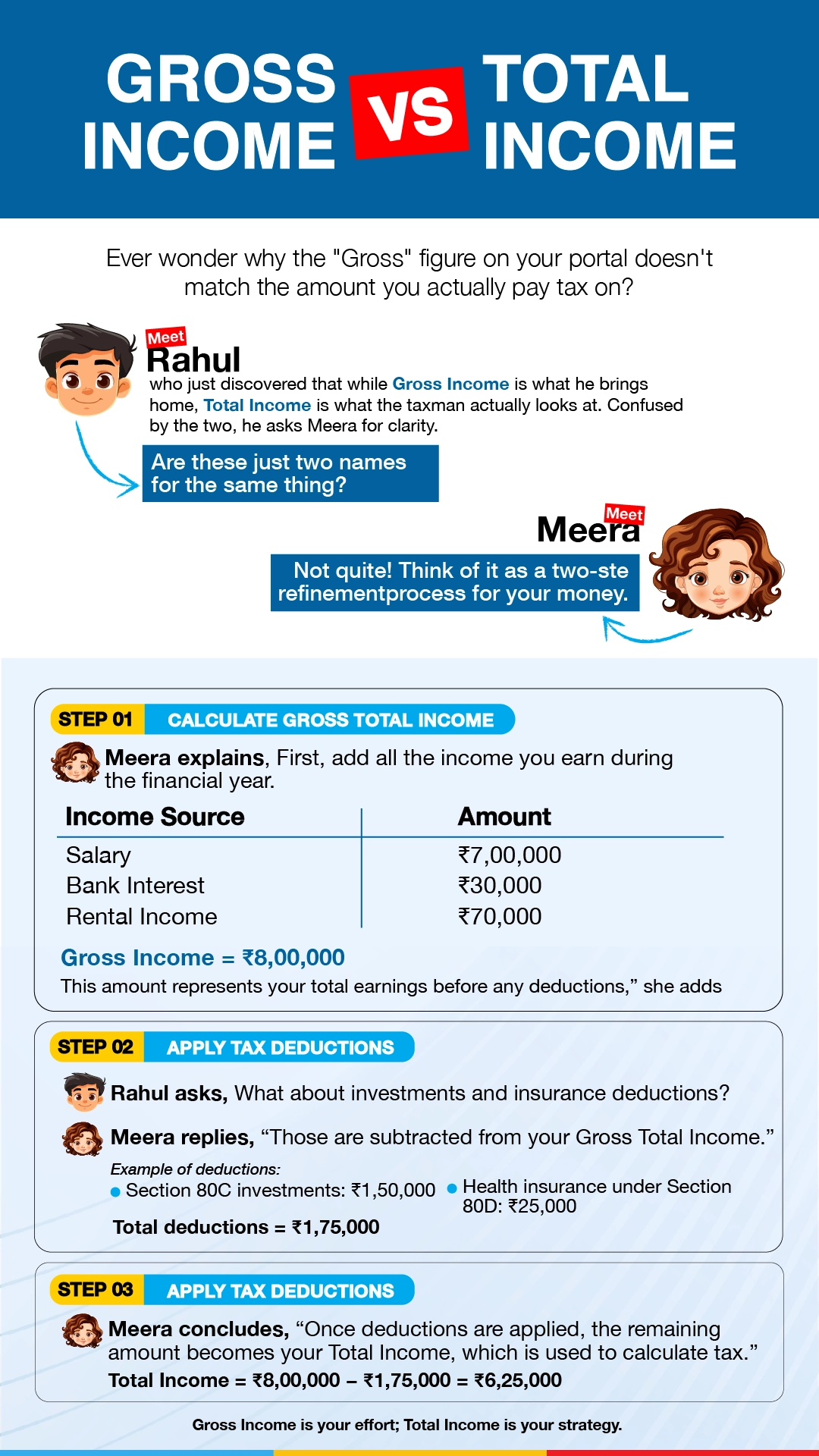

- Gross Total Income (GTI): The aggregate income from all sources before deductions under sections 80C to 80U of the Income Tax Act

- Total Income (TI): The income remaining after subtracting eligible deductions from the Gross Total Income; it's the taxable income

- Income from Salary: Earnings received from an employer, including wages, pensions, bonuses, and allowances

- Income from House Property: Income derived from owning and letting out property, such as rental earnings

- Income from Capital Gains: Profits arising from the transfer of capital assets like stocks, bonds, or real estate

Written by : Knowledge Centre Team

2026-07-24

1723 Views

10 minutes read

Share