Written by : Knowledge Centre Team

2026-02-10

1303 Views

8 minutes read

Share

The middle-class Indians are the ones who suffer the most from inflation and economic disruption. The thought of having nothing set aside for our future sends shivers up everyone's spine. This leaves a lot to learn about retirement and pension plans, as they help individuals plan their lives and ensure financial stability.

Being financially stable is necessary, especially during our old age when we have stopped working completely. With no source of earning, it becomes challenging to manage our expenses. That is where pension plans play a dominant role.

Key Takeaways

|

Many people delay retirement planning, thinking they have enough time. However, starting early is key to building a strong retirement corpus. Even small contributions made in your 20s or early 30s can grow significantly due to compounding, reducing financial pressure later. Early planning also gives you flexibility to invest in growth-oriented options when young and shift to safer choices closer to retirement.

Investing early in pension plans like Pension4Life by Canara HSBC Life Insurance ensures you build a guaranteed income stream for life without compromising your current lifestyle. Remember, the sooner you begin planning, the more financially secure and worry-free your retirement will be.

Pension plans, in plain terms, are retirement plans that enable both the employee and the employer to pay a certain sum of money. These funds are put aside for the good of the employee. This money is then returned to the employee upon retirement.

A few pension plans in which an employee can choose to contribute a portion of their current income will potentially benefit them and their family as they retire.

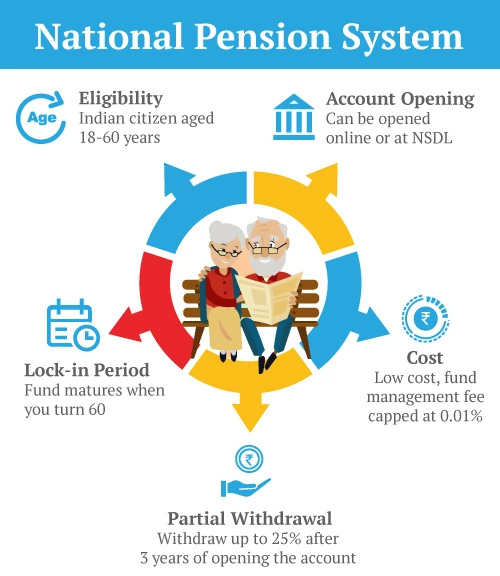

Pension schemes are the most widely used. The Indian pension scheme is made up of three parts. Civil servants' pensions, mandatory pension schemes administered by the Employees Provident Fund Organisation of India, and the National Social Assistance Programme for the unorganised sector together make up the Indian Pension Plans.

The most common pension plans in India are listed below. To choose the most effective option, you first must become familiar with the various plans available and choose the one that best suits your needs.

There are a lot of benefits that pension plans offer to individuals. Some of them are as follows:

Planning for retirement involves selecting the right partner who understands your needs and provides solutions that ensure a secure and worry-free future. Canara HSBC Life Insurance offers pension plans designed with deep expertise in insurance, banking, and customer-centric financial planning. Our pension plans combine the assurance of guaranteed income, flexibility in payouts, and comprehensive protection to help you live your golden years with dignity, confidence, and complete peace of mind. Some of the benefits are:-

Retirement is a significant milestone that requires thoughtful financial preparation to ensure comfort, dignity, and freedom from worries. Pension plans play an essential role in creating a stable income stream after you stop working, protecting you against rising living costs, inflation, and healthcare expenses. In a country like India, where social security systems are limited, investing in a pension plan becomes even more crucial for a secure future.

Canara HSBC Life Insurance offers a range of retirement and pension solutions designed to cater to your unique financial needs and goals. With our expertise, reliability, and customer-centric approach, you can plan your retirement confidently, knowing your future is in trusted hands. Start your retirement planning today with Canara HSBC Life Insurance and live your golden years with peace, security, and complete financial independence.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.