Written by : Knowledge Centre Team

2025-11-02

902 Views

8 minutes read

Share

Tax-savings play a very important role in meeting your future financial goals. But, many of us leave it for the last few months of the financial year, which is not a prudent behaviour. A poor tax planning strategy would make it difficult for you to meet your financial targets on time. Thus, if you haven’t done your tax savings yet, then listed below are 6 popular tax-saving instruments that will help you plan your taxes well in 2025

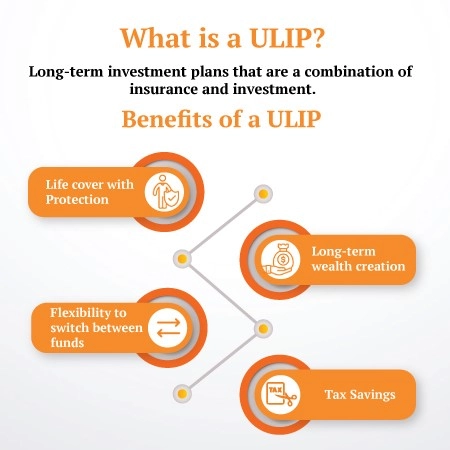

1. Unit Linked Insurance Plan - ULIPs have now become a popular investment option due to its flexibility, low cost, and tax-free returns. Unit Linked Insurance Plan is a market-linked insurance plan that comes with a lock-in period of 5 years. Furthermore, this insurance-cum-investment product is eligible for deduction as per Section 80C of the Income Tax Act. Deciding to invest in the best ULIP is wise as it offers you a life cover along with an investment avenue, where you can expect returns.

2. Public Provident Fund - Though interest rates are low, but PPF offers tax-free guaranteed returns. This is a long-term investment option that helps you avail tax benefits. The current interest rate for PPF is 7.1% and it comes with a lock-in period of 15 years. As compared to other bank deposit options, PPF is a much better option because the interest rates are tax free.

3. Tax-saving FDs - This is yet another best tip that will help you save on taxes. Though they rank low on returns it is the simplest way to save tax. The interest rate you get is as per the prevailing FD rates. Also, tax-saving FDs come with a lock-in period for 5 years which means you cannot withdraw your money before 5 years. You will only make a one-time lump sum payment. No premature withdrawals are allowed. In addition to this, tax-saving FDs are also good for those who plan their taxes at the last minute.

4. Senior Citizen Savings Scheme - This risk-free tax-saving instrument is an ideal option for those who have already retired or are going to retire soon. Senior Citizen Savings Scheme (SCSS) comes with a lock-in period of 5 years and is the best option for retirees. Also, the interest earned from the scheme is tax-free, which makes it one of the best tax-saving options for senior citizens.

Read about the top investment options for retirees.

5. National Savings Certificate (NSC) - The best part about the National Savings Certificate (NSC) is that the interest earned is eligible for tax deduction. This fixed-income investment option also comes with a lock-in period of 5 years with the current interest rate of 7.1%. This used to be one of the popular investment options, but not now as many bank fixed deposits have come under Section 80C.

6. Life insurance - This is considered as a default tax-saving instrument by investors Although this purpose is best served by term insurance policy as other life insurance policies such as endowment plans or ULIP offer poor returns at high premiums. On the other hand, a term insurance plan offers life coverage along with tax benefits. It allows you to avail tax deductions as per Section 80C of the Income Tax Act. Buy the best life insurance plan to suit your financial requirements and goals.

These are some of the pragmatic tax-saving tips that you should find very useful. Besides, if you are looking forward to buying an adequate insurance plan that also helps you save on taxes. iSelect Smart360 Term Plan allows you to enjoy tax benefits of up to ₹ 1.5 Lakh/annum on the premiums paid towards the policy as per Section 80C of the Income Tax Act.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.