Written by : Knowledge Centre Team

2025-12-07

1808 Views

10 minutes read

Share

Term insurance vs accidental insurance is a classical confusion for people considering insurance protection for the first time. It is true that you work hard to live a comfortable life and secure your future. You dream of buying a new house, going on a foreign vacation, and sending your child to the best college - the list is endless.

Both term insurance and accidental insurance help you offer a financial safety umbrella to your family. You may be doing your best to achieve your goals. However, if an unfortunate event happens, these plans will continue to bear your responsibilities.

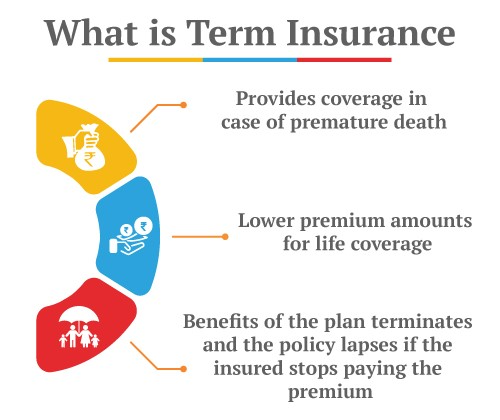

Before we can compare term insurance and accidental insurance plans, we should know the standard definitions of the plans. This will clarify the fundamental differences between the two types of insurance plans, and help you appreciate the other differences as well.

Term Life Insurance is an insurance product that offers financial coverage to you for a specific time period (policy tenure). These are the purest form of life insurance that gives you high coverage at an affordable price.

Assume you buy a term insurance plan at age 30 with a cover of Rs 75 lakh, and the policy tenure is 20 years. In case of the unfortunate event of your death during the next 20 years (policy tenure), the death benefit (Rs 75 lakh) is paid to your nominee by the insurance company. If you survive the policy tenure, you do not receive any benefits.

Also Read - What is Term Insurance?

Personal Accident insurance is a policy that reimburses your medical costs and provides you compensation in case of disability by accident. Also, it pays you a lump sum amount in case of death caused by an accident. Depending on the policy type, you can have additional benefits like coverage in case of income loss for a certain period.

You can have financial stability after an accident that can result in partial or permanent disability by investing in personal accident insurance.

| Term Insurance | Accidental Insurance | |

|---|---|---|

| Tenure | A term insurance plan has a policy tenure of 10,20 or more years, and there is no concept of renewal. | Accidental insurance has a policy tenure of one year, and you have to renew your policy every year. |

| Major Risk Factor | Term insurance covers you against death arising from natural causes. If the policyholder dies due to an accident, the benefit is not provided. The nominee receives the benefit amount in case of the insured person's demise | Coverage is specifically for deaths caused by accidents. The benefit amount is paid if the insured person dies due to an accident. In case the insured suffers injury in an accident, the cost of medical treatment can be claimed depending on the policy |

| Coverage Amount | The maximum coverage amount can be up to 20 times your annual income | Maximum 10 times your annual income |

| Benefit Distribution Mode | The sum assured in term insurance can be claimed as a lump sum, monthly income, or a combination of both | The sum assured is received only as a lump sum amount under personal accident insurance |

| Cover for Disability | You can add disability and accidental covers as riders | Disability and accidental death are primary covers of the policy |

Your untimely demise affects the future prospects of your family. However, an accidental disability can also cause financial hardships and unexpected expenses. So, the answer is not term insurance vs accidental insurance, but term insurance and accidental insurance.

You should invest in both term insurance and accidental as both have different advantages. The term insurance policy covers the financial needs of your family in the case of your death. Whereas, accidental insurance can also cover your financial needs due to accidental disabilities.

Learn if a term insurance plan cover accidental death.

Having both the policies would mean that you can continue your life cover after the disability. Thus, protecting your family financially even after the accidental claim. If you have only accidental insurance, the policy may cease to exist after a disability claim or have reduced benefits.

Additionally, accidental insurance will not cover death due to other causes.

You can buy personal accident insurance in one of the following two options:

It is better to avail of the personal accident and disability cover as a rider with term insurance. iSelect Smart360 Term Plan from Canara HSBC Life Insurance, offer premium waivers as well. The premium waiver option kicks in if you have to make a disability claim on the Accidental Rider benefit.

If the claim is payable the future premiums of your life cover will be waived off, but the cover continues until the expiry.

Your insurance cover should not only be large enough to cover all the financial needs of your family but also cover several risks. Both term and accidental insurance plans are essential as they cover different conditions and widen the scope of your insurance.

Ideally, your term insurance cover should be 10-15 times your annual income. Your accidental cover can be about 25-50% of your term cover.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.