Written by : Knowledge Centre Team

2026-02-19

1925 Views

8 minutes read

Share

When you are young, retirement feels far away and full of possibilities. But for many, the reality is quite different. A vast majority of senior citizens endure retirement, rather than enjoy it. Needless to say, health-related issues are one of the major woes afflicting the older population. But money is a bigger challenge. Financial insecurity is the biggest impediment to leading a comfortable retired life. There are a lot of investment options that are essential for a comfortable retirement.

Key Takeaways

|

The majority of the working population lives paycheque to paycheque, putting themselves at grave risk for the future. To ensure a comfortable retirement, there are three challenges that if addressed early in life can make retirement financially comfortable:

These three pillars lay the foundation for financial independence in your later years.

Considering the overall inflation rate to plan for retirement could be detrimental. You must consider what will remain relevant to you over the years. Both healthcare and food costs account for a major portion of senior citizens living expenses.

Instead of getting lost in complex calculations involving inflation, compounding, and returns, focus on a key question:

You can consider the complicated estimates and time value of money, including the inflation and rate of return on your investments. However, it all boils down to one simple factor – what percentage of your income are you saving towards your retirement?

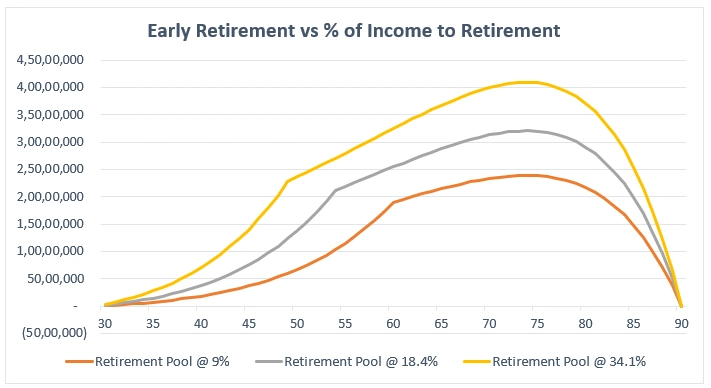

Figure 1 shows the accumulation and depletion of the retirement corpus built at different saving ratios. Here’s what it shows:

These scenarios assume the following:

This should give you an idea about how much of your income going to your retirement funds will ensure that your retirement is financially secure.

Learn the top mistakes to avoid while planning for your retirement.

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Both Saving and Investing may, prima facie, look very similar but are contrastingly different. Setting aside some money each month right from the day you start earning is quintessential. Without regular savings, you may end up with little or no funds after retirement.

Investing helps your money grow over time. When you invest your savings in financial tools like Fixed Deposits (FDs), Public Provident Fund (PPF), National Pension Scheme (NPS), your money grows at the specific rates of interest as announced by the bank or government. For example, FDs offer rates between 4% to 8% depending on the bank and tenure.

However, saving and investing alone may not be enough to maintain the lifestyle you're used to. To ensure your hard-earned money does not erode in value over time, the money must grow faster than the rate of inflation.

Also Read : Saving Vs Investment: Which is Better?

Both saving and investing are essential parts of financial planning. Saving helps you build a safety net for emergencies and short-term goals. Investing, on the other hand, is what grows your wealth over time and helps you beat inflation.

Here’s how they differ:

In short, saving keeps your money safe, but investing helps your money work harder. A balanced combination of both is the key to a financially secure retirement.

If you “save” money in non-interest bearing assets or leave it idle in a basic savings account, it gradually loses value over time.

For example:

Your real return becomes =3%-6%= (-)3%

This means your savings are effectively shrinking. Over time, the money you set aside buys less, not more. Here’s a simple illustration

Both these examples demonstrate the need to focus on “wealth creation” rather than keeping money aside or “investing” in low-income yielding instruments.

Any investment should be a well-thought-out process keeping in view long-term goals, the security of the family, and the education of children. Canara HSBC Life Insurance offers some of the best retirement plans in India. One of these is the Pension4Life Plan. It is another safe long-term investment plan that gives you income streams, post-retirement, called “annuities” till the end of your life after which the purchased/invested amount would be given to your nominee.

Retirement planning is less about predicting the future and more about preparing for it. By understanding the impact of inflation, making smart saving and investment choices, and focusing on long-term wealth creation, you can build a retirement life that’s not just secure, but comfortable and fulfilling. The key is to start early, stay consistent, and adapt your plan as life evolves. Your future self will thank you for the steps you take today.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.