Written by : Knowledge Centre Team

2025-08-19

897 Views

7 minutes read

Share

Life can be compartmentalized into different stages with each stage having a broad purpose to attain and move on. All are not fortunate to live through all the stages and those who do live through all the stages may not always experience what that stage is designed for. The exceptions are statistical outliers whereas the vast majority go through all the humdrum of life as designed by the creator.

Childhood is spent in curiosity whereas early adulthood goes in building careers, rearing families, buying life insurance to protect your loved ones and exploring life. The later years are dedicated to consolidating ones’ learnings and earnings besides nurturing the next generation. The final lap or the sunset years are spent closer home, reflecting on life and finally settling into oblivion.

The childhood and growing up years are supported by parents whereas the post-retirement years cause concern because no one can predict the actual life span. The 70-year average means there will be people who will live much beyond that number too.

Fairy tale stories depict retirement as second innings when the old couple becomes free birds again. Travel around the world, do as they please and enjoy every moment of their newfound private space. The kids are independent, the mortgages are paid off and all those items on the wish list now see the light of the day. Far from it. The reality is scary and in contrast to the rosy picture that is generally painted. Lack of financial discipline is putting people at risk of running short of money especially when out of employment during recessionary periods and post-retirement.

Start Early! Whatever you plan to do for a comfortable retirement, start working on it now. 25 is not too early to plan for retirement and 40 is not late either. Some PRO tips to get yourself started on retirement planning:

It is natural to get impulsive to avail credit for buying goods, appliances and holiday packages. Debts taken for buying appreciating assets such as real estate, gold etc is worth it because the returns on investment will be far more than the cost of debt. Depreciating assets burn holes in the pocket.

Spend wisely. Even loans on appreciating assets should taper down with time. Do not carry any baggage post 55/60 years of age.

If you spend Rs 30,000 to manage your living expenses, this amount, when factored with inflation, will become Rs 90,000 in 20-30 years from now. To get such a pay out from your annuities or pension scheme, you will need a corpus of about Rs 3 Crores.

Saving and Wealth Generation are different concepts altogether. Ramesh, aged 40, sets aside Rs 10,000 each month and keeps it in his savings account or fixed deposits that yield 3% to 5% per annum. At an optimistic 5% interest rate, Ramesh will have approximately Rs 40 lakhs in his kitty at the age of 60.

If you factor in the current rate of inflation of 5%, the real growth is actually zero. Building a larger corpus will strain your current lifestyle and health because you will strive to work harder to set aside more money. The trick is to rather make the money work harder than you do. Invest in assets that give inflation-beating returns and create wealth in the long run.

Guarantees are trustworthy when assured by credible, reputed entities that have legacy standing and impeccable track records. Guaranteed Income Plans from Canara HSBC Life Insurance is one such investment cum insurance plan that gives you the safety of insurance while growing your wealth to keep you happy in your older years.

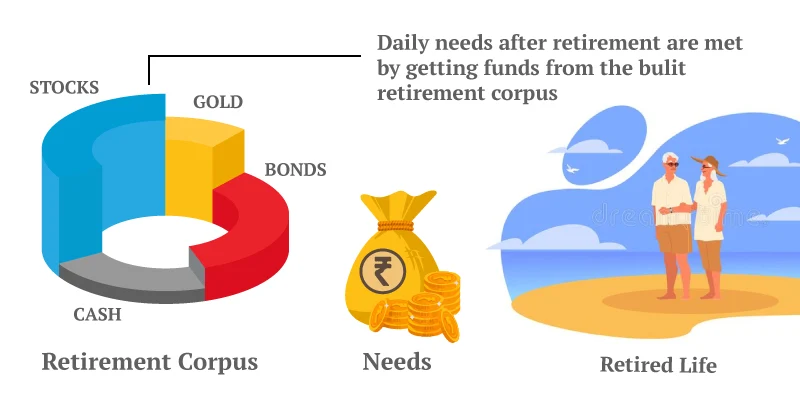

Retirement is an enigma. The uncertainties can be perplexing and create anxiety even in the most level-headed individuals. Thumb rules help you arrive at a figure that you may need by the time you hang up your boots and call it a day. This kitty is what you will have to draw on for the remainder of your life.

Investing in the right assets is important because you will not get a second chance to go back and rectify errors.

The “right assets” are always debatable and diversification helps spread out risks. So, you may invest in gold, real estate, equities and so on. Whatever you do, you must have a cushion to fall back on, should things go wrong.

The tax-free maturity value from the plan ensures that the value of your savings does not deteriorate due to tax. Thus, you can use the entire amount at maturity to build a pension for your retirement. Additionally, the life cover implies that your family will be adequately safeguarded even if anything happens to you before you can build the corpus.

Pension is another form of income. The only difference as compared to your income from employment is that pension comes from your hard-earned income itself, but invested and grown multi-fold by expert pension fund managers. For example, the Pension4Life plan pays pre-defined amounts, called “annuities”, each month after you retire until your death.

There are choices within this insurance policy, offered by Canara HSBC Life Insurance. You can opt for a single-life annuity wherein you get a pay-out till the end of your life OR opt for a plan that returns your invested amount to your nominee on your demise.

These 2 choices listed above can be applied to a joint-life annuity as well in which case your spouse/partner gets the annuity payments after your demise and returns the invested amount to the nominee after your spouse’s death.

Retirement is not as scary as it is made out to be-if planned well and begun early. Investing in wealth-creating assets will build that large corpus which can then be used to generate income streams in your older years.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.