Written by : Knowledge Centre Team

2025-12-04

1150 Views

13 minutes read

Share

The fixed deposit has been one of the most popular and oldest investment plans in the modern financial world. You deposit a sum of money with your trusted bank for a limited time and receive a higher sum back at expiry. For many small savers, fixed deposits have been their first real exposure to the benefits of compound interest

However, the interest you receive n fixed deposits is fully taxable and must be reported in your income tax return under ‘Income from Other Sources'.

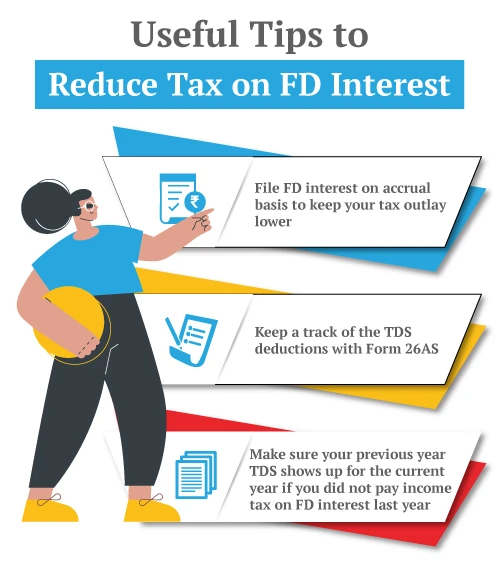

The interest you receive from a fixed deposit, either from a bank, post office, or corporation, is completely taxable and should be reported under “Income from Other Sources,” then taxed at your applicable slab rates.. You can choose to pay the tax in any of the following two ways:

Interest income that you earn from your term fixed deposits is fully taxable. Banks will deduct tax at source (TDS) on the interest income at 10% (20% if PAN is not furnished) if it exceeds:

The deducted TDS will show up on your Form 26AS, which reduces your final tax liability.

You will need to be careful while filing your FD returns on the receipt (cash) basis, as TDS applies to the accrued interest. So, make sure all your TDS for the years of accrual have been carried forward to the year in which you are receiving the interest.

The first question is, ‘can you avoid TDS on fixed deposit interest?’ Yes, you can, but only in the following cases:

While you do not need to do anything in the first case, in the second, you need to submit Form 15G (if you are a resident individual below 60 years of age) & 15H (if you are a resident senior citizen aged 60 or above) to the bank or financial institution.

Form 15G and Form 15H are self‑declaration forms through which you confirm that:

You are a resident (individual/HUF/other eligible person for 15G, or resident senior citizen for 15H).

Your estimated total income for the year is within the basic exemption limit under the chosen tax regime, and your tax liability (after deductions and rebate under Section 87A) will be nil.

Understand the difference between Form 15G and 15H.

From 1 April 2025, the TDS threshold on interest from bank fixed deposits has been increased to ₹50,000 (₹1,00,000 for senior citizens).

Source: TOI

The five-year tax-saving term deposits from banks and the post office give you a deduction under section 80C. You should note that this deduction is for the invested amount and not the interest.

Thus, you can claim a deduction of up to ₹1.5 lakhs on the invested sum. But any interest you receive from the deposit will become taxable in the year it accrues.

One of the easiest ways to reduce your tax liability for the financial year is to invest in tax-saving instruments. However, you should seek to reduce not only your present tax liabilities but also the future ones when the investment matures.

All tax-saving investments have one of the following three tax structures:

The following investment options fall in the first category, subject to the conditions prescribed in the Income Tax Act and rules:

Investing in these options not only reduces your annual tax outflow but also saves you from future taxable income.

Fixed deposits remain one of the simplest ways to grow your savings, but the interest they generate is fully taxable and must be planned for just like your salary or business income. By understanding how FD interest is taxed, when TDS applies, and how to use options like Form 15G/15H correctly, you can avoid unpleasant surprises at the time of filing your ITR.

At the same time, combining tax-saving FDs with smarter EEE‑type investments such as PPF, SSY, and eligible life insurance or ULIP plans can help you reduce today’s tax outgo and minimise taxable income in the future. When you align your FDs, deductions under Section 80C, and your chosen tax regime, fixed deposits can fit neatly into a broader, efficient tax-planning strategy rather than becoming a source of avoidable extra tax.

Yes. Interest earned on fixed deposits (including tax-saving FDs) is fully taxable and is added to your income under “Income from Other Sources,” then taxed at your slab rate.

Legally, tax applies in the year the interest accrues or is credited, even if you do not withdraw it, though many small investors practically offer it in the year of receipt and adjust for any TDS already deducted.

Yes. If your total interest with that bank crosses the prescribed annual TDS threshold and your PAN is updated, the bank/post office will automatically deduct TDS (typically 10%; higher if PAN is not given).

You need to add the total FD interest for the year to your income under “Income from Other Sources” in the appropriate ITR form (like ITR‑1/ITR‑2 as applicable), and then claim credit for any TDS reflected in Form 26AS/AIS. When filing your ITR, do not confuse interest paid vs interest accrual; you must reconcile the interest actually received with the total interest accrued and reported by the bank.

If your interest in a particular bank stays below the TDS threshold, TDS will generally not be deducted. If your overall taxable income for the year is below the basic exemption limit and your final tax liability is nil, you can submit Form 15G (below 60) or Form 15H (60+) to avoid TDS, even if FD interest is not your only income, as long as your total income keeps your tax liability at zero.

Yes, accrued interest is taxable income in India under the accrual basis for "Income from Other Sources," including FD interest credited each year, even if not withdrawn.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.