Written by : Knowledge Centre Team

2025-09-07

1266 Views

11 minutes read

Share

Critical illness riders offer coverage against life-threatening diseases such as heart disease, stroke, cancer, diabetes, kidney failure etc. Critical Illness rider offers financial protection to the life assured’s family with the treatment expenses of the critical illness.

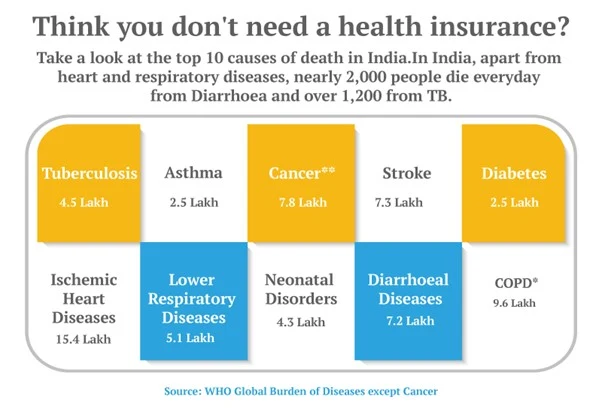

Life insurance plans can provide you with financial support during emergencies, including critical illnesses. You can have specific insurance plans to take care of treatment costs associated with critical illnesses like heart ailments and cancer in India. You can also add critical illness cover to your term insurance plan.

A Mediclaim insurance plan can cover a large part of the hospitalisation and surgery expenses. However, most critical illnesses require only temporary hospitalisation, yet the treatment can be costly. Thus, you need an alternative health plan, i.e., critical illness insurance.

If you are diagnosed with a covered illness or the critical illness plan will give you a large lump sum amount to look after your financial needs. Term insurance plan such as iSelect Smart360 Term Plan provide critical illness cover against 40 listed life-threatening diseases along with a terminal illness benefit.

Term insurance is one of the basic investments for your family’s long-term safety. Term insurance with critical illness cover means, you have an additional benefit with the large life cover. The critical illness rider will offer the following:

Insurance riders are additional coverage that you add to your term insurance or health insurance policies. The advantages of adding critical illness and other riders to your term insurance plan are:

Critical illnesses rider will include diseases like heart attack, cancer, stroke, kidney failure, etc. Critical illness rider of iSelect Smart360 Term Plan covers several disability conditions as well.

The dependants may use the benefit amount to save for their future and meet their regular financial needs. Similarly, iSelect Smart360 Term Plan have a default terminal illness benefit. This benefit pays the sum assured if the insured is terminally ill and has no chance of survival.

However, critical illness benefit is available to you as the insured. Even though the benefit does flow to your family as well in the way of a regular income, primarily the money should cover your medical and treatment bills.

You can also have specific critical illness covers, such as for covering cancer. Such critical illness riders will cover even the early stages of the disease increases your chances of survival and quick recovery.

The insurance market offers different types of insurance plans, including critical illness riders. Hence you should know how to choose the best critical illness rider plan for yourself. Below are some features to look for in a critical illness rider plan:

The first thing you need to check is the number of critical diseases and conditions covered under the plan. For example, the Health First critical illness plan from Canara HSBC Life Insurance covers about 40 illnesses and health conditions.

An essential aspect of any coverage is to select the right amount. It is especially important when you are buying term insurance with a critical illness rider. Ideally, critical illness cover should range from 30% to 50% of your term life cover.

All health insurance policies have a clause for a waiting period before they start covering specific diseases. Critical illness policies have a waiting period of up to 180 days for covering a new diagnosis. Any illness diagnosed within 48 months of the policy start date falls into pre-existing disease bucket and by default, the policy will not cover it.

Different insurance companies have a different age limits up to which you can continue critical illness insurance. Hence, do check the maximum age for coverage even while buying term insurance with critical illness cover.

An online claim process will make your life much easier at the time of a claim. With the critical illness plans of Canara HSBC life insurance, you can maintain your policy using an Electronic Insurance Account (EIA). Use the account to file your claim. You can also assign the task to someone else.

A critical illness rider is a great addon to your term insurance cover. Term insurance plans do not carry critical illness cover by default. So, you will need to check whether your life insurance provider offers a critical illness rider. If yes, you can add it to the term insurance plan.

iSelect Smart360 Term Plan from Canara HSBC Life Insurance offers critical illness cover as a rider.

Addon covers allow you to enhance your term cover and prepare better for various emergencies. Apart from the critical illness cover, you should consider the following added covers as well:

Having a basic term policy with a critical insurance plan is a necessary addition to your contingency preparations. It will provide you with extra protection and help handle any medical emergency if you have a proper financial planning. However, as your financial liabilities increase and you have more dependents, it is always better to have additional covers.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.