value of all these income sources to get the figure of your current retirement corpus:

EPF & PPF pay-outs

NPS pay-outs

Bonds

Pension plan pay-outs

Equity gains

Income from Debt funds

Bank deposits

ULIP gains

Insurance policy pay-outs

Other sources

Now, estimate how much your current corpus will grow over time through compounding. This growth depends on how many years you have until retirement and the average rate of return on your investments. For younger individuals, the corpus has more time to compound, leading to potentially higher growth. If your investments are equity-heavy, like a ULIP with a high equity allocation, the compounding effect could be even more significant.

Subtract your projected corpus value from Step 7 from the total retirement corpus required as per Step 5. The difference is the additional savings corpus you still need to accumulate before retirement.

Click here to use:- Retirement Calculator

Based on the value ascertained in Step 8 and your regular expenses, you can determine how much you need to save each month until retirement. This will help you systematically build the additional corpus required to meet your goals.

Finally, you need to add up all your ongoing retirement investments, including SIPs, pension plans, ULIPs, and other savings. Subtract this total from your monthly savings goal calculated in Step 9. The remaining gap is the additional amount you’ll need to start investing regularly to meet your retirement target.

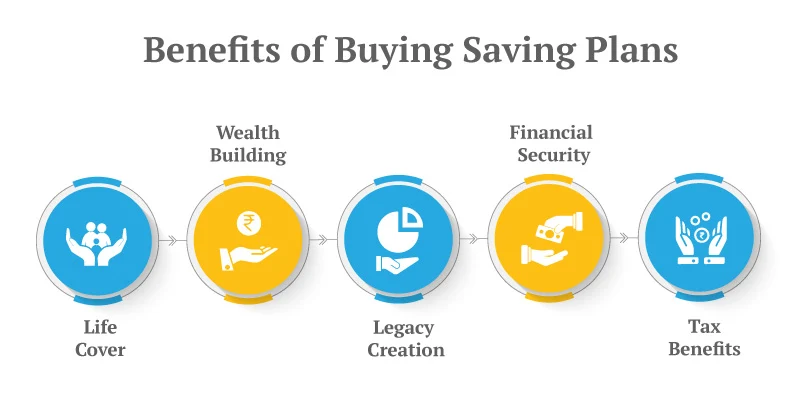

Planning your post-retirement life requires financial tools that offer guaranteed income and long-term security. Here are two retirement plans that can help you build a stable future:

Retirement planning can feel overwhelming at first, but with a structured approach and timely action, it becomes much more manageable. By calculating your future expenses and building a suitable savings corpus, you can take control of your financial future. The 10-step method shared above offers a practical way to assess your readiness.

To support your journey, Canara HSBC Life Insurance provides retirement plans that offer guaranteed income, protection, and flexibility. Start today to enjoy financial freedom and peace of mind in your post-retirement years!

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.