1. Marginal Relief for Individuals:

Marginal relief limits your income tax liability to 40% of the difference between your total income and your tax exemption limit. You cannot receive any further credits on income after marginal relief is provided.

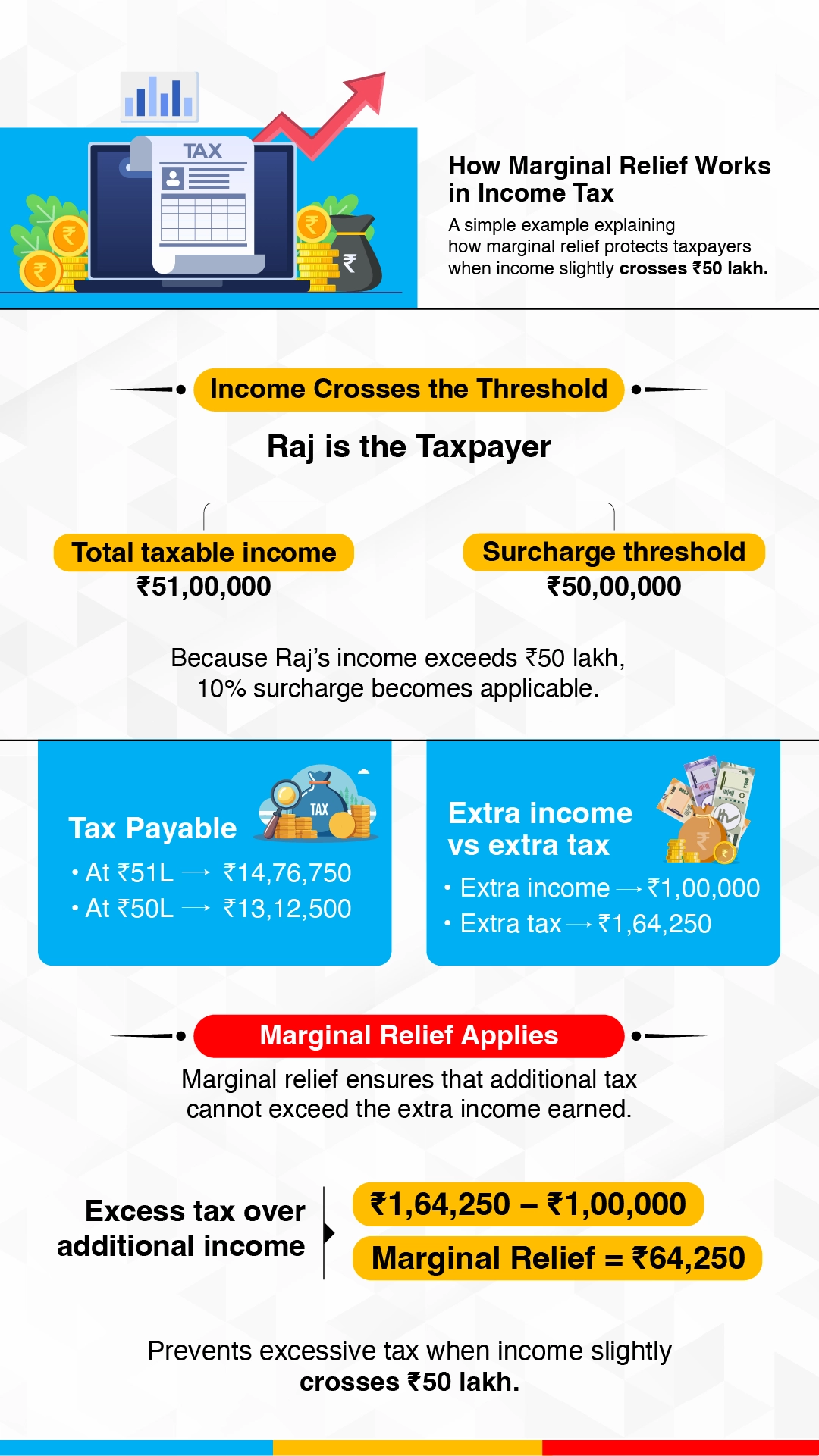

According to Surcharge Provisions made under the Income Tax Act, a marginal relief shall be provided to certain taxpayers. This relief will be equal to the difference between the tax payable (including surcharge) on income above the set limit (₹50 Lakhs or ₹1 Crore) and the amount of income that exceeds the set limit (₹50 Lakhs or ₹1 Crore).

Let’s take an Example:

Say Raj earns a total income (net income after all possible deductions or the taxable income) of ₹51 Lakhs in a financial year, which is more than the 50 Lakhs limit but does not exceed ₹1 Crore. Therefore, Raj will have to pay a surcharge on the income tax computed at the rate of 10%.

Therefore, the total tax payable will be ₹14,76,750. But, if Raj had earned only ₹50 lakhs, then he would have to pay only ₹13,12,500, which means earning an extra ₹1 Lakh gets him to pay extra income tax of ₹1,64,250.

Fortunately, Raj receives marginal relief on the difference between the excess tax payable, ₹1,64,250 (₹ 14,76,750 – ₹13,12,500), and the amount of income exceeding ₹50 Lakhs, ₹1 Lakh (₹51,00,000 – ₹50,00,000). The marginal relief that Raj receives will be ₹64,250 (₹1,64,250 – ₹1,00,000).