Browse Article by Category

Money back policy is a life insurance product that provides life coverage during the policy term and survival benefits after the end of policy tenure. A money back policy is the right insurance plan for you if you want to protect the future of your loved ones. It can be your one-stop plan to fulfil multiple cash flow needs with a single investment.

A money back plan is a long-term safe investment plan that keep your investment safe from inflation and taxes and ensure your family will complete their goals even after your untimely demise.

Table Of Content:

Secure Your Child’s Education and Future Milestones

Enter OTP

An OTP has been sent to your mobile number

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Sorry! No records Found

Request Registered

Thank You for submitting the response, will get back with you.

Complaint Registered

. Please use this ID for all future communications regarding this concern.Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

What is a Money Back Policy?

Money back policy is a type of life insurance product that offers regular returns or a lump-sum amount to the insured at a pre-defined time during the policy term. With a money back policy, you can receive guaranteed returns, or the returns may depend on investment performance, or a combination of both. You should buy the right money back policy that meets your specific financial goals. A money back plan also offers a life insurance cover to secure financial wellbeing of your loved ones if an unfortunate event occurs.

Money Back Insurance Policy – Overview

When you invest in a money back insurance policy, you will receive money during the policy tenure as a percentage of the sum assured. The payout you receive is called "Survival Benefits." You will continue to receive regular payments throughout the tenure of the policy. The remaining sum assured is paid on maturity along with vested bonuses if any. In the event of the demise of the insured, the beneficiary receives the sum assured along with a bonus amount. The amount is given even if the insured has received payment during the policy tenure. This is one of the unique features of a money back plan.

Most traditional life insurance plans do not allow you to withdraw funds before the tenure. You always have the option of taking a loan, but the amount may be limited, and you have to start thinking about the repayment as soon as you avail of the loan.

To be prepared for unexpected events in life, you should have a plan that pays you lump sum amounts during your tenure. A money back plan is an excellent option that solves your liquidity problem.

How Does a Money Back Policy Work?

A money-back policy offers you survival benefits, investment opportunities, and maturity benefits. Let us see how the money back plan works.

Using a money-back policy, you can plan for your financial goals like your child's education and your retirement.

Suppose you want to buy a child money-back plan. Assume the current age of your child is 10 years old. You buy a money back plan for a sum assured of Rs 20 lakhs in 2021. The tenure of your policy is 25 years, and you pay a premium throughout the policy tenure. As per the policy term, you will receive survival benefits of 20% of the sum assured (Rs 4 lakhs) every five years.

On maturity, you will receive your last 20% along with the bonus, if any. You can use the pay outs as follows:

- 2026: In the fifth year, you receive Rs. 4 lakhs. You can use these funds for your child's tuition fee.

- 2031: The next payment of Rs 4 lakhs will be made in the policy's tenth year. Your child will be 20 years old by this time. The money received can be used for the higher education of your child.

- 2036: When your child turns 25, you will receive the third payment in the 15th policy year. You can use the amount for their marriage expenses.

- 2041: The fourth payment you can keep for retirement purposes. It will come in the 20th policy year.

- 2046: You will receive the remaining Rs. 4 lakhs from the policy, plus any applicable bonuses, and the policy will be terminated.

- If you die during the policy term, your nominees will receive the sum assured of Rs. 20 lakhs plus any accrued bonuses, and the policy will be terminated.

By 2041, you would have received Rs 16 lakhs. In 2046 (maturity), you will receive the remaining Rs 4 lakhs along with the bonuses. The policy will terminate once you have received the final payment.

In the case of an unfortunate event, if you die in the 18th year of the policy, the beneficiary will receive Rs 20 lakhs (sum assured) along with bonuses. The nominee receives the complete sum assured, even though you have received Rs 12 lakhs by then.

Example of a Money Back Plan

Let us understand how a money-back plan works with the example of Sachin.

Sachin has started investing in the Money Back Advantage Plan, a money back policy from Canara HSBC Life Insurance.

Sachin is married and has a 10-years-old son as well. He purchased the policy for a period of 16 years. To continue his money back policy, he has to pay regular premiums for 10 years (premium payment term).

Survival and Maturity Benefits

Through this money-back insurance policy, he will receive 20% of the sum assured as payouts in the 5th, 9th, and 13th years of the policy.

These amounts are known as "survival benefits". If Sachin survives the term of the insurance policy, then the remaining amount will be given in the 16th and final year of the policy. This is also known as the ‘maturity benefit’.

Here are the stages of the policy:

- 1st payout: This is in the 5th year of the policy. With the money received, Sachin and his family planned a trip to Europe, something they had always wanted.

- 2nd payout: The second payout is made in the 9th year of the money-back policy, Sachin’s son has now turned 18 and has finished his schooling. He wants to have a career in the field of science and, thus, decides to pursue B.Tech. This payout is used to pay his college fees.

- 3rd payout: Sachin received the 3rd payment at the end of the 13th year of the policy. He used this payout for his son’s marriage.

- 4th payout: This is the final payout. This is the maturity benefit and also includes the bonuses the policy has accrued. He thinks now that his son is settled. He decides to use this maturity amount to save for his retirement and purchase a small house for himself and his wife.

What Happens at the Time of Death?

If Sachin dies during the term of the policy, then his family will receive the sum assured along with the accrued bonuses.

Why Do you Need a Money Back Policy?

You will need a money-back policy in the following scenarios:

- You want to preserve your Savings: This is a very common use of money-back policies, as it allows your savings to stay safe and become useful later. Also, these savings will not only come back to you within a few years, but you will also have a growing retirement corpus available at maturity.

- You want to Simplify your Investments: Investment decisions can be very challenging, especially when your focus is on earning money rather than investing. But you do not want to lose your savings while you decide. So, invest in a money back policy to preserve the capital from inflation, lock-in, and taxes.

- Save for an Important Family Goal: Money back policies can not only preserve your invested capital, but also the goal itself. The sum assured will be available to the family when you cannot be there for them.

- Support a Dependent Family Member: Often, parents spend their entire life’s earnings and fortune to help you stand on your feet. Even at times, you may have a family member who needs lifelong financial support due to illness or disability. Money-back policies are perfect long-term cash flow solutions in these scenarios.

Key Features of a Money Back Policy

The best money back plan helps you achieve both your medium and long-term goals. It also gives you a life cover. Here are some features of the best money-back policy:

- Guaranteed Returns: A money back policy is an ideal investment if you want safe and secure returns. The returns are not driven by the fluctuation of the equity market. You receive guaranteed returns irrespective of how the market is behaving.

- Income During the Policy Tenure: You receive regular income to take care of your large expenses. For example, you can use the money to pay off your existing loans, go on vacation, or redesign your house.

- Income on Maturity: You get a guaranteed and secured income on maturity, which helps you plan your future in a much better way.

- Financial Support upon Death of the Insured: If the policyholder passes away, the nominee receives the sum assured along with the bonus (if any). The policy acts as a standard insurance plan in this respect.

- Bonus Additions: There are two types of bonus amounts in a money-back policy: a reversionary bonus and an additional bonus.

- The reversionary bonus is given as a percent of the sum assured by the company. The amount gets added to the overall payment you are supposed to receive at maturity or in the event of an unfortunate event.

- Sometimes, the company may also give you an additional bonus depending on the company's performance. The other instance when you receive additional bonuses is when you pay the entire premium on time.

- Add-on Riders: The option to add different riders to your money back plan depends on the policy you are choosing. You may also get the option to add a hospitalisation rider to your money back policy that will help you manage the hospital expenses if the policyholder or life insured has been hospitalized.

A premium waiver is another rider that you may include if it is available in your money back plan. If the policyholder fails to make the premium payment, this rider protects the loss of the life insurance plan. The policies continue to protect the lives of those who are insured rather than expiring due to nonpayment of premiums.

Benefits of Money Back Plans

Money back policy is one of the best variants of life insurance. A money-back plan gives you guaranteed regular payouts at defined intervals. These payouts start within the policy and help you meet various needs and achieve your investment goals. Here are the advantages of this plan.

- Guaranteed Returns on Investment: One of the biggest benefits you can get from your money back plan is that you will get guaranteed returns. Thus, as the name suggests, it makes sure that you get your money back from the policy. This advantage makes the money-back policy a tension-free investment. You will not have to stress as to how your investment will do and whether you will be able to get money or not. This is an ideal plan if you do not like to take risks and the safety of the corpus is your top-most priority.

- Provides you with a Life Cover: Since a money-back plan gives you a payout at regular intervals, and that it comes with an insurance cover as well. So if anything unexpected happens and you lose your life, then your family will be given a lump-sum amount, i.e., the sum assured. The sum assured that your family will receive will help keep them financially secure so that they do not have to struggle. Through this money, they can carry on with their expenses and can achieve their goals even if you are not there to provide for them.

- Returns are Generated After a Few Years: In other variants of life insurance, there is only a death benefit involved. That is, your family will receive the sum assured if you die during the policy. While in other policies, you may have to wait a long time to receive a benefit. But with a money-back insurance policy, you receive the returns while your policy is still running. You start receiving payouts just a few years after investing in the policy. In the Canara HSBC Life Insurance, Money Back Advantage Plan, for example, the payout begins at the end of the fifth year.

- Helps Increase your Sum through Bonuses: Bonuses are an integral part of a money-back plan. You can get an additional amount in terms of bonuses, such as "reversionary bonus" and "terminal bonus". These bonuses are available if you have paid all your premiums. A simple reversionary bonus is added to your policy at the end of the year. This gets accrued every year. This accrued amount is given to you at the time of maturity or at the time of your death, to your family. There is another bonus known as a "terminal bonus" in the money-back plan. These are based on the profits earned by the insurance company.

- Tax Benefits: As with other life insurance plans, a money-back plan is also eligible for tax deductions. These tax deductions are available under section 80C of the Income Tax Act 1961. These tax-benefits help you reduce your tax liability. That is, you can lower your annual tax outflow if you invest in a money-back policy and save even more money.

Under Section 80C, you can avail a deduction of up to Rs 1.5 lakh towards the premium you pay for your money back plan. Also, the maturity benefit will be exempt from tax if your annual investments in the plan never exceed 10% of the policy life cover. - Secure Investments with a Money Back Plan: Money back plans have premium protection features. The premium protection feature allows you to ensure investment for the full policy term even after your demise within the policy term. After your demise the family receives the life cover sum assured immediately and the intended maturity value upon usual maturity.

- Value of Money Higher with a Money Back Policy: The value of money declines over time due to inflation. This means that Rs 1 lakh now is more valuable than Rs 1 lakh five years from now. The money back policy pays part of the sum assured before maturity. Therefore, you receive a major part of the total survival benefit much before maturity. The value of these early receipts in your hand is higher than if the amount was paid all at once at maturity.

- Insured Receives the Full Sum Assured on Maturity: Upon maturity, the money back policy will pay the remaining sum assured and accrued bonuses. Thus, the policy pays the entire sum assured to the insured upon surviving the policy term. Parts of the sum assured would have been paid at regular intervals before maturity.

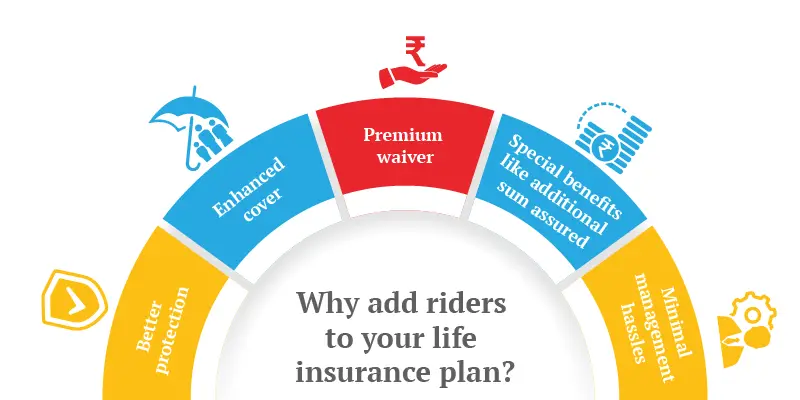

Riders Available in a Money Back Policy

A money-back policy provides you with an option to add coverage that is not included in the original policy document in the form of riders. Riders give you cover in cases like accidental death, hospitalisation expenses, terminal illness, permanent disability, and many more.

The availability of the rider varies from insurer to insurer and also depends on your policy tenure. In general, you can purchase the below riders along with the best money back policy.

- Waiver of Premium: This rider provides you with a waiver from paying the premium amount under certain circumstances. Even though you don't pay a premium, you will be eligible for life insurance.

- Accidental Death Rider: In this rider, if the policyholder suffers an accidental death, the beneficiary will receive a lump sum amount.

- Terminal Illness Rider: If you contract a terminal illness (as defined by the rider), the rider will provide you with guaranteed cash. So, in a way, it acts as a guaranteed money back plan. You can use the money to pay off your medical bills or for any other reason. Some of the major terminal illnesses covered are:

- Heart attacks and bypass surgery

- Paralysis or strokes

- Different types of cancer

- Renal or kidney failure

How to Choose the Best Money Back Policy?

You can invest in multiple types of money back policies nowadays. Select the money back policy as per your cash flow needs and financial goals. Check for the following while buying a money back plan to select the best possible plan:

- Define your purpose and financial goal. For example, if you are purchasing the money back plan to fund your child’s higher education goal.

- Select a tenure such that your financial goal’s demands and plan’s cashflows coincide

- Select the amount you need with the cashflows and maturity. This will help you define your investment amount.

- Adjust the investment as per your present capacity

Select the premium protection feature to safeguard the maturity value if necessary. For instance, you want to provide for the child’s education or marriage goal even when you are not there. However, if you are saving to fund your retirement needs life cover payout for your family will be enough.

Additionally, you can select participating and non-participating options to invest in for additional growth.

Child Money Back Plans

Child money back plans are money back plans more suited to fulfilling a child’s higher education and marriage goals. A child will need a regular cash infusion every few years during their higher education years. A money back policy with its regular cash flow can support this financial need of the child without your intervention. At the same time, you can guarantee the financial support even if anything happens to you on the way.

Comparison Between Fixed Deposit (FD) and Money Back Policy

Fixed Deposits and Money Back Plans are two of the most popular investments that involve lower risk and guaranteed returns. But these plans have several differences as well. Let's take a look at the differences between these two investments.

| BASIS | FIXED DEPOSIT | MONEY-BACK PLAN |

|---|---|---|

| Type of Investment | It is a fixed investment/savings scheme wherein you put lump-sum money and earn returns | This is a type of life insurance plan that provides life coverage and regular payout |

| Returns | Fixed-rate | Guaranteed Returns |

| Term | Flexibility in choosing the term. FD’s range from 7 days to as long as 10 years | Generally taken for a long-term period can range from 10-30 years |

| Investment Required | The investment is generally low and depends on where you are opening your account. Minimum investment ranges from Rs 1000-5000. There is no maximum limit | The premiums are to be paid regularly and the amount depends on various factors such as age, sum assured, riders, etc. Visit the online premium calculator to get an estimate |

| Mode of Payout | FD gives you a pay-out in a lump sum after maturity | You will get payouts at regular intervals defined by the policy. Maturity benefit at the end can be in lumpsum. |

| Withdrawal | You can withdraw your amount but it will cause a reduction in the interest rates | Withdrawals can be allowed in a money-back plan depending on the type of policy |

| Tax-Benefits | Not eligible for tax benefits | Eligible for tax benefits u/s 80C and 10(10)D of the Income Tax Act |

Eligibility Criteria to Buy a Money Back Policy

To buy a money-back policy, you need to satisfy any (2) of the below-mentioned eligibility criteria:

- The minimum age at the time of buying the policy should be 8 years or above.

- The maximum age to start a new policy is 55 years. If you are paying premiums in monthly mode, the maximum entry age would be 45 years.

- The maximum age for the policy to mature is 71 years.

- You should be financially sound to pay the premiums for the policy.

Documents Required to Buy Money Back Policy

If you are planning to buy a money-back plan, you will have to provide the following documents to the insurance company:

- Documentation proving your age

- Your address proof document

- Proof of your income

- Application form duly completed

- Medical reports, if required

Why Buy Money Back Plan from Canara HSBC Life Insurance?

Canara HSBC Life Insurance is offering you a wide range of life insurance plans. You should buy money back policy from Canara HSBC Life Insurance for the following reasons:

Are money-back policies a good investment for you?

If you want the safety of capital, money-back policies are a perfect investment option for you. Money-back policies are safe, long-term investment plans that invest money in government bonds and top-rated corporate debt.

Due to the regular cashback feature, money-back policies are also more liquid than other long-term insurance policies. You can use the money back plans to create a secure stream of tax-free income for your family. Thus, money-back policies are a perfect wealth transfer instrument as well.

For example, you can start five money back advantage plans over the next five years and invest in such a way that the money-back arrives every year from a different policy.

Related Articles on Money Back Plan

FAQs on Money Back Policy

A Money back insurance policy is a life insurance investment plan which offers guaranteed returns, life cover and tax-saving benefits. Money back plans also offer automatic cash back at regular intervals. The cashback is a defined percentage of the guaranteed sum assured. For example, 4 cash backs of 15% of the guaranteed sum assured, which is 60% of the total sum assured. The remaining 40% will be payable at policy maturity.

A money-back policy is the only investment plan offering survival benefits, maturity benefits and life insurance cover. The plan can ensure that your family can meet their goal even after your early demise. The money you invest in the plan qualifies for deduction under section 80C of the income tax act. Also, the cashback you receive from the policy is tax-free under section 10(10D).

The amount you pay as a premium helps you reduce your tax liability under section 80C. Thus, you can claim a deduction for up to Rs. 1.5 lakhs of invested premium every financial year. The money backs and maturity value received from the policy is also tax-free if the annual premium of the policy had been less than 10% of the life cover amount.

The money-back policy that suits your budget and risk preference and aligns perfectly with yours as well as your family’s needs and goals is the best money back policy. Take into consideration all your current and future needs before purchasing the best plan.

Paying premiums regularly is essential to keep any life insurance policy running. The frequency with which you will pay your premiums depends on the insurance company you are buying them from.

For example, in Canara HSBC Life Insurance, Money Back Advantage Plan, the premium payment term is 10 years and you can choose to pay monthly or annually.

The policy allows a grace period of 30 days in the case of annual premium payments and 15 days for other modes. If you failed to pay the premium on the due date you can deposit it within the grace period without losing your benefits. However, after the grace period, you may have to pay a penalty as an additional premium and lose some of the bonus additions. If the policy has acquired paid-up value, you may have to revive the policy.

However, if you have opted for the premium waiver option and you are unable to pay the premium due to the covered event, like accidental disability, etc. your policy will continue. You will not need to pay further premiums. But do file the claim for the incident with the insurer to activate the premium waiver benefit.

No, you are not allowed to transfer your money back policy. However, there is an option to make an assignment in another person's name. Or you can buy a new money back policy for the other person.

The amount you receive from your policy is taxable only if the invested premium in a policy year is more than 10% of the base life cover sum assured of the policy.

If you want to surrender your money back policy, you will have to visit the branch office of the insurance company. Or you cannot do it online.

The policy can be revived only within three years of expiry. Upon expiry, the policy acquires paid-up value and can be revived only within the permissible period. The policy can be revived only a limited number of times in the policy period. The maturity age cannot be increased from the original plan’s maturity date. Revival premium will include the difference between the old and new premium and interest on the overdue premiums.

All investment instruments have a certain amount of risk. Money back policy is less risky compared to other investment products.

Popular Searches

- Senior Citizen Saving Scheme

- Post Office Savings Scheme

- What is Sum Assured?

- Money Saving Tips

- Saving Plans for Child

- Endowment Policy

- iSelect Guaranteed Future Plus Plan

- National Savings Certificate

- Tax Saving Plans

- Senior Citizen Savings Scheme Calculator

- NPS and PPF

- Savings & Investment Plans

- Saving Schemes

- Save Money For Salaried Professionals

- One time Investment Plan for Child

- Investment Options for an NRI

- All About PPF

- Sum Assured

- Policy Surrender Value

- Guaranteed Savings Plan