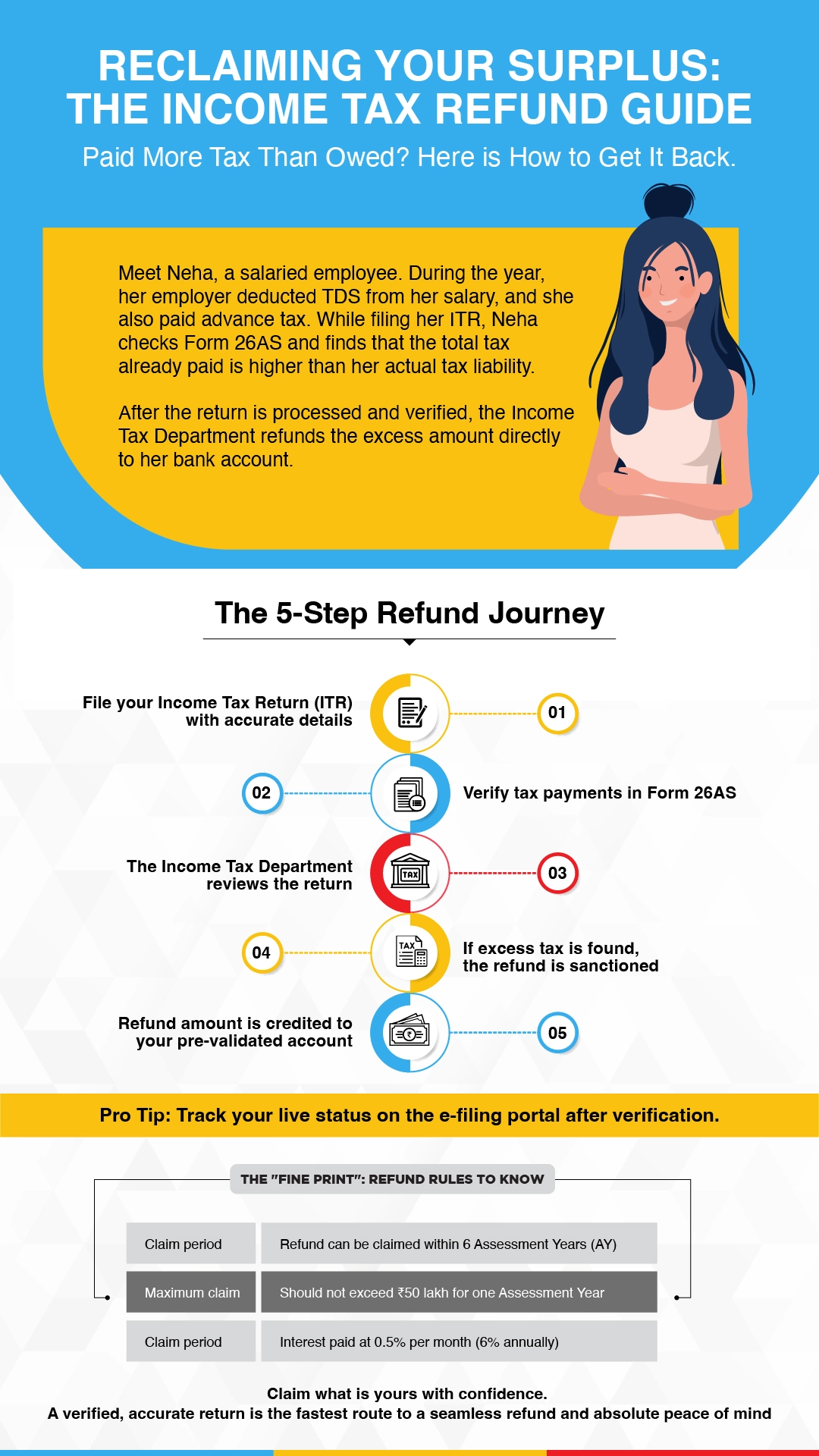

How to Claim an ITR Refund?

The simplest way to claim your income tax refund is by filing an accurate income tax return before the due date. While filing your return, you can check the total advance tax payments under Form 26AS.

After you have filed your income tax return the assessment officer must be satisfied with the income tax calculation on the form. If your balance of advance tax payment under Form 26AS is more than your tax liability under the filed ITR, the officer may approve your tax refund.

You can check the income tax refund status on your e-filing dashboard after filing and verifying the ITR.

Due Date to Claim Income Tax Refund:

You can claim an income tax refund after the end of the relevant assessment year. However, the following conditions will also apply to the tax refund claims:

You can claim a tax refund on the income tax paid within six successive assessment years.

- CBDT will not accept tax refund claims older than this period

- CBT pays simple interest at 0.5% per month (6% per annum) on delayed refunds"

- The officers may accept delayed tax refund claims if they require verification

- The total claim amount for one assessment year should not be more than ₹50 lakh

Income Tax Refund in Special Cases

In case a person is unable to claim an income tax refund due to insolvency, death, liquidation, incapacity, or any other cause, their legal representative, guardian, receiver, or trustee can file for an income tax refund on their behalf, under Section 238 of the Income Tax Act, 1961.

Interest Earned on Income Tax Refund

The Income Tax Department mandatorily pays interest if the refund amount is equal to or above 10% of the total tax paid under Section 244A of the Income Tax Act. Accordingly, simple interest of 0.5% per month is levied on the amount of tax refund and paid to you.