Written by : Knowledge Centre Team

2025-11-08

993 Views

8 minutes read

Share

Group term life insurance is a popular employee benefit for a lot of companies today. Insurance helps employers secure their employees’ families financially. Such benefits help the workforce to focus and relaxed about the safety of their family’s future.

It is a type of life insurance where one contract covers the whole group of people. Typically, a policy owner is an employer or business similar to a trade union and the policy includes employees or team members. Group term insurance is often provided as part of a comprehensive employee benefits package.

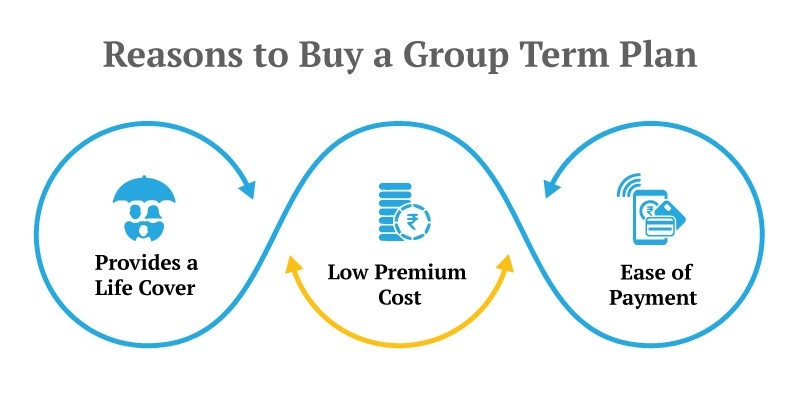

In most cases, the cost of group term insurance is much lower than what employees will pay for the same protection cover individually. So, this life insurance is a win-win deal for both the employer and employees. Also, if you do not have any other insurance, a group term life insurance will offer a basic safety umbrella.

Group term life insurance is a life insurance policy available to a group of people. If several people associate with each other for a common goal, such as employment, travel, borrowing, etc. the group can avail a term life insurance, which is known as a group term insurance as it is taken by a group of people.

For example, employers provide group insurance coverage to their employees. If you are covered under a group insurance plan provided by your employer, the employer usually pays most (and in some cases all) of the premiums.

The employer can claim the premium amount as a tax-deductible expense, while the employees receive the financial safety umbrella. The amount of your group term cover can be up to 10 times your annual salary.

Group life insurance policies are generally written as temporary insurance and are provided to employees who meet eligibility requirements, such as permanent employment or 30 days after employment. The availability of these term plans can be adjusted by appropriate life events or during open registration.

The average amount of coverage is usually equal to the annual salary of the combined work. Employers often pay most or all of the basic availability premiums. The additional value, usually multiplied by the employee's annual salary, is usually provided with an additional premium paid to the employee.

Group term life insurance has many distinct features which benefit the employees covered under the plan and the employer providing the cover. Some of the prominent features are:

There is no doubt that a group insurance plan is a clever way to find insurance coverage for a wide range of risk factors, let alone health.

With this program, you can choose to offer members of your group life cover by paying their premiums. Alternatively, members of your group can pay their own premiums while enjoying the lowest premium rates for the group program.

A person who pays a premium (either you or your members) may receive tax benefits in accordance with existing Income Tax laws.

* Tax laws are subject to periodic amendments.

Team members using the program receive a life cover benefit at a lower cost. In the event of a tragic incident, the program provides a number of death benefits to the nominee. This amount can protect you from debts such as loans taken by members.

Group term insurance plan has several benefits which your life insurance plan may not offer. Some of the important benefits are:

Normally, all employees are automatically enrolled in the base coverage when they meet the eligibility requirements. Requirements vary and may include working a certain number of hours per week or part-time as an employee. Availability of the coverage of group-term plans varies. In some programs, registration is only available when a person starts working or at a relevant milestone of life, such as the birth of a child. For some plans, additional coverage can be added during open subscription time.

Enhancing the plan by adding riders or benefits may require additional underwriting. Usually, it is a simple and easy-to-write process, where the insured individual ascertains their eligibility rather than going for a physical examination. The employer can then decide whether to offer additional coverage or not.

Group term life insurance plans allow you to receive all the benefits of each program under the same contract. They also offer tax benefits and lower premiums due to the presence of the group. Therefore, they are quite a popular option, and Canara HSBC Life Insurance offers plenty of group term plans for employers to choose from for their company.

The minimum and maximum age to enter a group term life insurance range from 14 to 18 years and 69 to 85 years, respectively. The maximum age for the cover is usually limited to 85 years.

The tenure of a group term life insurance plan is one year. The plan can be renewed every year and the new premium will depend on the number of claims filed in the last year and net additions to the group.

The minimum sum assured under the group term life insurance plan can range between Rs 1000 to 5000.

Group term life insurance usually charges only a risk premium. Thus, they do not offer any maturity benefit or return of premium options. However, you can buy iSelect Smart360 Term Plan from Canara HSBC Life Insurance and avail return of premium option with your term insurance.

Yes, group term insurance plans also offer riders like critical illness, accidental death cover, etc. Adding riders can increase the premium of the group term policy.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.