- Term Insurance: A life policy offering coverage for a set period, paying a death benefit if the insured passes away during the term.

- Nominee: The person entitled to receive the claim benefits.

- Premium: The amount paid periodically to keep the policy active.

Key Takeaways

|

What Do Term Insurance Plans Not Cover?

A Term insurance provides financial protection to your family in case of any unfortunate eventuality. As a beneficiary, your wife, parents or children can receive a lump-sum death benefit in case of demise of the insured during the policy tenure. Even though term plans are among the most affordable and rewarding insurance options one can have, it is better to have complete knowledge about the kind of deaths that are covered under a policy, and also those that are not covered. It is always beneficial to be aware of the terms and conditions of the term insurance policy, to ensure there are no unpleasant surprises waiting for your family members or dependents, when they are already in stress. Term plans are best suitable for planning short to medium term goals. Let’s see what kinds of deaths are typically not covered in term insurance plans in India:

- Death due to driving under the influence of alcohol

- Death due to a pre-existing health condition

- Accidental death due to driving under the influence of drugs

- Death due to the participation in adventure sports

- Death due to the participation in racing events

- Death due to pregnancy and childbirth

- Death caused due to the participation in illegal activities

The above mentioned are certain lifestyle influenced exclusions in a term insurance policy. It is important that you mention about your smoking and drinking habits, if you happen to have them, at the time of application of the policy. Following which an insurance company will typically assess the risk of death due to these habits and may charge an additional premium for the cover. However, hiding the information can lead to problems at the time of claim settlement, causing trouble to your family. And in case the information is revealed after application, the company may cancel your policy.

Also Read - Term Plan Meaning

Apart from these previously mentioned pointers, there are some other conditions that are mostly not cover by a term policy:

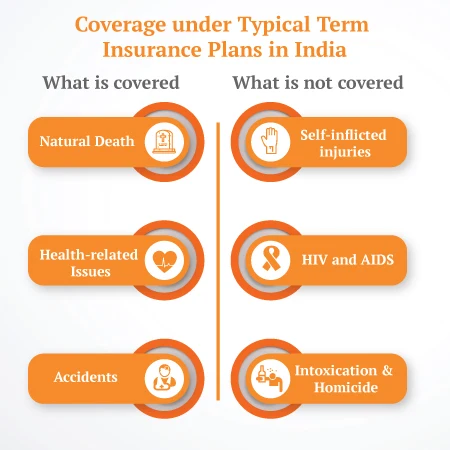

- Self-inflicted injuries: If the cause of death is participation in a hazardous adventurous activity leading to self-inflicted injury, the claim might be rejected by the insurance company.

- HIV and AIDS: Insurance claims made against death due to sexually transmitted diseases like HIV or AIDS are not admissible by the insurance company.

- Natural disasters: Deaths that caused by natural disasters are not covered by the life insurance company. However, there are often riders available to cover these instances.

- Intoxication: Any death that takes place due to the consumption of drugs or alcohol is not admissible and the company has the right to reject its claim.

- Homicide: If the policyholder dies due to a murder, the insurance company has the right to put the claim on hold until the acquittal of the nominee. In case the murder is committed by the nominee, the insurance company will reject the death claim.

In cases where certain hazardous life conditions are predictable by the policy holder, insurance companies may offer riders and additional coverage options. It is advised you flourish all information at the time of buying of the policy. Also, if there is a change in lifestyle after allotment of the life insurance policy, the policyholder should ideally share the information with the insurance company to ensure efficient coverage and easy claim settlement, when the time comes.

Any natural death or death due to health-related issues will be covered by insurance plans in India. With critical illness covers, in case of death of the policyholder due to a critical illness or medical complication, the beneficiary will receive the sum assured as the death benefit. Most term plans also provide coverage in case of death of the insured due to an accident or disability caused by an accident. Moreover, term policies also offer the option of choosing from a variety of additional benefits that promise additional sum assured for specific uses like child education.

Protect Your Family with Affordable Term Insurance

Enter OTP

An OTP has been sent to your mobile number

Didn’t receive OTP?

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder as on

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Sorry ! No records Found

Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Death within First 2 Years of the Policy Term:

For any term life insurance plan, in case an unfortunate event takes place within the first two years of the policy term, the case is considered under Section 45 of the Insurance Act, 1938. It states that the claim will firstly be investigated for fraud, including improper disclosure of information or even misrepresentation. However, after 2 years no claim can be denied on the basis of these grounds. Therefore, the importance of being honest and presenting the correct information with your insurance company cannot be emphasized enough.

The iSelect Smart360 Term Plan by Canara HSBC Life Insurance is ideal for those who have big plans in life and need an insurance cover as flexible as their needs. The plan offers you flexibility to Increase you’re your cover aligned with changing life stages and protection needs at key life milestones, in addition to inbuilt benefits for Accidental Death, Child Support, and Accidental Total and Permanent Disability.

Did You Know?

Denial rates have increased over the last five years, rising by more than 20%, leading to prolonged financial stress for families.

Source

Steps to File a Term Insurance Claim

Filing a claim should be a hassle-free process. Here is the step-by-step guide one can follow:

- Notify the Insurer - After the insured person dies, the insurer must be informed as soon as possible.

- Gather Required Documents - This may include the original policy document, death certificate, medical records (if applicable), and identity proof for the nominee.

- Complete Claim Form - The nominee must fill out the claim form and forward it to the insurer.

- Follow Up on the Claim – Stay updated on the claim status and respond promptly to any additional requests from the insurer.

- Wait for Claim Processing - The insurer will verify the details before processing the claim. If everything is in order, the insurer will settle the claim in a few weeks.

Conclusion

While term insurance provides financial security, policyholders must understand what is excluded from coverage. Being aware of potential claim rejection reasons can help avoid unpleasant surprises for beneficiaries. Always ensure transparency while purchasing the policy and pay premiums on time to keep the coverage intact. By doing so, one can safeguard their family's future without unnecessary complications.

Glossary

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Recent Blogs

Does Term Life Insurance Cover Disability? Know the Facts

07 Aug '26

942 Views

10 minute read

Wondering if term life insurance covers disability? Get a complete breakdown of disability coverage, riders & options available under term plans today.

Read More

Term Insurance

7 Things to Expect From Your Term Insurance Plan - Key Features

07 Aug '26

4904 Views

7 minute read

Discover 7 things to expect from your term insurance plan. Learn key features, coverage details, benefits and what matters most before you buy

Read More

Term Insurance

Term Insurance for Diabetics in India: Eligibility & Benefits

07 Aug '26

909 Views

6 minute read

Yes, diabetics can get term insurance! Explore the best term plans for diabetes with Canara HSBC Life Insurance. Read more to learn about eligibility and benefits.

Read More

Term Insurance

Types of Death Covered and Not Covered in a Term Insurance

07 Aug '26

1699 Views

8 minute read

Before buying term insurance, know what types of death are covered & excluded. A complete breakdown of inclusions & exclusions under term plans in India.

Read More

Term Insurance

Decreasing Term Insurance Plan - Meaning & How It Works

07 Aug '26

1202 Views

7 minute read

Not many know about decreasing term insurance plans. A clear breakdown of what it is, how it works, key benefits & who it is best suited for in India.

Read More

Term Insurance

Impact of Travel to High-Risk Countries on Term Insurance Premium

07 Aug '26

719 Views

6 minute read

Wondering how international travel affects your term insurance cost? Understand how visiting high-risk or conflict-affected regions influences premiums and policy approval.

Read More

Term Insurance

How Mental Health History Affects Term Insurance Eligibility in India?

07 Aug '26

417 Views

6 minute read

Understand how a history of mental health issues impacts eligibility for term insurance in India. Learn disclosure rules, insurer evaluation, and tips to improve approval chances.

Read More

Term Insurance

Term Plan for India's Non-Working Spouse

07 Aug '26

2762 Views

11 minute read

Discover the significance of a term plan for an Indian spouse who is not employed. Protect loved ones, provide for future needs, and guarantee the family's financial stability.

Read More

Term Insurance

How to Calculate Your Term Plan Premium Easily ?

07 Aug '26

2813 Views

6 minute read

Use a term insurance premium calculator to estimate your term plan cost. Learn how premiums are calculated and factors that affect what you pay.

Read More

Term Insurance

Term Insurance - Top Selling Plans

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.

Family Shield: Enhanced Protection

iSelect Smart360 Term Plan

- 3 Plan options

- Life cover till 99 years

- Steady income benefit

- Block your premium at inception

Start Young, Pay Less, Stay Secured

Young Term Plan

- Life cover till 99 years

- Coverage for spouse

- Block your premium rate

- Covers 40 critical illness

Family Shield: Enhanced Protection

Saral Jeevan Bima

- Affordable prices

- Multiple premium payment option

- Get Tax benefits

- Hassle-free purchase process

Popular Searches on Term Insurance

- Types of Term Insurance

- Buy Term Insurance Online

- Term Insurance Plan

- 1 Crore Term Insurance

- 2 Crore Term Insurance

- 5 Crore Term Insurance

- Term Insurance for women

- Term Insurance Calculator

- Term Insurance for Housewives

- Term Insurance Tax Benefit

- Term Plan with Return of Premium

- 50 Lac Term Insurance

- Zero Cost Term Insurance

- Temporary Total Disability

- Buy Term Insurance Online

- What is Term Insurance?

- Term Insurance for NRIs

- 10 cr Term Insurance

- Term Insurance for Senior Citizens

- Spouse Term Insurance Plans

- Term Insurance for NRI

- Accidental Death Benefit