Written by : Knowledge Centre Team

2026-07-30

1095 Views

8 minutes read

Share

There are many benefits of being your own boss. You get to make all sorts of choices for yourself and your work. However, there are many risks and challenges of being self-employed. You may have a family to take care of, and with no fixed guaranteed income, it could be challenging at times.

Also, you do not have savings schemes like the provident fund to secure your future and group health plans to provide you coverage during medical emergencies. For these reasons, self-employed people must make additional efforts to protect themselves and their loved ones from life's uncertainties.

Key Takeaways

|

Disability Insurance is an insurance cover that offers financial support in case you suffer from a physical disability. Disability for the insurance has been defined as follows:

Loss of one or more limbs, i.e., hands, arms, feet, or legs.

Loss of a sensory capacity, for example, hearing, speech, and vision in one eye or both.

Disability can happen due to an accident or medical reasons, and can be permanent or temporary. A comprehensive disability cover will cover most disabilities.

Also Read - Short term vs Long term Disability Insurance

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disability insurance is an important safety cover for the self-employed. While you may enjoy the freedom and flexibility that comes with working for yourself, life can take an unexpected turn. Imagine meeting with an accident on your way back from a client visit and injuring your arm or leg. Suddenly, you're unable to work, and your income stops, even as expenses continue to pile up.

As a result, you cannot work, and your income flow stops. At the same time, your medical bills will continue to rise, and your regular financial obligations will not wait. It is a tricky situation to face.

You can effectively manage such a situation with a Disability Insurance cover. Disability Insurance can help you:

Secure yourself and your loved ones.

Cover essential living expenses during recovery.

Relieve financial stress so you can focus on healing.

Benefit from tax deductions on the premiums paid.

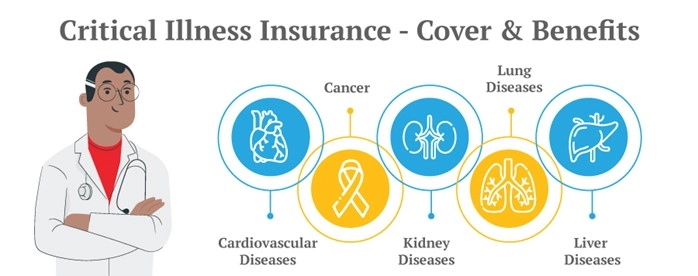

You can avail of disability insurance cover under accidental cover and critical health insurance covers. Both of these covers are available as riders and as standalone policies.

The best way to have these covers is to add them to your term life insurance cover. This way, they are more manageable, and you can avail of additional benefits too.

You cannot predict the future, but you can prepare yourself for unexpected life events by having different insurance as a self-employed individual. Below are some of the must-have insurance covers for the self-employed:

As a self-employed individual, you can solidify your financial safety by incorporating the following practices in your journey:

Being self-employed comes with unmatched freedom, but it also brings significant responsibilities. From running your business and managing household expenses to planning for future uncertainties, you juggle many roles each day. And when you are handling everything on your own, having a financial safety net becomes essential.

One practical way to enhance this security is by selecting a term insurance plan that allows you to pay the death benefit as a regular income instead of a lump sum. This can help your family manage ongoing expenses comfortably, without the pressure of handling a large payout all at once.

Whether you are a freelancer, an entrepreneur, or running a small setup, protecting yourself does not have to be complicated. By making timely decisions about insurance, renewing plans on schedule, and paying your premiums regularly, you can secure both your present and your future.

Stay mindful and take simple steps to protect the life you are building.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.