Written by : Knowledge Centre Team

2025-10-07

1129 Views

8 minutes read

Share

Insurance is a contract where the insurer accepts a specific amount of risk for a specific amount of premium cost. How you enter into this contract with an insurer is a step by step process which involves the assessment of the following two factors: Financial capacity or Human Life Value and Individual risk of illness & death.

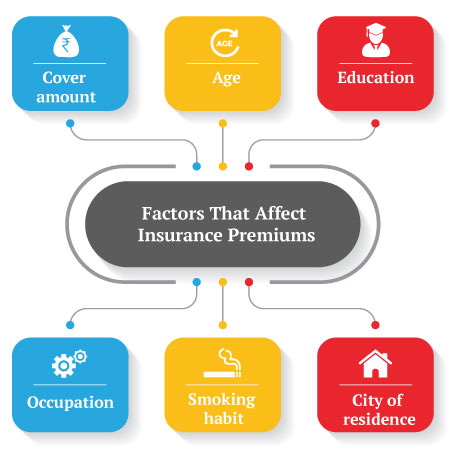

The truth is, the premium quote you see initially is based on standard assumptions. The final premium, however, reflects your unique risk profile, which includes factors like your age, medical history, lifestyle habits, occupation, and even your income level.

So, if your term insurance premium was revised, it’s not an error. It’s the insurer recalibrating the premium to match the level of risk they’re taking on.

Key Takeaways

|

Think of it this way: when you first check a quote online, it’s like a ballpark figure. But once you fill in the proposal form and undergo medical tests, the insurer gets a much clearer picture of your health, lifestyle, and earning capacity. Based on this information, they reassess the premium or coverage amount.

To truly understand why this happens, you need to look at how insurers evaluate risk in the first place, which is exactly where we’ll begin.

Insurance is a contract where the insurer accepts a specific amount of risk for a specific amount of premium cost. How you enter into this contract with an insurer is a step-by-step process which involves the assessment of the following two factors: Financial capacity or Human Life Value, and Individual risk of illness & death.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Other factors which may have some influence on the general life-expectancy are the state of residence, etc.

Understanding how insurers calculate your premium can demystify the revision process. They use underwriting guidelines backed by actuarial data, essentially, large-scale statistical models, to assess your risk level. Here's how it works:

Medical underwriting: Your blood pressure, BMI, cholesterol, and other test results are analysed. If anything falls outside the 'normal' range, your premium may increase.

Lifestyle risk assessment: Smokers, heavy drinkers, or individuals in high-stress or dangerous jobs are flagged as higher risk.

Creditworthiness & financial behaviour: Some insurers even consider your financial discipline and stability while setting premiums.

This risk-based pricing ensures fairness. People with higher risk contribute a little more, which allows premiums to stay affordable for everyone else.

When you first check your term insurance premium online, using a calculator or getting a quick quote, you’re being shown a standard premium. This is a base estimate created for someone in your demographic profile, assuming average risk levels.

Age: Younger applicants are generally considered lower risk and are quoted lower premiums.

Gender: Statistically, women have higher life expectancy, so their base premiums are usually lower.

Policy Term and Sum Assured: A longer policy duration or a higher coverage amount (sum assured) leads to a higher base premium.

Occupation Type (general category): Desk jobs may be rated as lower risk than physical or hazardous jobs, but the standard premium assumes the lower-risk group unless stated otherwise.

Smoker/Non-smoker Declaration (self-reported): Some tools allow you to declare this upfront, but it's often validated later.

After you deposit the standard premium, you need to complete the application form and go through a medical check-up. The application form will pick up any information about your personal risks that you provide. The rest of the health risks will be assessed during the medical examination.

Based on all this information the insurer will assess your personal risk for the life cover and any add-on covers you have selected. The insurer may revise your premium estimate, or the life cover provided if:

If only your HLV is lower, the insurer will reduce the policy sum assured instead of changing the premium amount. However, if the insurer considers you to be higher risk but your HLV estimates are good, you can secure the cover with a slightly higher premium.

When your premium is revised, you are expected to deposit the difference and avail yourself of the policy. Ideally, this is precisely what you should do, as going to another insurer with the proposal is only going to take time. Chances are the other insurer will also revise your premium quote based on your risk profile.

In some cases, yes. If your premium has been revised based on medical test results that you believe are inaccurate, you can:

Request a copy of your medical report

Seek a second opinion or retake tests (especially if you suspect an error)

Share any past medical records that support your claim of good health

If you provide stronger evidence, the insurer may reconsider your case. However, keep in mind that insurers follow strict medical underwriting norms, and revisions usually aren’t made arbitrarily.

Life insurance is a contract of trust. Unlike a normal business contract, life insurance requires full disclosure from both parties. You can find everything about the life insurance company on their website or with the regulator. While applying for life cover, it is your responsibility to declare all relevant information as correctly as possible for you.

If you happen to hide important facts which may influence your premium or life cover estimates, you may face the following issues:

Rejected life insurance proposals reflect badly on your trust record with life insurers, and they may refuse insurance to you at all. Also, if the risk to your life is higher, it is all the more important for you to have life cover as soon as possible.

So, don’t worry about a ₹ 1000 increase on your annual term insurance premium, your family would still be better off with this little outflow.

A revision in your term insurance premium doesn’t mean something went wrong. It means the insurer took the time to truly understand you, your health, lifestyle, income, and risks, and offered a protection plan tailored to your unique life profile.

While it's natural to feel unsure when the premium increases, remember: this isn’t just a cost, but a reflection of the value and risk associated with your life cover. In the long run, a slightly higher premium is a small price to pay for the peace of mind and financial protection it offers your family.

By being honest in your disclosures, proactive in understanding the process, and willing to pay the adjusted premium, you’re not just buying insurance, you’re building trust, security, and long-term stability for your loved ones.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.