Written by : Knowledge Centre Team

2025-12-29

1004 Views

10 minutes read

Share

For many years, people had few options for securing the future of their retirement phase or their families. Today, on the other hand, there are hundreds of options provided by the numerous banks available to the average Indian – so many that the problem is choosing the right kind of plan for you and your family.

The need for life insurance, especially for the primary breadwinner of the family, is obvious. If there is an untimely demise of the person who supports the family financially, other members may have to scramble to survive. To make sure that the family is supported in such an unfortunate incident, at least until another person can secure a well-paying job, many people go for an insurance policy that will guarantee that a specific death benefit will be paid to their choice of nominee after their demise. This assurance goes a long way in helping your family maintain their quality life even after you are gone.

The diversification of the target demographic and the insurance market's growth has resulted in the necessity for new insurance plans. For example, the limited-term insurance plan allows its customers to pay off all their premiums in a short period, preferably at the peak of their career when they can afford to set aside the premium money.

Similarly, banks are beginning to offer a kind of term insurance plan with assured coverage for almost a hundred years.

Why would you not want a term insurance plan that extends to almost a hundred years to rephrase the question? Your family's financial burdens will be cushioned for a more extended period. After achieving economic equilibrium, they may even think about investing the monthly allowance they get from the insurance company for maximized returns.

Even your family has to deal with additional costs. In the case of educating your children abroad, inflation leading to higher household expenses, the need to invest in expensive appliances or hardware, or the marriage of a family member, a hundred years of coverage will ensure that there is a stable influx of income no matter what, for as long as it lasts.

A whole life term insurance plan guarantees your nominees' financial protection and, by extension, your entire family. Unlike an ordinary term insurance plan, these plans will extend up to 99 years (which effectively is a century). This is the longest possible term you can acquire as a shield for your beneficiary parties.

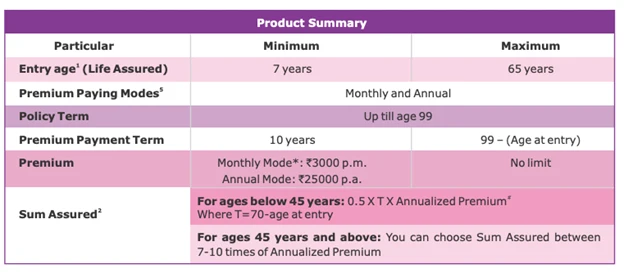

The 99-year term insurance plan will be applicable until you reach the age of ninety-nine. Effectively, if you take up this plan when you reach fifty, your policy will give you forty-nine years of protection. This can easily cover expenses until your kids reach the age where they can support themselves.

People worldwide realize that no savings will suffice, even after they reach their age of retirement. Ordinary retirement plans and insurance premiums are merely becoming insufficient with the rising expenses of living and the accelerating inflation rates plaguing the global economy. This is why people want financial protection that covers them and their families for years ahead.

With the current pandemic scenario that takes no prisoners, early death is more likely than ever, even for healthy and at his or her prime. People also realize that the assets that they may invest in today – stocks, real estate, property, etc. – may not be sufficient to support their children in the future since the world is changing culturally and economically at a faster rate than ever.

Going for a whole life term insurance will minimize all of these hurdles for your children. Past the retirement age of sixty to seventy-five, your family will be provided with a monthly installment that will cover your needs according to the estimates.

Like any other term insurance plan, the hundred years plan extends to a particular time, in this case, until you reach 99 years of age (even if you die before that age). The policyholder will pay an insurance premium every month – this is usually an affordable amount that the policyholder can choose, based on their current economic standing.

This compounded amount will be paid to the nominee towards the end of the plan. If and when you pass away before the culmination of the plan (which is highly likely since the overall life expectancy in India’s now 68, despite a significant increase in the past decade (source)), the beneficiary would be provided with a guaranteed amount of money.

There are several benefits to the 99 years plan:

The affordability factor also comes into play when you look at the highly flexible options for the frequency of payment of the premium. This can be monthly, quarterly, or annual, depending on the stability of your pay. If you work in a field like business or in the entertainment industry where their income is sporadic and come in spurts of large amounts, the yearly plan will be beneficial for you. Transferring a large chunk of your income once a year will ensure that your family is well off after you are gone. The 99-year plan, therefore, suits almost every profession out there due to its high customizability.

In conclusion, whole term life insurances have their advantages. Still, you should ensure that you take proper care of yourself and disclose your habits and health details to the insurance company beforehand.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.