Written by : Knowledge Centre Team

2025-11-07

1187 Views

11 minutes read

Share

Term insurance is an economical way to financially safeguard your family with a huge corpus irrespective of what life has in store for you. The family can still survive and children can continue education as you had planned and envisioned.

Even though you may be diligently saving month-on-month, savings can evaporate when there are financial and health emergencies. Having a comprehensive term insurance policy that gives a guaranteed sum assured and additional benefits in case of accident or total permanent disability is highly recommended. Therefore, life insurance should also find a place in your portfolio in addition to bank deposits, gold, equities, bonds, real estate and other asset classes.

A joint insurance plan covers two individuals under a single policy and is designed to cover couples. This plan pays the sum assured on the death of either of the two insured and, in some cases, regular income to the surviving partner.

Assume Mrs and Mr Kini purchased a joint life insurance policy. The convenience of covering both partners in one policy and ease of managing the policy made the couple opt for a joint term plan. Mr Kini, the family's lone income earner, has chosen a sum assured of Rs. 50 lakh. Mrs Kini is eligible to receive Rs 50 lakh from the insurer if Mr Kini dies within the policy's term.

Just like a regular term plan, you and your spouse pay a premium for a specific period to remain jointly covered under the policy. At any point, if either of you, unfortunately, passes away, the sum assured would be paid to the other. However, joint life insurance has a few advantages over two individual policies.

A joint life insurance policy is better suited for married couples because it turns out to be cost-effective in the long run. If one of the partners dies, the surviving spouse can claim the full sum assured. The policy remains in force and the surviving spouse is exempt from paying future premiums.

| Criterion | Joint Term Plan | Individual Term Plan |

|---|---|---|

| Coverage | A single policy covers both | Individual policy for each |

| Sum Assured | Based on the combined income of both | Based on individual income |

| Death-Either | Pay-out will be made to the surviving partner. Policy continuance depends on the type of plan | Sum assured paid to the nominee and the policy terminates. The surviving partner is covered under his/her plan. |

| Death-Both | If both partners die, the sum assured will be provided to the nominee | The sum assured in each policy is paid to the respective nominee |

| Premium Waiver | Premium waived for the surviving spouse after the death of one | No premium waiver for surviving spouse the policy continues as is |

| Cover for Homemaker Spouse | Available with a reduced sum assured | Not available to non-working/earning individuals |

Your investment portfolio would anyway have multiple FD Receipts, a PPF Account, NPS Account, Gold, Real Estate etc. Managing multiple insurance policies will only add to your woes. Why not simplify by availing of a joint-life policy?

With volatile markets, redundancy of jobs, the emergence of newer illnesses and the rise of nuclear families, you must plan for all situations. People work on gigs, stay home to manage the household or move places for better opportunities. The Sum Assured on a term insurance policy is calculated basis the Human Life Value (HLV) which is estimated to be around 15times the person’s annual income.

The joint-term plan benefits are useful in case either of you plans to become a stay-at-home parent until your child grows up. The Sum Assured is payable in case of unfortunate demise of either parent.

Conventional policies frown to offer life cover to a non-working person.

The iSelect Smart360 Term Plan offered by Canara HSBC Life Insurance is designed to fit your unique needs for your family’s safety. The joint term plan makes the combined policy cheaper than buying two separate policies. Another unique feature is the return of premiums option which gives you more peace of mind because you know you will not only get protected but also get all the money back. Additional riders to cover accidents, disability etc make the policy an all-around protection plan.

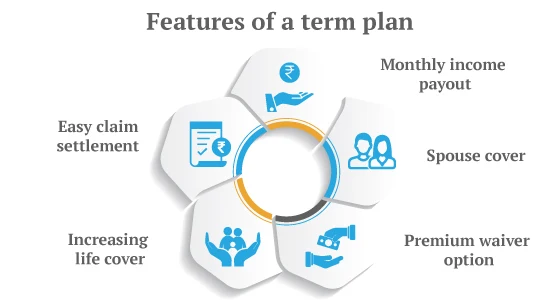

Some of the features which make this plan unique and extremely helpful as joint life policy are:

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.