Written by : Knowledge Centre Team

2025-12-05

2202 Views

8 minutes read

Share

In today's unpredictable and fast-paced life, no one knows what might happen at the next moment. This makes it imperative to think about your loved ones' future. For the safety of your family and securing their life, it is important to buy the best term insurance plan, which will act as a financial cushion in the future. A term insurance plan provides the policyholder with financial coverage for the policy term and offers financial security to their beneficiary in the event of the policyholder's demise during the policy term. The monetary amount to be received by the beneficiary will be according to the plan that you select.

While the core function of term insurance is to provide death benefits, many people wonder about the kind of deaths it covers, particularly accidental deaths. Does your standard term plan provide coverage for accidents? Are there exclusions? And what role do riders play in this context? If your mind ever crossed these questions, then you are on the right page. This blog explores everything regarding the insurance for accidental death. Keep scrolling to dive deeper into the details.

Key Takeaways

|

A standard term insurance plan provides a death benefit if the policyholder passes away during the term. But the nature of the death, like natural, accidental, or otherwise, can impact the payout.

Yes, most term insurance plans do cover accidental deaths. An accident is defined as an unforeseen, involuntary, and sudden event leading to death, typically within 90 to 180 days of the incident. Examples include:

However, accidental deaths resulting from high-risk activities like adventure sports (e.g., skydiving or bungee jumping) or willful negligence may not be covered unless you’ve opted for specific riders.

The payout and benefits of every life insurance policy you buy depend on the cause of the policyholder's death, among other things. These conditions may sometimes vary according to the company in question or the chosen plan.

All these details are clearly stated in your policy, and this is why you should always read the papers stating the terms and conditions before buying a life insurance plan and also share all these details with your nominee so that at the time of claiming the insurance payout, they are saved from any hassle and confusion.

The following list is an overview of the types of deaths that a typical term life insurance plan does and does not cover:

The following are the causes of death that are typically eligible for a term insurance payout:

The following are the causes of death that are typically not eligible for a term insurance payout:

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

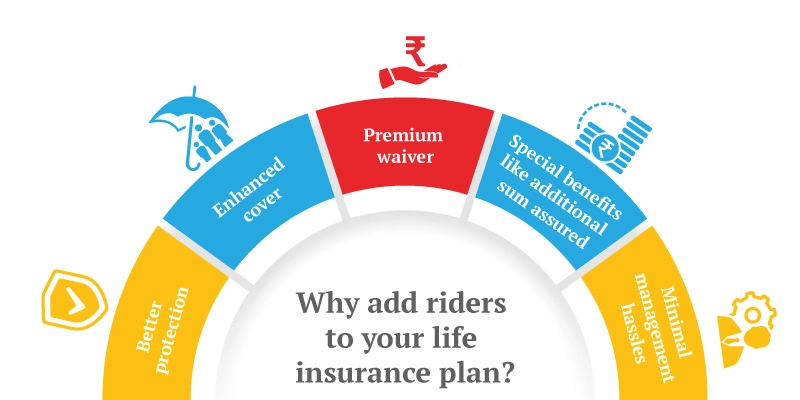

There are numerous ways in which term insurance plans prove to be beneficial. Here are some of the benefits of buying a term insurance plan for the financial security of your loved ones:

Before purchasing a term insurance plan, it’s essential to take a step back and evaluate key factors that will determine how well the policy serves your family’s needs. From assessing your dependents' future requirements to choosing the right insurer and riders, here are four crucial considerations to make an informed decision:

Life is unpredictable and unreliable, but we, at Canara HSBC Life Insurance, strive to be the opposite. We understand your needs and offer term insurance and many other plans that act as saving instruments for you so that you can ensure your family's future and ensure their happiness.

So, don't wait for uncertainty to strike. Act today and invest in a term plan that covers every curveball life may throw your way.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.