2021-09-30

875 Views

Share

An OTP has been sent to your mobile number

Sorry! No records Found

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

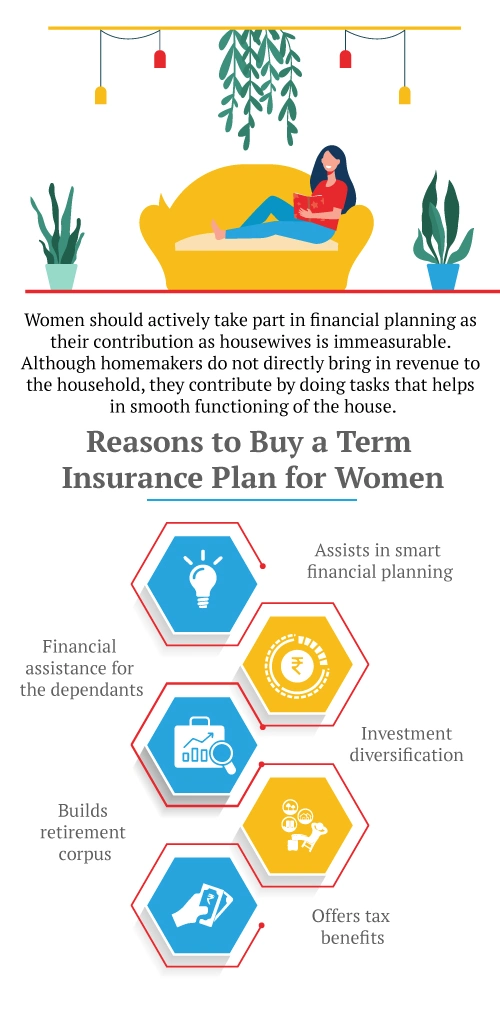

In the present upsetting and dubious world, anything can occur whenever. The degree of hazard is very high, and an individual's wellbeing is in question. Normally, working experts are covered by the protection given by their separate organizations. In any case, having a term insurance plan for a non-working spouse is similarly significant. There is no motivation to feel that they are protected since they stay back at home. They are similarly presented to pressure while doing the day by day errands.

A term insurance plan usually ensures a risk-free life for the family members, in case of an early or sudden demise of the earning member. A large sum of money will be provided to the family members, which will aid in paying off the bills, clearing debts or fulfilling other monetary obligations. You are required to pay a certain amount either periodically or lump sum, which will add up to a protective coverage for you and your family.

Remember that the term non-working spouse refers to the companion who deals with the home and related issues. Using any and all means, they are not "non-working". Along these lines, it is fundamental to furnish them with a protection plan, very much like their accomplice. Underneath given are some more reasons concerning why one ought to put resources into such an arrangement.

The degree of inclusion normally relies upon the pay of the functioning life partner. Apart from buying an individual term insurance policy, one can settle on an arrangement remembered for the term insurance of the functioning life partner. All in all, there will be a solitary joint protection plan for both, with lower premium rates.

The premium is usually decided based on age, employment, and several other factors. With iSelect Smart360 Term Plan, get whole life cover online at affordable prices.

While choosing the measure of inclusion, one should think about loads of components. Initially, recollect the exorbitant world we are living in, where costs are expanding every day. Also, your mate is indispensable, thus don't consider setting aside cash at the expense of a significant individual from your life. The bare minimum value should be that of five years income replacement. The coverage of your spouse must be sufficient enough to meet your child’s needs and other expenses.

Click to use : Term Insurance Calculator

There have been various protection misrepresentation cases since the purchaser didn't go through the agreements or was tricked by some phony protection supplier. Accordingly, remember the underneath recorded focuses prior to buying any plans.

There is a wide range of life insurance policies offered by Canara HSBC Life Insurance. Secure and protect the financial future of your loved ones today!

Also Read : What is the meaning of Term Insurance

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.