Written by : Knowledge Centre Team

2025-10-07

927 Views

8 minutes read

Share

There are three broad kinds of insurance policies- term insurance, whole life insurance, and endowment policies. A whole life policy is one in which you pay a premium till the death of the insured. An endowment policy is one in which you pay a premium for a specific period and receive a payout in case of both death and maturity. A term plan is for a specified number of years with no maturity benefit. There are multiple variations of these two categories available in the market. Which one you go for depends on your family's financial needs and plans.

Key Takeaways

|

A term insurance policy is a plan that pays the sum assured if the policyholder passes away within the policy term. Term plans provide a much higher coverage at a relatively low premium. However, if you live out the entire policy term, there is no maturity benefit. Since there is a death payout only, it is advisable to go for as long a term as policy. A term plan is designed purely for the protection of the family. The death benefit they receive will be high enough to take care of their expenses adequately. This makes it the perfect choice if your family is financially dependent on you.

If you haven't been insured yet, you can check out the iSelect Smart360 Term Plan by Canara HSBC Life Insurance. It can be easily bought online and offers the option of increasing your cover by 25% every 5 years. This way, your sum assured can increase by 100% in the policy term and your family can be secured even with rising costs.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

When choosing a term insurance plan, consider:

If you are still deciding on a policy, the iSelect Smart360 Term Plan by Canara HSBC Life Insurance offers optional cover for accidental death and total and permanent disability, ensuring your family’s complete financial protection.

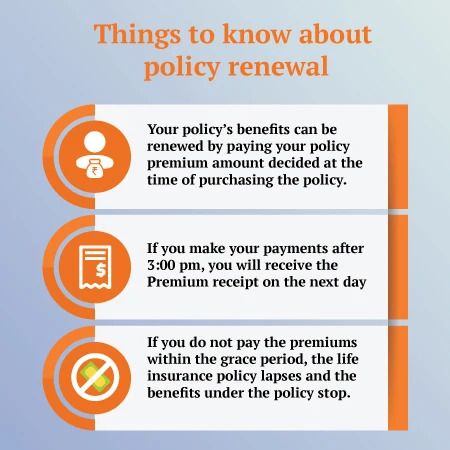

Renewing your term life insurance policy is crucial to ensure your family’s financial safety net remains intact without any gaps. Many people focus only on buying term insurance but often forget the importance of timely renewal. Regular renewal of your policy maintains your life cover without interruption, saves you from unnecessary extra costs in the future, and ensures continued protection for your loved ones.

Here are some key benefits of renewing your term life insurance policy:

The main purpose of a term insurance policy is to provide security to your family in the event of your death. However, if your policy matures and you don't renew it, it lapses and your family loses the security you have been paying for all this while. Non-renewal essentially defeats the purpose of term insurance.

A term insurance policy generally has no savings component. It is a pure life cover. If the policy matures and you do not renew it, you receive no return for all the premiums you have paid. Your paid premiums essentially become a loss. If you go for term insurance policy renewal and keep paying premiums, it extends your cover for premature death. Your family remains assured of their financial well-being in your absence. Moreover, the premiums are also minimal. So it should not be a huge financial burden to pay it regularly.

When you first buy a term insurance, a lot of factors like your age, medical history, family situation, etc. are taken into consideration. If you simply opt for term insurance policy renewal, you might not have to go through the entire process again. You might have to undergo medical tests again, but this depends on your insurer. However, if your policy lapses, you will have to go through the entire procedure again and could end up paying more by way of interest, higher premium amount, etc. Many times, people stop paying term insurance premiums because there is no paid-up value. The policy then lapses, and they lose all the premiums they have paid. Then they have to opt for a new policy which ends up costing them more.

Premiums paid for an insurance policy are tax-deductible under Section 80C of the Income Tax Act. If you stop paying premiums in order to save money, you also lose out on the tax benefit and might end up with a greater taxable income. The death benefit of a term insurance policy is also exempt from tax under Section 10(10D) of the Income Tax Act.

If you have been thinking of a term insurance policy and haven't zeroed in on one yet, make sure you check out the iSelect Smart360 Term Plan by Canara HSBC Life Insurance. It offers optional cover for accidental death and accidental total and permanent disability.

Despite its advantages, term insurance is often misunderstood. Common misconceptions include:

“I get nothing if I survive the term.”

Yes, but the main aim is to protect your family. Some plans today offer Return of Premium options if you want maturity value.

“I am too young to buy insurance.”

Buying early locks in lower premiums as health risks are lower when you are young.

“My employer's cover is enough.”

Employer-provided cover usually ends when you leave the job and is often insufficient for your family’s needs.

The claim settlement ratio is crucial because it reflects the insurer’s reliability. A higher ratio indicates:

Buying term insurance online offers:

For example, iSelect Smart360 Term Plan by Canara HSBC Life Insurance can be purchased completely online with instant premium quotes.

Term insurance is one of the most effective ways to protect your family’s financial future in your absence. Renewing your policy on time ensures that this safety net remains uninterrupted, helping you avoid unnecessary costs and maintain valuable tax benefits. It is important to assess your coverage regularly, choose the right riders, and opt for plans that grow with your family’s needs.

Canara HSBC Life Insurance offers comprehensive term plans like the iSelect Smart360 Term Plan, which provide high life cover at affordable premiums and allow you to increase your sum assured over time. By choosing the right term insurance and renewing it diligently, you can give your loved ones the peace of mind and financial security they truly deserve.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.