Written by : Knowledge Centre Team

2025-11-01

848 Views

5 minutes read

Share

We live in a time where inflation is a concern for every individual. It makes financial planning imperative for you at an early stage. With a financial plan, you get clarity on your financial goals that will come at different stages of life. To meet all your financial goals, you invest in financial instruments to address the various needs of protection.

You can achieve all your financial goals with a sound financial plan. However, life's journey is never smooth, and there can be some unexpected turns. You cannot see those at the start of your financial planning journey. However, you can prepare for them. An essential aspect of financial planning is to buy insurance plans to cover each financial goal.

For example, to preserve wealth, you have to make sure your existing savings continue to grow. However, in case of any critical illness to you or your loved ones, all your savings can drain.

You can have all-around protection through two plans - term plan and endowment plan. Let us look at the difference between the two and understand how each fits your financial planning.

The core purpose of a term insurance plan is to provide financial help to your family (nominee) in case of an unfortunate event of your demise. The sum assured in term insurance is high, and it can take care of outstanding EMIs, your child's education, and even household expenses.

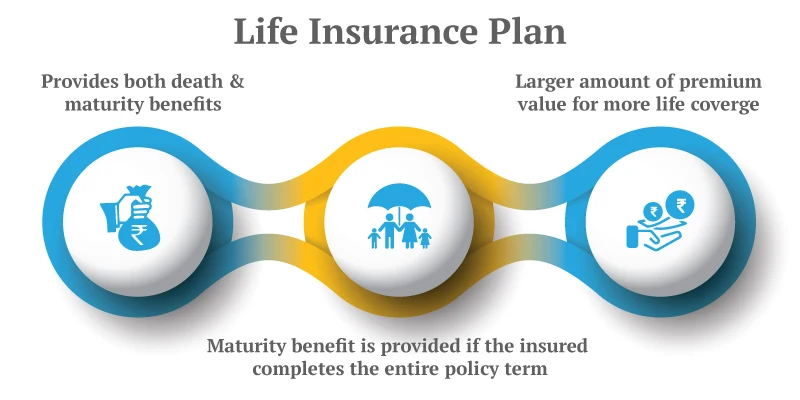

An endowment plan is also a life insurance plan, but this plan comes with an additional feature - these are also a saving plan. They help you save regularly over a specific period and get a fixed amount on the policy tenure completion.

With different investment and financial objectives, both plans differ significantly in both essential and value-added features. The most important primary features have been compared below:

The sum assured in a term plan is highest as it is designed to provide you only risk cover. It fulfils your need for protection.

In endowment plans, a small part of the premium goes towards the protection bucket. A significant percentage of your investment goes to the saving bucket. Hence, the sum assured is not high in an endowment plan.

Click Here to use Compound Interest Calculator

Term insurance is the least expensive life insurance product. With term insurance, you get maximum coverage by paying the lowest premium.

An endowment plan gives you a maturity benefit along with the risk cover. Participating endowment plans also offer you reversionary bonuses on maturity. The investment and growth options of endowment plans mean higher premiums.

Though most of the premium in an endowment plan is dedicated to investment, only a minor part goes to ensure a life cover.

Click to use : Term plan Calculator

In general, the term insurance plan does not provide you with any additional coverage option. However, Canara HSBC Life Insurance iSelect Smart360 Term Plan gives you the option for inbuilt coverages like accidental total and permanent disability benefit, child support benefit, and accidental death benefit.

Most endowment plans provide you with additional coverage options like protection against critical illness and accidental death benefits.

Also Read about Cashless Treatment

As mentioned above, a term insurance plan does not have any survival benefit. It means if you outlive the policy term, you won't get anything. However, with iSelect's Plan Option Life with Return of Premium option, if you outlive the policy term, you get back the total premium paid by you at maturity.

As endowment plans are saving plans, these plans give you a fixed amount plus loyalty addition at the end of the policy tenure.

With term insurance plans, the nominee can receive the sum assured in many ways in case of your demise. The payout can be as the lump sum amount, in equal instalments, or a combination of both. Depending on your need, you can customize your payment option by choosing one of the above options.

With endowment plans, the payment is made to you as lumpsum either as a maturity benefit or on the policyholder's death.

An essential question for you now must be - to choose both the plans or go with any one of the two insurance plans. You can go with both plans for different reasons. As discussed above, both solve different purposes. You can tag them against separate financial goals and make the most of these plans.

For long-term goals like a child's education or retirement, you need a lump sum amount. Also, these financial goals come with a hard date. Hence, you should invest in secure financial instruments. Having an endowment plan for such financial goals is the right thing to do. These plans act as wealth preservation for you. You can live your life peacefully knowing what you will get on maturity.

To prepare yourself for life's uncertainties and have long-term financial safety, you should also buy a term insurance plan. If something happens to you, all the financial goals will remain intact.

Also Read- Investment Plans

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.