Written by : Knowledge Centre Team

2026-02-20

907 Views

5 minutes read

Share

Buying a term insurance policy helps you protect your family against financial instability if something happens to you. You can opt for a significant amount of coverage (or Sum Assured) under a term plan by paying a lesser premium than other life insurance plans. The availability of coverage and associated premium amount, however, depends upon various factors such as your age, annual income, and most importantly, your lifestyle and health status.

Insurance companies require applicants to take a complete body medical examination for term insurance before issuing the policy with a high sum assured. This is applicable for both traditional term insurance plans and term insurance for spouse cover. Here is why undergoing a medical test can be necessary while buying term insurance. Learn more in this blog.

Key Takeaways

|

Undergoing a medical test for term insurance coverage is mandatory, in either or both of the cases mentioned below:

Your age is 40 or above

You have chosen a sum assured of ₹1 crore term plan or more

There are some term insurance policies which do not require you to undergo a medical examination for term insurance, up to the age of 40 or 45 years. Insurance companies may similarly provide relaxation for term insurance medical test requirements for applicants aged less than 45 years and for coverages up to ₹20 or 25 lakhs.

However, if you have any pre-existing illness, family history of health or hereditary conditions, the insurers would require you to take a medical test for term insurance, irrespective of your age and opted sum assured. Overall, the requirement of term insurance medical tests is subject to the underwriting policies of the insurer. You should, therefore, go through the medical grid of the insurance company to determine the age and sum assured for which a term insurance medical test is mandatory.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Insurance companies assess your health status to determine whether you have any existing health conditions or a history of medical issues, which might later increase the probability of a claim. In case you have any health issues that may increase your chances of premature demise, the insurance company may increase the premium payable, put restrictions on the sum assured, or even reject your term insurance proposal, based on your medical test results.

On the other hand, if your health is normal, the insurance company may offer insurance coverage without additional terms and conditions. Term insurance plans require medical test reports to verify the information provided in the application. These reports help the insurance company estimate your risk profile before deciding on the available coverage and the applicable premium.

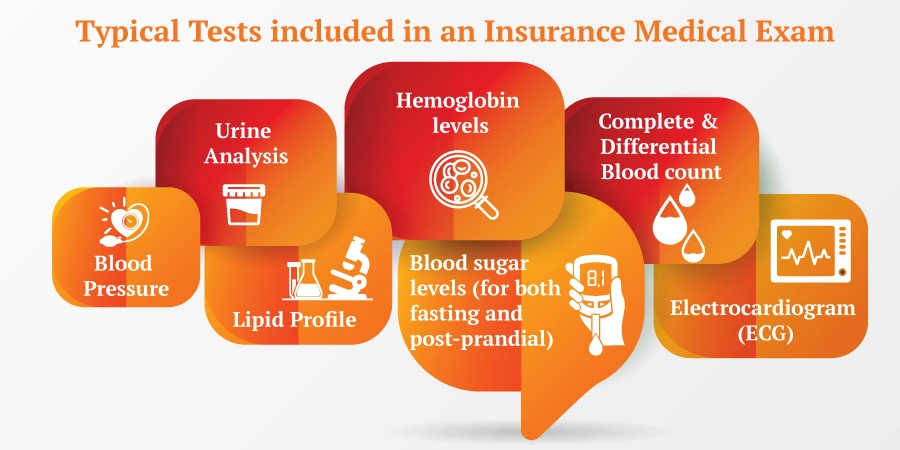

The medical tests required vary for each applicant, depending on the declarations in the insurance application. Routine tests include measurements of weight, height, and BMI, along with the following:

Blood pressure

Blood sugar

Complete blood count

Urine test

ECG (Electrocardiogram)

For higher ages and sum assured amounts, additional tests such as treadmill test, EEG, HIV I & II, hormonal and cholesterol assays may be included. Further tests may be required if you have a history of ailments like diabetes or hypertension, or addictions.

To get more information about your health, first calculate your BMI.

BMI or Body Mass Index is a broad measure of your body fat to work out if your weight is healthy.

*Disclaimer: The BMI Calculator provides an estimate based on height and weight and is for informational purposes only. It does not consider factors like muscle mass, bone density, or fat distribution, which can impact health. Results should be interpreted with caution and alongside other health indicators. Users are responsible for their health decisions and should consult a healthcare professional for accurate assessments.

Preparing well for your term insurance medical test can ensure accurate results. Here are simple tips:

Get adequate sleep before the test day.

Avoid caffeine, alcohol, and tobacco for at least 24 hours before the test.

Stay hydrated by drinking sufficient water.

Do not skip meals, especially if fasting is not required for the test.

Carry all previous medical records and prescriptions, if any.

These preparations will help you complete the medical tests smoothly and avoid any unnecessary delays in policy issuance.

Undergoing medical tests before buying a term insurance plan comes with the following benefits:-

At Canara HSBC Life Insurance, our requirement for medical tests varies from case to case. If you are looking to opt for comprehensive term insurance coverage and wonder if you would need to undergo a medical examination, feel free to connect with our team of life insurance specialists and discuss your queries.

Undergoing a medical test before buying a term insurance plan is an important step to ensure that your policy is issued smoothly and your family receives the full benefits without any hassles. It helps insurance companies accurately assess your health risks and provide you with the most suitable coverage at affordable premiums.

At Canara HSBC Life Insurance, we offer customised term insurance plans that prioritise your family’s financial security with minimal procedures and maximum transparency. If you are planning to buy a term insurance policy, consult our team to understand the medical test requirements and choose a plan that best protects your loved ones

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

Canara HSBC Life Insurance offers online term insurance plans to secure your family financially in your absence.