Written by : Knowledge Centre Team

2026-01-10

890 Views

5 minutes read

Share

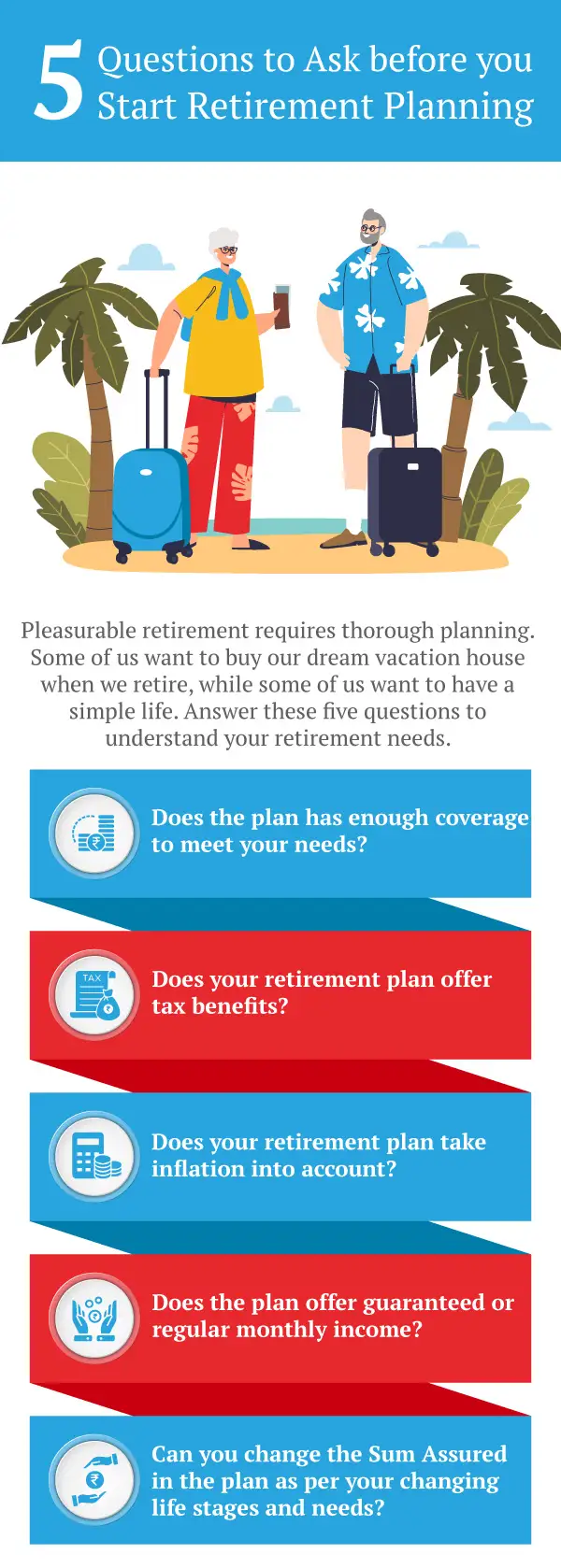

Retirement is all about securing a lifestyle you’ve always dreamed of. If you envision any goals like peaceful days in the hills, pursuing hobbies, or spending quality time with your loved ones, having the right retirement plan in place is crucial. With rising costs and longer life expectancy, early and smart retirement planning can make all the difference.

Today’s professionals no longer rely solely on pensions. Instead, they seek flexible, growth-oriented retirement goals and plans that align with their life goals. The key question on every millennial's mind is How much do I need to save to retire comfortably? This blog explores the answer through a practical case study, explains key investment options so that you can you are secure your retirement phase easily.

Key Takeaways

|

Based on your annual income, you can easily figure out how much retirement savings you need for a comfortable life. You need to chalk out a plan to save a part of your annual income into a savings plan that can yield sufficient returns at the prevailing ROI.

To better understand how to save for retirement, you can refer to the case study given below:

Varun is a 30-year-old finance consultant working in a leading fintech concern based in Delhi. He is earning an annual package of ₹12 lakhs. His ambition is to buy a small plot of land in Dehradun and build a luxury villa, and live a comfortable retirement life over there. No doubt, he requires a lot of savings to fulfil his dream.

Taking into account the prevailing return on investment, i.e., 8%, if Varun’s income is increasing at the rate of 5%, there can be 3 different scenarios:

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Based on the risk appetite, you may opt for one of the following types of retirement investments:

Note: Tax benefits are subject to change in tax laws. Please consult your tax advisor.

Retirement planning goes beyond saving and calls for smart investment choices aligned with your future goals. You can choose guaranteed income, market-linked returns, or tax-free withdrawals based on your needs. Canara HSBC Life Insurance offers flexible plans like Promise4GrowthPlus and iSelect Guaranteed Future Plus to help you build a secure and comfortable life after retirement. Start early to make the most of your savings journey.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.