Written by : Knowledge Center Team

2025-12-17

1087 Views

8 minutes read

Share

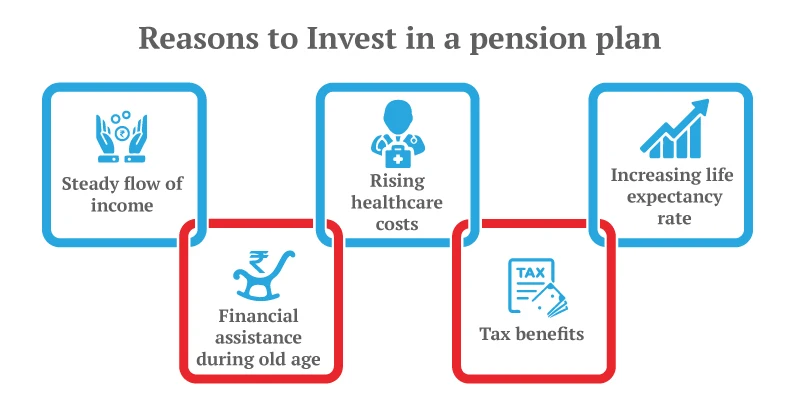

Reaching the age of 50 years is a milestone in numerous ways. Not only is your life open to welcome new adventures and opportunities, but it comes with some financial hurdles as well. One of the most complicated financial difficulties that a person can encounter is planning for post-retirement life. This problem can become pressing when you have entered your 50s and still do not have a retirement plan.

However, you might have heard that it is always better to start late than never start at all. Hence, you must not feel disheartened as planning for retirement in your 50s can also bring you stable returns in the coming 5 or 10 years to lead a well-disposed life after retirement.

It would always be a smart choice to have your retirement plans in place by the time you reach the age of 30 or 35 in your life. However, if you haven’t planned for your retirement already, there is still some hope to resolve this situation. Planning for retirement in your 50’s will have to be distinct from what you would have portrayed planning in your 20’s or 30’s.

The main reason for this is that you a set number of years left to catch up for all your lost time at this stage of your career. Your retirement planning will have to be thoroughly calculated as you must carefully balance the risk and reward. Mentioned below are some of the tips you can follow to save for retirement in your 50s:

However, you must note that when you invest in retirement or a pension plan, your premium amount will be higher than what you would have spent if you opted for a pension plan in your 20s or 30s.

Canara HSBC Life Insurance offers a wide variety of savings plan to help you with your retirement planning. Here are some of the best pension and retirement plans to invest in, even if you are in your 50s.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.