Written by : Knowledge Centre Team

2025-08-13

2887 Views

8 minutes read

Share

Everything is planned and going on as per plan. You married at 27, had 2 kids by 30, and purchased a flat at 31. You go on vacation every year and are also planning for your children’s careers even as you climb the corporate ladder to earn more name, fame, and wealth. All is well until everything is well in the jigsaw puzzle of life. What if one piece of this puzzle goes missing? What if that piece is you?

Household appliances have guarantees, but, unfortunately, life has no guarantee. But life insurance is one instrument that can help your family cope up with the bills and strive to attain the goals that you had set. Life insurance, especially term life insurance, is a guarantee that your family will have money in the bank even though the emotional loss is irreplaceable.

Term life insurance provides insurance coverage for a specific period and ergo, the phrase “term insurance”. In case of unfortunate demise during the term period, the beneficiary is given the “Sum Assured”. Term insurance is availed by paying a fixed amount, at pre-defined intervals, called premiums. Premiums have to be paid, without fail, to avail of the full benefits that are offered under any insurance policy.

Learn how does a term insurance plan work.

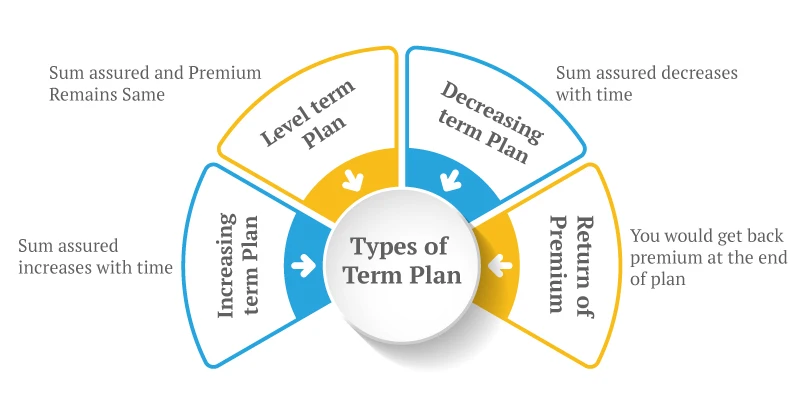

Depending on the type of term cover you had, you may face any one of the following situations:

The second option is possible when you buy a term plan with a return of premium option. For example, if you buy a 20-year Term cover of Rs. 1 crore, with the return of premium option and your premium is Rs. 20,000 p.a., you will receive Rs. 4 lakhs at the expiry of the plan.

Premiums are calculated basis the person’s health, age, health condition, and Sum Assured. A health check-up may be triggered depending on the level of risk assessment. Premiums are fixed and payable for the entire length of the policy term. In case of unfortunate demise before the policy expiry date, the nominee gets the Sum Assured, also called the Death Benefit.

In case of demise after the policy expiry date, the Sum Assured may or may not be paid depending on the terms and conditions of the specific policy. You can renew or buy a new term insurance policy if the insurer’s rules allow; however, the new premium will depend on the age and health at the time of renewal.

When exploring term insurance plans, you must go for the one that meets your needs and life circumstances. Some insurance companies may provide coverage until the age of 99 whereas others may offer coverage only until 75.

The length of tenure of a term insurance plan is as important as the Sum Assured amount offered. If your family does not get the money because of the age criterion, the entire purpose of availing of a policy is defeated.

| Age | Recommendation |

| In your 20’s | If you are single and do not have any financial dependents, you can save money in investment plans instead of putting in term plans. However, if you do, you must look at a minimum term of 40 years and preferably until the age of 99 |

| In your 30’s and 40’s | You must look for a minimum term of 30-40 years and preferably until the age of 99 |

| In your 50’s and 60’s | Your children would be financially independent by then. Focus on getting a plan that can support your spouse in your absence. A term of 20-30 years is recommended. |

Canara HSBC Life Insurance’s iSelect Smart360 Term Plan is a robust and comprehensive policy covering the most probable scenarios as listed below:

This is the most fundamental option if you have just set out on your journey to explore life insurance products.

For example, Mr Ramesh, aged about 40 years, is comparing term life insurance plans. His wife Rashmi, 37 years, is also keen to have her policy. Both can opt for separate policies and on one’s demise, the other would get the Sum Assured. In iSelect Smart360 Term Plan, Ramesh and Rashmi can opt for a joint policy which will be cheaper than buying two separate individual policies.

Both death and terminal illnesses are covered under this option. If Ramesh is diagnosed with a terminal illness at 45, the Sum Assured would be paid to Rashmi and the policy will close. If Ramesh is hale and hearty until the maturity of the policy, all the paid premiums would be returned to him, but the policy would continue until Ramesh attains 99 years of age. At the age of 99, Ramesh would get the Sum Assured, and then the policy would cease.

If Ramesh, aged about 40 years, dies before completion of the policy term, his spouse Rashmi would get the Sum Assured. However, if Ramesh outlives the policy term, all the paid premiums would be returned to Ramesh.

Learn about term insurance plan with return of premium.

iSelect Smart360 Term Plan, offered by Canara HSBC Life Insurance, comes with a plethora of options to meet the diverse needs of different types of people and at an affordable cost. Some of the salient features:

Thus, you should choose a term plan as per your objective at the maturity of the plan. The difference between the benefits of these plans also affects their cost. However, it’s only a fraction of the benefit amount.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.