2025-02-02

898 Views

5 minutes read

Share

Financial management during a disability is crucial to ensure a stable income and savings to rely on. It's important to prioritise essential expenses and build an emergency fund beforehand, which can ease the pressure.

This is where disability insurance steps in to lend a strong layer of protection. From making home modifications and adjusting daily routines to managing new commuting needs, these changes can lead to unexpected costs. In more serious cases, you may even need to take a break from work or explore a different career path altogether.

Therefore, to ensure your financial stability, different types of disability insurance are available.

Let us learn more about how you can focus on recovery with thoughtful planning and the right coverage.

Key Takeaways

|

A person is disabled when they have a mental or physical impairment, and the impairment has a substantial effect on their ability to carry out day-to-day activities. This can result in temporary loss of income, reduced income, or permanent financial dependency. Disability insurance is a protection against the above financial situations.

Since you cannot do your daily activities, you also won't be able to go to work. Based on the type of disability insurance, what coverage can do for you is:

Replace a portion of your income when you are unable to work because of disability, or

Pay a lump sum amount so that you can meet your medical and household needs

The monthly income helps you meet your regular financial needs and maintain your current lifestyle, while the lump sum is useful for the treatment and other large liabilities.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disability insurance comes in different forms to match various needs and life situations. They offer a unique way to protect your income when illness or injury prevents you from working. The two main types of disability insurance are:

Insurers classify disabilities based on the magnitude of the impact it has on your regular and earning activities. Below are the different types of disabilities classified in insurance plans:

| Disability Insurance – Type | What is it? |

| Accidental Disability Insurance | A disability that arises due to an accident is covered under these insurance plans. Under this, you get a certain percentage of the sum covered depending on your insurance plan. |

| Critical Illness Insurance | These plans provide a wide range of cover against specific life-threatening diseases like cancer, stroke, kidney failure, etc that impact your day-to-day work. |

| Short-Term Disability Insurance | These cover you for a limited time. The waiting time for most short-term disability insurance is 14 days, and benefits are limited to a maximum of two years. You continue to receive benefits until you have recovered or exhausted the coverage amount. |

| Long-Term Disability Insurance | Under this insurance plan, you can continue to receive benefits for a few years or your entire life. The waiting period can be a few weeks to months. |

When you opt for disability insurance, you get cover for disabilities as per your disability plan. The disability insurance works as below:

There are many options when it comes to selecting disability insurance. The first step is to assess your situation. Before buying disability insurance, consider your liabilities and evaluate your family's financial situation. Based on the data, determine the appropriate coverage level you will need, and then start to look for disability insurance.

Below are a few things you should look for in a disability insurance plan:

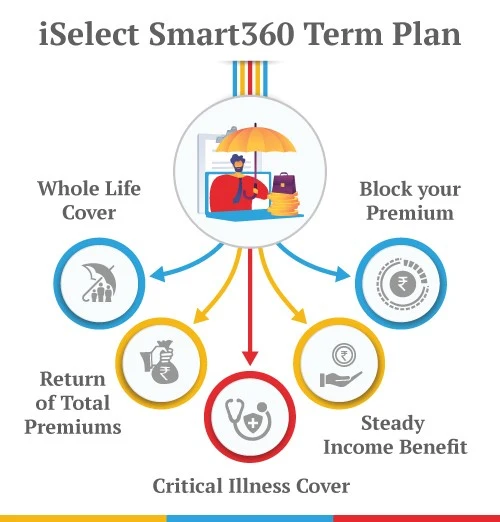

iSelect Smart360 Term Plan by Canara HSBC Life Insurance is an online comprehensive term insurance plan that offers life cover till 99 years, along with disability cover. Future premiums will be waived off if the policyholder is diagnosed with a critical illness or in case of accidental total and permanent disability, if opted for.

Having adequate insurance, like term and health insurance, is a must for your savings plan. However, there are specific life events that can completely overtake your planning. Hence, it is essential to consider insurance coverage for specific situations..

By understanding the types of disability insurance, you can begin investing a small amount in these insurances. They help you with solid financial safety for your loved ones and enable you to enjoy your life without worrying about unexpected life events.

To make that sense of security even more real, you can explore our insurance plans. With thoughtfully designed plans that include critical illness and disability coverage, at Canara HSBC Life Insurance, you are building a future where uncertainties do not take centre stage. Let your financial strategy reflect the same care you have for your loved ones.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.