Written by : Knowledge Centre Team

2026-02-05

3914 Views

8 minutes read

Share

Financial planning is crucial for sustaining the current economy and it applies to every individual, irrespective of their job type. However, self-employed and freelancers carry the burden of having an uncertain income, and so they must get involved in formulating a suitable financial plan.

Key Takeaways

|

With financial planning, they can acquire fiscal safety and assurance when conditions are unstable. Unlike salaried individuals, freelancers don’t have access to benefits like provident fund, employer insurance, or fixed monthly income.

This makes it even more important for them to be proactive about budgeting, saving, and risk management.

A well-structured financial plan helps in meeting day-to-day expenses and also ensures long-term stability and growth.

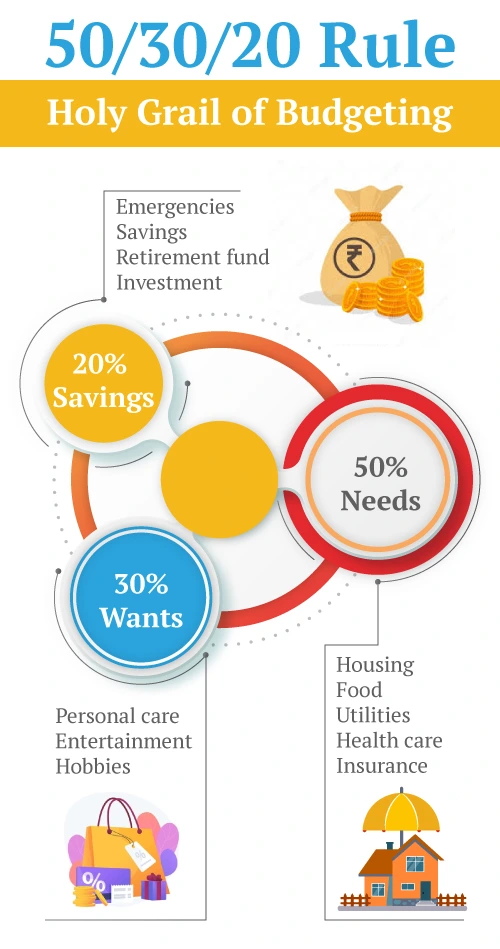

Planning out your finances is not easy and requires appropriate knowledge and contemplation. Here are a few definitive steps that your financial plan should include:

Moreover, you could consider opening a high-interest savings account that provides you flexible fund withdrawal, without increasing the interest rate on the balance. Your business bank account should benefit your financial structure in several ways.

Learn these 6 easy budgeting tips for long-term financial strength.

A term insurance cover is another smart investment, to protect your family after you. The iSelect Smart360 Term Plan by Canara HSBC Life Insurance offers multiple premium payout options, cover for the spouse, and increased coverage options.

Income plans are extremely beneficial as they are tax-efficient, being tax-free under section 10(10D). The insurance income plans are based on pre-decided investments and time intervals, establishing minimum customer intervention in the whole process.

Here are 6 benefits of buying saving plans with guaranteed income.

Finance is a life aspect where uninformed decisions can cost you heavily. Diligent financial planning is essential and all of these tips have to be implemented while doing so. Being self-employed and a freelancer comes with extra responsibilities as you do not have an institution to fall back on. With an effective financial plan, you can continue to be your boss without worry.

While planning your finances is essential, being aware of common mistakes can save you from unnecessary stress and monetary setbacks. Here are a few real-life errors that freelancers and self-employed professionals should steer clear of:

Avoiding these mistakes doesn’t require drastic changes, just conscious, informed decisions. By learning from these missteps, you can build a resilient and reliable financial base for your freelance journey.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Financial independence doesn’t just mean working on your own terms; it also means taking full responsibility for your financial well-being. As a freelancer or self-employed professional, you don’t have the safety nets that salaried individuals often rely on. That makes proactive financial planning not just advisable, but essential.

By creating a clear roadmap, budgeting smartly, preparing for uncertainties, investing wisely, and safeguarding your future, you empower yourself to thrive in the world of self-employment without stress.

Start today, and your future self will thank you.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.