Written by : Knowledge Centre Team

2025-12-19

1009 Views

7 minutes read

Share

Recently, we have seen much upheaval in the world at the behest of the pandemic, and other unexpected developments. Some of them have been global while others are limited to specific areas and communities in the world.

The pandemic had many risk management companies and organisations scrambling for ideas. Insurers accelerated technological adaption to stay relevant in the new reality. Also, health and death claims rose all across the world, resulting in a premium rise within the year. Life Insurance plan is an amazing concept of risk management. It is a community product, and the larger the area of adaption, the better it works. The cost of the insurance is determined in multiple stages, and you can further make different classes of the risk groups.

For example, consider a small town of 100 families. Flood destroys houses of two families on an average every year. The destruction is random and any two houses may receive the damage.

The town can save its population from gradually going bankrupt by offering insurance to every family. If the repair cost for one house is Rs. 10,000, the 100 families can collect Rs. 20,000 and create a pool to assist the families in distress.

In this case, if in any year less than two houses are damaged the premiums (contribution of each family) for the next year could be lower. And if more than two houses are destroyed in a year the premiums will have to increase.

Now, this is a small town, if you extrapolate such towns across a larger area, you can imagine different towns with different populations. All these different towns will have a different number of houses being damaged due to a number of natural causes.

If the same insurance pool has to cover the risk of more than one town, a small part of the premium cost of all the towns will have to be shared. Thus, if out of the several towns covered by the insurer if one experiences higher claims, it will affect the cost for other towns as well.

Life insurance premium, as well, works on similar principles. However, the small difference is, the insurers worldwide are connected through re-insurers. Re-insurers are global companies which insure the risk of primary insurers.

Thus, there could be two reasons for a possible premium increase of a term insurance plan:

Any change in these two factors will affect the prices in general and for the whole group.

The short answer is ‘no,’ the increase will only affect the new term insurance policies. So, if you are paying a premium for an existing policy it will remain the same. However, when you buy a new term plan, the new premiums would be as per the new rates.

However, if you are trying to apply for sum assured increment on your existing policy, you may enjoy the discounts, being an existing customer. Few insurers like Canara HSBC Life Insurance offer life-stage increment option on their term insurance plan iSelect Smart360 Term Plan.

You can request for an increment in the life cover amount of the plan after marriage, childbirth or home purchase using a home loan.

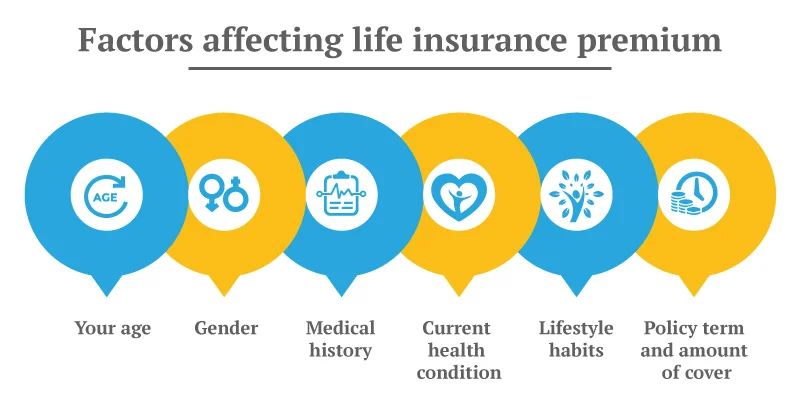

Since the increase affects the new subscribers, you should know what will affect your individual life cover premium.

Although a blanket increase in mortality premium will affect the price you pay for the life cover, you still need to consider the following factors:

If you want your life insurance premiums to be lower, you need to buy the cover at an early age. While health is in your control to some extent, lifestyle habits like smoking and drinking are completely in your control.

In the case of an existing health condition, the insurer may charge an extra premium. However, if you are the primary breadwinner of your family, term insurance is all the more important for you.

So, the only way to have a lower premium for your life cover is to buy it at a young age and maintain a healthy lifestyle.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.