Your expected retirement age

Your expected retirement age Life-expectancy

Life-expectancy Health condition

Health condition Current income

Current income Current age

Current age- Vesting Age: When pension plan matures for withdrawals or annuity purchase, often customizable from 40-85 years in retirement schemes

- Corpus: Accumulated retirement savings from contributions and returns, used for lump-sum or annuity payouts post-vesting

- Annuity: Regular income stream from pension corpus, immediate (post-lump sum) or deferred, ensuring lifelong payments

- Deferred Annuity: Lump-sum investment grows during the deferment period before starting regular lifelong payments

- ULIP: Unit-linked Insurance Plan; a life insurance plan offering life cover plus market-linked investments for wealth creation

Retire Stress-Free with Guaranteed Income

Enter OTP

An OTP has been sent to your mobile number

Didn’t receive OTP?

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Request Registered

Thank You for submitting the response, will get back with you.

Complaint Registered

. Please use this ID for all future communications regarding this concern.Request Registered

Thank You for submitting the response, will get back with you.

Request Registered

Thank You for submitting the response, will get back with you.

Sorry

Table Of Content:

0

1

1.

What is Retirement Planning?

0

2

2.

What are Retirement and Pension Plans in India?

0

3

3.

Secure Your Retirement with Guaranteed Income Plans

0

4

4.

How Do Pension Plans Work?

0

5

5.

Types of Retirement & Pension Plan Schemes in India

0

6

6.

Pension Plans vs PPF vs NPS: How Do They Compare?

0

7

7.

Who Should Invest in a Retirement Plan?

0

8

8.

Retirement Planning by Life Stage

0

9

9.

Retirement - Top Selling Plans

10

10.

How to Plan for Retirement: A Step-by-Step Guide

11

11.

4 Steps for Retirement Planning

12

12.

How Much Should You Contribute to Your Retirement?

13

13.

Retirement Calculator

14

14.

How To Use the Retirement Calculator?

15

15.

Why Start Retirement Planning Early?

16

16.

Reasons to Start Retirement Planning Today

17

17.

Benefits of Buying a Retirement Plan

18

18.

Tax Benefits of Retirement Plans

19

19.

How to Choose the Best Retirement Investment Plan in India?

20

20.

How Much Do I Need to Retire?

21

21.

Documents Required to Buy a Retirement Plan

22

22.

Retirement Planning Guide for Working Women

23

23.

Glossary

24

24.

FAQs for Retirement Plans

25

25.

Related Blogs

A comprehensive retirement plan can help you stave off the worries of inflation and living costs during your golden years. The key to a fulfilling retirement is to plan early and use the best retirement plans possible to achieve your goal.

Key Takeaways

|

What is Retirement Planning?

Retirement planning is the process of deciding the goals to pursue after retirement and the roadmap to achieve those goals. You no longer receive a paycheck once you retire, and thus have to rethink a few things. You have to assess where the income will come from, how you will meet your expenses, and how much your savings are. All these things make up the term retirement planning.

Though no time is perfect, you should start planning for retirement as early as you can. The earlier you start planning for your finances, the better it will be for you once you reach the retirement stage.

What are Retirement and Pension Plans in India?

Retirement plan and pension plan are names you will hear commonly for saving plans designed to serve your post-retirement financial needs. However, the meaning of a retirement plan may differ slightly from that of a pension plan.

Pension plans are a type of investment in which an employee is required to allocate a portion of their savings to a fund over a specified period. This saving will help you build a substantial corpus, enabling you to have a secure financial future. Retirement/Pension plans provide financial stability by offering a steady income after retirement, ensuring that you can live comfortably without worrying too much about finances.

A few examples of retirement plans are the Employee Provident Fund (EPF), New Pension Scheme (NPS), Public Provident Fund (PPF), etc. Whereas pension plans would be the annuity plans that will offer a monthly income from the invested money.

Secure Your Retirement with Guaranteed Income Plans

Enter OTP

An OTP has been sent to your mobile number

Didn’t receive OTP?

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder as on

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Sorry ! No records Found

Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

How Do Pension Plans Work?

Investing in a pension plan requires you to contribute a certain sum to a fund over time. This can be done either regularly or in a lump sum. These payments which you invest in your pension plan help build your corpus through the years. This corpus is used to provide you with regular payments that you can use to meet your expenses once you retire. Thus, a pension scheme makes sure that your income flow does not stop even after retirement.

- Investing in a Pension Plan: A pension plan begins with regular contributions made by an individual or their employer. These contributions can be made either monthly, quarterly, or yearly, depending on the plan type. Investments are made in various financial instruments, such as mutual funds, government bonds, and fixed deposits, to grow the corpus over time.

- How Corpus is Built Over Time: The accumulated amount in a pension plan grows through compounding returns and market-linked investments. Pension plans often offer different investment strategies (conservative, balanced, or aggressive) based on the risk appetite of the investor. The longer the investment duration, the larger the corpus, ensuring a substantial fund for post-retirement needs.

- Regular Income Post-Retirement: Once the policy matures, the accumulated corpus is used to provide a steady income stream. Depending on the plan, retirees can opt for annuity payments, lump-sum withdrawals, or a combination of both. Annuity payments can be fixed or linked to inflation to ensure sustained financial support.

- Ensuring Financial Stability: Pension plans act as a financial cushion during retirement, covering daily expenses, healthcare costs, and lifestyle needs. Choosing the right pension plan with adequate coverage helps retirees maintain financial independence and avoid reliance on family support. Additionally, tax benefits on contributions and withdrawals add to the plan's overall advantages.

Types of Retirement & Pension Plan Schemes in India

A retirement pension scheme can be either a government-backed plan or a private annuity from a life insurance company. These are designed to help individuals build a steady income after retirement by combining long-term savings with financial security.

- Immediate Annuity: An annuity is payable immediately, as per the payment frequency chosen, at a constant rate in arrears. Premium is paid in a lump sum at the beginning of the annuity plan.

These are pension plans more than investment plans for retirement, are best used near or after retirement once you have accumulated your retirement funds.

- Deferred Annuity: An annuity is payable post Deferment Period, as per the payment frequency chosen, at a constant rate in arrears. Premium is paid in a lump sum at the beginning of the annuity plan.

You can invest in multiple such plans to start your pension at or after retirement. Your investment continues to grow while you wait for the annuity to start in the deferment period.

- Pension plan With Life Cover: This pension plan includes insurance coverage that entitles your dependents to a lump sum in case of an unfortunate event. Such plans are best for you if your spouse is financially dependent and is younger than you.

- Pension Plan Without Life Cover: This plan pays out the corpus built to date to the nominees in case of an unfortunate event. There is no life cover (sum assured) in these plans. Due to the lack of life cover benefit, this plan will only transfer the remaining corpus to your nominees upon your death.

- Unit-Linked (Market Linked) Retirement Plan: A market linked retirement plan invests your premiums in equity and debt funds, depending on your risk appetite to build a corpus that is paid out at maturity. These plans are great for long-term corpus growth. So, if your risk appetite and age allow for equity exposure, use Unit-Linked Pension Plans to build your retirement funds faster.

- National Pension Scheme (NPS): The NPS is a government-backed retirement savings plan designed to provide financial security after retirement. It is a voluntary, long-term investment plan regulated by the Pension Fund Regulatory and Development Authority (PFRDA).

Under NPS, individuals contribute regularly to their pension accounts, and the funds are invested in a mix of equities, corporate bonds, and government securities based on their chosen asset allocation. Upon retirement, a portion of the corpus can be withdrawn as a lump sum, while the remaining amount is used to purchase an annuity, ensuring a steady income. NPS offers tax benefits under Section 123 and 124 of the Income Tax Act (previously referred to as Section 80C and 80CCD(1B) of the Income Tax Act 1961, respectively), making it an attractive option for retirement planning. - Government-Backed Retirement Schemes (EPF, PPF, APY): Beyond NPS, the Indian government offers several other retirement-focused savings schemes that form the backbone of financial security for millions of Indians.

- Employees' Provident Fund (EPF): A mandatory retirement savings scheme for salaried employees in organisations with 20 or more employees. Both the employer and employee contribute 12% of the basic salary each month to the EPF corpus, which earns a fixed, government-declared interest rate. The accumulated corpus, along with interest, is payable to the employee upon retirement and is fully exempt from tax subject to applicable conditions.

- Public Provident Fund (PPF): A voluntary, long-term savings scheme open to all Indian citizens, including self-employed individuals. PPF follows an Exempt-Exempt-Exempt (EEE) tax structure; contributions, interest earned, and maturity proceeds are all tax-free. The scheme has a lock-in period of 15 years and currently offers a government-declared interest rate of 7.1% p.a., making it one of the safest retirement savings instruments available.

- Atal Pension Yojana (APY): A government-backed pension scheme primarily targeted at workers in the unorganised sector. Subscribers can choose a fixed monthly pension of ₹1,000 to ₹5,000 per month after the age of 60, depending on their contribution amount and age at entry. The government also co-contributes for eligible subscribers, making APY an accessible and affordable pension option for those without formal employment benefits.

Pension Plans vs PPF vs NPS: How Do They Compare?

Pension plans in India broadly fall into two categories: government-backed schemes and private annuity plans from life insurance companies. Compare the best pension plans in India alongside PPF, NPS, and government schemes to find the right fit:

Parameter | Pension Plans (Annuity/Life Insurance) | PPF (Public Provident Fund) | NPS (National Pension Scheme) |

Return Type | Guaranteed (traditional) or Market-linked (ULIP) | Fixed, government-declared rate (currently 7.1% p.a.) | Market-linked (equity, corporate bonds, govt. securities) |

Risk | Low to Moderate | Low | Low to Moderate |

Tax Benefit | Premiums deductible under Section 123 (Section 80C) | Contributions are deductible under Section 123 (Section 80C); the maturity amount is tax-free | Section 123 (Section 80C) + additional ₹50,000 under Section 124 (Section 80CCD(1B)) |

Lock-in Period | Until policy maturity/retirement age | 15 years | Until age 60 |

Liquidity | Low (partial withdrawals subject to plan terms) | Partial withdrawal allowed from the 7th year | Low (partial withdrawal allowed in limited circumstances) |

Annuity Requirement | Optional (plan-dependent) | Not applicable | Mandatory (minimum 40% of corpus must be used to purchase an annuity |

Who Should Invest in a Retirement Plan?

The right time to invest in a retirement plan is always now, regardless of your age, profession, or life stage. Here are five profiles that can benefit significantly from starting or strengthening their retirement planning today.

- Young Professionals (20s-30s): Start early to maximise compounding and build a large retirement corpus with smaller contributions. Lower premiums and higher risk appetite make market-linked options like ULIPs or NPS suitable for long-term growth.

- Self-Employed Individuals: Without EPF or gratuity, retirement planning is essential. Irregular income makes disciplined investing critical. Flexible options like NPS or annuity plans help build a steady post-retirement income independent of business performance.

- Mid-Career Individuals (30s-40s): With rising income and responsibilities, focus on balancing growth and stability. Combine market-linked plans with annuities, and review existing savings to stay aligned with retirement goals.

- Pre-Retirees (50s): Shift focus to preserving wealth and generating a steady income. Evaluate savings adequacy and opt for immediate or short-deferment annuity plans while accounting for inflation and healthcare costs.

- Women: Longer life expectancy and career breaks make retirement planning crucial. Lower lifetime earnings can impact savings. Pension plans with life cover and annuities help ensure long-term financial independence and security.

Retirement Planning by Life Stage

Retirement planning is not a one-time activity. It evolves as you move through different phases of life. Your income, responsibilities, and risk appetite all change with age, and your retirement strategy should reflect that. Here is a stage-wise guide to help you stay on track at every step of the journey.

- Your 30s - Build the Foundation: Your 30s are the best time to lay the groundwork for a financially secure retirement. With fewer responsibilities and a longer investment horizon, you have the unique advantage of time, and time is what makes compounding so powerful.

- Aim to allocate 10-15% of your income towards retirement savings and lean towards equity-heavy instruments such as Unit-Linked Pension Plans or NPS, which offer higher growth potential over the long term

- Start small if needed, but stay consistent. Even modest contributions made in your 30s can snowball into a significant corpus by the time you retire

- Review your plan annually and increase contributions as your income grows

- Your 40s - Strengthen Your Portfolio: By the time you reach your 40s, your income has likely grown, and so have your financial responsibilities.

- This is the time to get serious and increase your retirement contributions to 15-20% of your income

- Shift towards a more balanced portfolio that blends market-linked growth with stable, lower-risk instruments

- Avoid the trap of lifestyle inflation; every incremental rise in income should translate into higher savings, not just higher spending

This is also a good time to consolidate your existing retirement investments, plug any gaps in coverage, and consider adding annuity products to your portfolio to lock in future income.

- Your 50s - Protect What You Have Built: In your 50s, the priority shifts from aggressive accumulation to capital protection.

- Increase your retirement contributions to 20-25% of your income and gradually move your portfolio away from high-risk, equity-heavy instruments towards debt-oriented and guaranteed return options

- Avoid dipping into your retirement corpus for any reason. Premature withdrawals can significantly derail your long-term plan

- This is the stage to get clarity on your expected retirement age, desired lifestyle, and estimated monthly expenses post-retirement

Consulting a financial advisor at this stage can help you fine-tune your withdrawal strategy and ensure your corpus lasts as long as you need it to.

- Your 60s and Beyond - Distribute Wisely: Retirement is here, and the focus now is on making your corpus work for you.

- Convert your accumulated savings into steady, reliable income streams through annuities, pension payouts, or other low-risk income-generating instruments

- Avoid parking large sums in high-risk investments at this stage, as capital preservation is paramount

- Budget carefully to ensure your corpus is not exhausted prematurely, and always maintain a separate emergency fund to handle unexpected healthcare or personal expenses

It is also a good time to review your estate plan, update nomination details across all financial instruments, and ensure your loved ones are adequately provided for.

Retirement - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Retire Grand with Flexi Benefits

Smart Guaranteed Pension

- Guaranteed Lifelong Income

- Limited premium payment term

- Multiple annuity options

- Option to defer the annuity payments

Save, Dream, Plan. Live Peacefully

iSelect Guaranteed Future

- 4 Plan options

- Option to choose premium payment term

- Get Tax benefits

- Premium protection cover

How to Plan for Retirement: A Step-by-Step Guide

Your retirement goal will differ from others depending on several factors involving your lifestyle and income during your employment years. Another factor that you should account for in your retirement goal is inflation.

Inflation is a crucial factor in retirement planning because it steadily reduces purchasing power and can significantly impact your lifestyle and expenses in your later years. As you progress in your retirement, your chances of earning from employment reduce, and so do your chances of correcting the investment mistakes.

Thus, the earlier you factor in inflation in your retirement goal, the better.

Other factors that will define your retirement goal are:

| Factors | Impact |

|---|---|

| A higher retirement age gives you more time to invest and grow your corpus. However, early retirement will give you less time to accumulate sufficient money. Also, you will need more money to sustain your extended post-retirement life. |

| A higher life expectancy extends your retirement period. Thus, you will need a larger corpus to sustain your living costs. Also, inflation will have a greater impact. |

| Health conditions and lifestyle affect your medical expenses in later years or during post-retirement life. Poor health and unhealthy habits may increase your medical expenses post-retirement. |

| Current income affects your lifestyle and overall living costs; it also determines the amount you can save now to meet your retirement goal. |

| The current age is the factor that will define how much time you have until retirement and how much of your income today should be allocated towards your retirement goal. |

Process of Planning for Your Retirement Goal:

Retirement goal planning is a simple process that. Consists of two distinct financial phases, – accumulation and distribution. The accumulation phase is when you are earning from employment and building your retirement pool.

In the distribution phase, you use the accumulated funds to replace your income from employment.

If you are 30 years of age and earning ₹ 10 lakhs per year at the age of 60, your first year’s monthly income will look as follows:

At 10% of your income | At 20% of your income | At 25% of your income |

₹ 92,457 | ₹ 1,84,915 | ₹ 2,31,144 |

*Disclaimer: Rate of return for the retirement funds has been assumed at 8% p.a.

This assumes that your annual income grows by 5% every year during your employment years. You will also withdraw your pension at a growing rate of 5% per year to account for inflation, until the age of 90.

You can also, look at these amounts as, “you can contribute a higher percentage of your annual income towards retirement to retire earlier.”

So, for the accumulation phase, your retirement goal may not account for your actual expenses but only your rate of contribution.

4 Steps for Retirement Planning

Retirement is the simplest goal to plan for if you follow the correct approach. Investing for a prosperous retirement is the only challenge with this goal. So, here is how you can go about it to keep it simple and rewarding:

- Step 1: Start By Saving At Least 10% of Your Income: Remember, your pension income and the success of retiring at your desired age depend on how much of your present income you save for a retirement goal. If you have 30 years to spare, the best you can do under Indian economic conditions is to invest at least 10% of your take-home income towards your retirement goal. This should be a safe investment in long-term pension or retirement plans.

- Step 2: Start Investing Small Amounts in Equity Funds: If you have more than 10 years before you retire, start investing small additional amounts in equity funds. The best way to allocate your money to equity is through Unit-Linked Insurance Plans, as you not only get the tax benefits but can also manage your portfolio risk automatically. You should aim to increase this contribution to at least 5% of your annual take-home income.

- Step 3: Add Long-Term Assets to Your Portfolio: Adding inflation-linked assets like house property for rental purposes and gold will help you continue to enjoy inflation-adjusted income even after retirement. Although such investments may be less liquid, they are useful in a post-retirement emergency, such as a low pension corpus.

- Step 4: Minimise Post-Retirement Tax: A monthly pension from a pension plan is taxable as salary income. Thus, you should add retirement plans that allow tax-free partial withdrawals, such as Unit-Linked Insurance Plans. This will help you reduce your tax burden post-retirement. Diversifying your savings across multiple assets is essential to achieve an important long-term goal such as retirement.

How Much Should You Contribute to Your Retirement?

The answer depends on your current age, expected retirement age and your contributions made so far. Simply put, you can follow the table below to decide the ideal contribution for your financially healthy retirement:

Saving an adequate amount is essential to your happiness after retirement. But what is that adequate amount?

The answer to this question depends on your current age as well as the contributions you have made so far. The retirement age is generally 60. So, if you decide to start contributing when you have 30 years left to retire, that is when you are 30, then setting aside 10-12% of your annual income will be good enough.

But as you grow older without investing, your required contribution will increase. If you have only 20 years to retire, then the amount you need to contribute each year will increase to 20% of your salary.

This effect is driven by the power of compounding returns, which is why you are advised to start investing early.

Years to Retire | Min. Contribution to Retirement Funds |

30 or more | 10% of annual income |

20 to less than 30 | 20% of annual income |

Less than 20 | 35% or more |

Less than 10 | 90% or more |

Assuming an ROI of 8% p.a. on retirement investments and the expected retirement age of 60

The less time you have, the higher your contribution has to be towards retirement. That is, unless you already have a pool of funds available.

Retirement Calculator

A retirement planning calculator is a simple tool that gives you an idea of the corpus you can accumulate with a regular monthly investment for your golden years.

1

My Retirement Age

2

Amount Invested

3

Additional Details

4

Our Recommendation

My Retirement Age

Amount Invested

Additional Details

Our Recommendation

Your Current Expenses are

Rs 50,000/month

Inflationary Expenses you will need post retirement

Rs 1,00,000/month

Hi {customerName}

We recommend to start Investing

Disclaimer-

The above calculation and illustration of figures are indicative only and not on actual basis.

How To Use the Retirement Calculator?

A retirement calculator helps you estimate how much you need to save for a comfortable retirement by factoring in income, expenses, and inflation over time.

- Submit Personal Information: Choose your current age and expected retirement age. The calculator gives you a conservative option for selecting retirement age up to 60 years only. If you plan to extend your employment beyond this age, this investment plan will only leave you in a better position.

- Enter Present Expenses & Savings: Your present monthly expenses will define the amount of money you will need as a pension after retirement. If you have already started investing towards your retirement or want to allocate an existing asset to this goal, enter the value in the ‘Current Savings for Retirement' field. Lastly, you can select an expected rate of return on this asset.

- Calculate the Goal & Required Investment Amount: After entering your expense and existing asset information, you can press the Calculate’ button to estimate:

- Your monthly expenses at the time of retirement

- The retirement corpus you will need

- The amount you need to invest every month to achieve these goals

Why Start Retirement Planning Early?

People often delay planning for their retirement owing to a false sense of having abundant time. However, retirement planning is not a task of a few weeks or even months; a fulfilling post-retirement life requires several years of disciplined planning and implementation. The earlier you start, the more you stand to gain.the earlier you start retirement planning, the better!

The 3 Stages of Retirement Planning: Regardless of when you begin, retirement planning moves through three distinct phases:

- Accumulation: In the first stage of retirement planning, you contribute regularly to a pension plan, carving out premiums from your monthly income. The corpus available at your disposal after retirement will depend on the number and size of contributions made during this phase. Starting early means more contributions over a longer period, and a significantly larger corpus at maturity.

- Preservation: The preservation phase kicks in approximately 10-15 years before retirement. As you near retirement, your lifestyle expenses tend to rise, and your risk appetite begins to fall. This is the stage to conduct a thorough review of your existing investments, assess your post-retirement requirements more accurately, and shift your portfolio gradually towards lower-risk instruments to protect what you have built.

- Distribution: The distribution phase begins when your regular employment income stops. This is the final phase of retirement planning, when the fruits of decades of disciplined saving begin to pay off. In this phase, you start receiving a monthly income from your pension plan to support your post-retirement expenses and maintain your desired lifestyle.

Reasons to Start Retirement Planning Today

Here are a few reasons you need to start planning right away:

- It Is Cheaper When You Are Young: Retirement plans offer dual benefits of insurance and investment. When you are young, your body is less prone to diseases, which reduces the risk for the insurer. Since insurance is a business of risk assessment, the premiums are lower for young policy buyers.

- The Power of Compounding: When you leave an investment to accumulate for a long time, the interest earned on the original investment also starts to generate returns. This leads to rapid accumulation, and the corpus grows exponentially. When you start investing early, compounding helps multiply the investment rapidly.

- More Time for Course Correction: All market-linked investments are inevitably risky. When you start investing early, you have ample time to monitor the performance of the investment and make necessary portfolio adjustments. Waiting too long leaves little room to correct gaps in your retirement corpus, a shortfall that becomes increasingly difficult to bridge as retirement approaches.

- Save More Tax Every Year: Investments in retirement and life insurance pension plans help you save tax annually under Section 123 of the Income Tax Act (previously referred to as Section 80C of the Income Tax Act), with deductions available on investments of up to ₹1.5 lakhs. Additionally, maturity value and partial withdrawals are exempt under Schedule II (Table S.No. 2) of the Income Tax Act 2025 (also known as Section 10(10D) of the Income Tax Act 1961). Starting early means you maximise these tax benefits year after year, building a larger corpus while reducing your annual tax liability.

- Counter Inflation Over the Long Term: Investing early gives your retirement fund more time to account for inflation and income growth. A corpus built over 25-30 years is far better equipped to absorb the impact of rising prices than one built over 10. Starting early ensures you can begin your pension without having to compromise on your lifestyle or standard of living.

- Retire Richer: The more time you give your money to grow, the larger your corpus will be at retirement. Since you cannot significantly shift your retirement date, it is better to start as soon as possible and give your investments maximum time for compounding to take full effect. An early start is the single most reliable way to ensure a wealthier, more comfortable retirement.

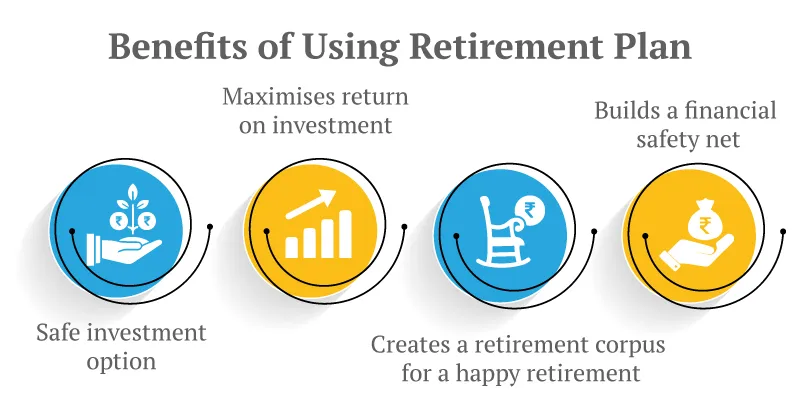

Benefits of Buying a Retirement Plan

Investing in a retirement plan does more than secure your post-retirement income. It offers a range of financial advantages that work in your favour throughout your investment journey.

- Safe & Reliable Income: Life insurance pension plans can offer the safest and most reliable long-term pension income

- Wealth Boosters: Retirement plans add bonus units and return to long-term investors portfolios

- Loyalty Additions: Another form of bonus addition to your portfolio if you stay invested for more than 10 years

- Automated Portfolio Strategies: Use automated portfolio management to benefit from equity funds while you are busy at work.

- Tax-Savings U/S 80C & 10(10D): Investment of up to ₹ 1.5 lakhs to life insurance pension plans is tax-deductible under section 80C. Maturity value or partial withdrawals are exempt under Schedule II (Table S.No. 2) of the Income Tax Act 2025 (also called section 10(10D))

- High Liquidity: You can withdraw funds without breaking or surrendering your pension plan in need

Tax Benefits of Retirement Plans

Retirement plans in India offer significant tax advantages at every stage, from the contributions you make to the income you receive after retirement. Understanding these benefits can help you plan more efficiently and reduce your overall tax liability. Note that the Income Tax Act, 1961, has been replaced by the Income Tax Act, 2025, and several sections have been renumbered accordingly. The key provisions are outlined below.

- Tax Deduction on Contributions: Premiums paid towards life insurance pension plans are eligible for tax deduction of up to ₹1.5 lakh per year. This deduction is available under Section 123 of the Income Tax Act, 2025 (previously Section 80C of the Income Tax Act, 1961) and applies to contributions made towards pension plans, ULIPs, and other qualifying life insurance products. This is within the overall limit of ₹1.5 lakh applicable across all eligible instruments under this section.

- Additional Deduction for NPS Contributions: Over and above the ₹1.5 lakh limit, contributions to the National Pension Scheme (NPS) are eligible for an additional deduction of up to ₹50,000 per year under Section 124 of the Income Tax Act, 2025 (previously Section 80CCD(1B) of the Income Tax Act, 1961). This makes NPS one of the most tax-efficient retirement instruments available in India, with a combined maximum deduction potential of ₹2 lakh per year.

- Tax Treatment of Commuted Pension: A commuted pension refers to the lump sum amount received by a retiree instead of a portion of their periodic pension. Under Section 19(1), Table S.No. 9 of the Income Tax Act, 2025 (previously Section 10(10A) of the Income Tax Act, 1961), commuted pension received by government employees is fully exempt from tax. For non-government employees, a partial exemption applies depending on whether the employee also receives a gratuity. The remaining uncommuted pension is taxable as salary income as per the applicable tax slab.

- Tax Exemption on Life Insurance Pension Plan Payouts: Maturity proceeds and partial withdrawals from life insurance pension plans are exempt from tax under Schedule II, Table S.No. 2 of the Income Tax Act, 2025 (previously Section 10(10D) of the Income Tax Act, 1961), subject to applicable conditions. This makes life insurance-backed pension plans particularly attractive from a post-retirement tax planning perspective, as the income generated can be received largely tax-free.

- Tax Treatment of NPS Withdrawals: Upon maturity of the NPS account at age 60, up to 60% of the accumulated corpus can be withdrawn as a lump sum, which is fully exempt from tax. The remaining 40% must be used to purchase an annuity, and the annuity income received thereafter is taxable as per the individual's applicable income tax slab.

- Tax Treatment of EPF and PPF Withdrawals: Withdrawals from the Employees' Provident Fund (EPF) and Public Provident Fund (PPF) are fully exempt from tax, subject to the conditions specified under the Income Tax Act, 2025. PPF in particular follows an Exempt-Exempt-Exempt (EEE) tax structure, meaning contributions, interest earned, and maturity proceeds are all tax-free.

How to Choose the Best Retirement Investment Plan in India?

Choosing the right retirement and pension plan requires evaluating your financial goals, risk appetite, income stability, and retirement timeline to ensure long-term security. Here are the key factors to consider before making your decision:

- Start Early and Stay Consistent: The earlier you start investing, the more time your money has to multiply. As soon as you begin earning, start setting aside small amounts for retirement and increase your contributions steadily as your income grows. Even modest early contributions can outgrow much larger contributions made later, thanks to the power of compounding.

- Consider Equity Exposure: Even though equities are volatile compared to other asset classes, they tend to generate relatively better returns over the long term. Studies have consistently shown that equities outperform other assets over extended periods. Since retirement plans are long-term investment products, even a small allocation to equity funds has the potential to generate significant returns. Look for plans that offer equity options and allow you to adjust your allocation as you approach retirement.

- Prioritise Diversification: When saving for something as important as retirement, having disproportionately high exposure to a single asset class is inadvisable. Choose a plan that allows you to spread your investments across asset classes, equity, debt, and fixed income, so that your portfolio is resilient to market volatility while still generating meaningful returns.

- Check the Vesting Age: The vesting age is the age at which your pension plan matures and begins paying out. Choose a plan whose vesting age aligns with your planned retirement age. Some plans offer a vesting age as early as 40 years, while others extend up to 85 years, giving you flexibility to match the plan to your retirement timeline.

- Look for Automatic Portfolio Management: If your retirement plan includes equity exposure, automated portfolio management is an important feature to look for. This allows your money to benefit from market movements safely, even when you are not actively monitoring your investments. The best plans also offer automatic rebalancing that gradually reduces equity exposure as you near retirement, protecting your corpus from late-stage market volatility.

- Evaluate Bonus Additions: The best retirement and pension plans reward long-term investors with bonus additions such as loyalty additions and wealth booster benefits. These bonuses are typically unlocked after 5-10 years of continuous investment and can significantly accelerate the growth of your retirement corpus, particularly when you are invested in safer, lower-return portfolios.

- Assess Plan Expenses: Retirement and pension plans, particularly ULIPs, involve charges such as fund management fees and administrative costs. Since these expenses are typically deducted from your investment, choosing a plan with lower charges directly translates into a higher fund value at maturity. Always compare the total cost structure of a plan before committing.

- Check the Annuity Options: An annuity ensures that your corpus continues to generate income for as long as you live. Look for plans that offer a range of annuity options suited to your needs, including plans that guarantee payouts for a fixed number of years regardless of whether the policyholder survives. The right annuity structure can make a significant difference to your post-retirement financial stability.

- Review Surrender Charges and Borrowing Value: Retirement and pension plans build good cash value as they approach maturity. In an emergency, lower surrender charges allow you to recover the maximum amount from your investment. That said, surrendering a policy should be a last resort; most plans allow you to borrow against the policy at much lower interest rates, and the borrowing value is directly linked to the surrender value.

- Consider the Maximum Maturity Age: The maximum maturity age of a plan limits how long you can keep your funds invested in one place. Choose a plan with a high maximum maturity age so that you are not forced to make frequent reinvestment decisions close to or during retirement, which can expose your corpus to unnecessary risk and administrative burden.

How Much Do I Need to Retire?

Estimating your retirement corpus is the most crucial and personalised aspect of retirement planning. There is no single fixed number, as it depends on your age, desired lifestyle, existing savings, and several other financial factors. A commonly used rule of thumb is to target a corpus of 20–25 times your annual expenses at retirement, but arriving at the right figure for your situation requires a closer look at the following considerations.

- Your Current Age and Planned Retirement Age: The gap between your current age and your planned retirement age determines how long your money has to compound. The earlier you start, the less you need to invest each month to reach the same corpus. A 30-year-old saving for retirement at 60 has 30 years of compounding working in their favour, a significant advantage over someone starting at 45.

- Your Current and Future Living Expenses: Begin by estimating your current monthly expenses, including food, utilities, transportation, household costs, and discretionary spending. This figure forms the baseline for your retirement income requirement. As a practical benchmark, most financial planners recommend planning for 70–80% of your pre-retirement monthly income to maintain a comparable standard of living after retirement.

- The Impact of Inflation Over Time: Inflation is perhaps the most underestimated factor in retirement planning. At an annual inflation rate of 5%, expenses that cost ₹6 lakh today will cost approximately ₹14.38 lakh in 20 years. Your retirement corpus must be large enough not just to meet your expenses at the time of retirement, but to sustain rising costs throughout your retirement years. Always inflation-adjust your corpus target; failing to do so is one of the most common retirement planning mistakes.

- Life Expectancy and Retirement Duration: With improving healthcare and rising life expectancy in India, it is prudent to plan for a retirement that lasts 25-30 years or more. A corpus that comfortably covers 15 years of expenses may fall dangerously short if you live to 85 or 90. Plan conservatively because it is always better to have more than you need than to outlive your savings.

- Healthcare and Emergency Expenses: Medical expenses tend to rise significantly with age and are among the least predictable costs in retirement. A dedicated healthcare reserve, separate from your regular retirement corpus, is essential to avoid dipping into your primary savings for medical emergencies. Factor in the cost of health insurance premiums, routine medical care, and the possibility of long-term treatment or hospitalisation.

- Life Events and Major Milestones: Retirement does not mark the end of significant financial responsibilities. Children's higher education, weddings, or supporting ageing parents can all generate large, one-time expenses that must be factored into your retirement plan. Accounting for these milestones in advance ensures that your corpus is not unexpectedly depleted by events you could have planned for.

- Post-Retirement Lifestyle and Place of Residence: Your retirement lifestyle, whether you plan to travel, pursue hobbies, relocate to a quieter city, or start a small venture, has a direct bearing on how much you need. Living in a metro or Tier 1 city carries significantly higher costs than retiring in a smaller town. Be honest about the lifestyle you envision and build your corpus target accordingly.

- Existing Savings, Investments, and Other Income Sources: Your retirement corpus does not need to do all the heavy lifting alone. Rental income, dividends, part-time work, EPF, PPF, and NPS payouts can all supplement your monthly income and reduce the pressure on your primary corpus. Take stock of all existing assets and income streams before arriving at your final corpus target. The gap between what you have and what you need is what your retirement plan must bridge.

Documents Required to Buy a Retirement Plan

You need to have the following documents for buying a Retirement Plan:

Age proof document like a passport, a voting card, etc

Identity proof like Aadhaar, PAN Card, etc

Address proof like a driving license, a passport, a voting card, etc

Income proof like a bank statement, salary slip, etc

Retirement Planning Guide for Working Women

You are wearing multiple hats during a single day, and almost all of these hats are very important in your life. So, the best way for you to plan your retirement goal is as follows:

Keep it simple: Whether you can achieve your retirement goal or not depends majorly on one factor, and that is what portion of your income you are saving for retirement. If you have 20 to 30 years before your retirement age, saving 10 - 20% of your annual income towards this goal would take you a long way.

Use Diversified Portfolio: Retirement is one of those goals where your satisfaction with your fund pool is directly proportional to the diversity of your investments. This also helps you to maximise your retirement savings.

Automate Everything: The second important step is to delegate regular tasks so that you don’t have to spend time on them. Use the auto-debit facility to automate your investing contributions. If you invest in unit-linked plans, you can also use one of the automated portfolio management options to control your investment risk at all times.

Keep Your Money Invested: Retirement is not just a long-term goal; it’s a lifetime goal, as you will need to ensure that your retirement funds last at least your lifetime. So, for the best results, make sure your unused money is earning adequate interest at all times.

Use Life Insurance Plans: Life insurance pension plans are broadly available in two forms: traditional participating pension plans, which offer guaranteed returns and bonuses, and Unit-Linked Insurance Plans (ULIPs), which offer market-linked growth. Although both will give you the benefit of tax deductions under Section 123 (80C of the Income Tax Act 1961), ULIPs will also give you a tax-exempt partial withdrawal option under Schedule II (Table S.No. 2) (Former Section 10(10D)).

Retirement planning secures your future through early, diversified pension investments like NPS, ULIPs, and annuities that combat inflation and ensure a steady income. Start with 10-20% of income, leverage tax benefits, and progress through accumulation, preservation, and distribution phases for financial freedom.

Glossary

FAQs for Retirement Plans

There is no single best retirement plan. The right choice depends on your financial goals, risk appetite, and retirement timeline. As a general framework:

ULIPs (Unit-Linked Insurance Plans) are best suited for individuals with 20+ years to retirement who are comfortable with market-linked growth and want the dual benefit of insurance and investment.

Guaranteed annuity plans are ideal for those seeking assured, predictable income after retirement, regardless of market conditions.

NPS (National Pension Scheme) is well-suited for those who want a government-backed, flexible, and tax-efficient retirement vehicle with a mix of equity and debt exposure.

We, at Canara HSBC Life Insurance, offer retirement solutions across all three categories:

Legacy Builder: A ULIP-based retirement plan designed for long-term wealth creation while also building a financial legacy for your loved ones.

iSelect Guaranteed Future Plus: A guaranteed income plan that starts payouts from the 2nd policy year, ideal for those seeking early and assured returns.

Smart Guaranteed Pension: A traditional guaranteed pension plan that provides a steady, assured income stream post-retirement.

Pension4Life: An annuity plan designed to provide lifelong pension income, ensuring you never outlive your savings.

The answer depends on whether you are looking for a government-backed pension plan or a private pension plan:

Government pension plans such as NPS and EPF are regulated, low-cost, and offer tax benefits. NPS in particular offers flexibility in asset allocation and is open to both salaried and self-employed individuals. EPF is available to salaried employees and offers a fixed, government-declared rate of return.

Private pension plans, such as annuity plans offered by life insurance companies, provide guaranteed regular income after retirement and are not subject to market fluctuations. These are particularly suitable for those who want a predictable, lifelong income.

We at Canara HSBC Life Insurance offers strong options in both categories:

For guaranteed pension income, Pension4Life and Smart Guaranteed Pension provide assured, regular payouts that are not linked to market performance, ideal for those prioritising certainty over growth.

For market-linked pension accumulation, Legacy Builder offers equity participation through a ULIP structure, with the flexibility to build a larger corpus over the long term.

For those seeking early income, iSelect Guaranteed Future Plus starts guaranteed payouts from the 2nd policy year itself.

These terms are often used interchangeably, but they are not the same:

A retirement plan is a broader term that refers to any financial strategy or instrument designed to help you build a corpus for life after employment. This includes NPS, EPF, PPF, ULIPs, mutual funds, and fixed deposits, essentially any vehicle that helps accumulate wealth for retirement.

A pension plan is a specific type of retirement product that provides regular income after retirement, typically through an annuity mechanism. The focus is not just on accumulation but on the distribution of income throughout your retirement years.

Ideally, you should start investing in a retirement plan in your 20s or early 30s to maximise the benefit of compounding. The difference that a few years can make is significant:

Starting at age 25 with a monthly contribution of ₹5,000 at an assumed return of 8% p.a. can grow to approximately ₹1.15 crore by age 60.

Starting at age 35 with the same contribution and return assumption, yields only approximately ₹47.87 lakh by age 60, less than half.

That said, starting at 40 is still far better than not starting at all. Every year of delay increases the contribution required to reach the same corpus. The best time to start was yesterday; the next best time is today.

A commonly used rule of thumb is to target a retirement corpus of 20–25 times your annual post-retirement expenses. For example:

If you estimate needing ₹6 lakh per year after retirement, aim for a corpus of ₹1.2 crore to ₹1.5 crore.

However, this figure must be adjusted for inflation. At an annual inflation rate of 5%, ₹6 lakh today will cost approximately ₹14.38 lakh in 20 years. Your corpus target must account for this rise in expenses over your entire retirement period.

Other factors that influence your corpus requirement include your expected retirement age, life expectancy, healthcare costs, lifestyle goals, and existing savings. Use the retirement calculator on this page to factor in all these variables and arrive at a personalised corpus estimate for your situation.

Self-employed individuals do not have access to employer-backed retirement benefits such as EPF or gratuity, making personal retirement planning essential. The good news is that several instruments are well-suited to their needs:

NPS is open to individuals aged 18 to 70 and allows flexible contributions with no fixed monthly commitment, ideal for irregular income. It also offers strong tax benefits under Section 123 and Section 124 of the Income Tax Act, 2025.

PPF is a reliable, government-backed option with fixed returns and an EEE tax structure, allowing flexible contributions up to ₹1.5 lakh annually.

For market-linked growth with life cover, Legacy Builder suits long-term investors, offering equity exposure, top-up flexibility, and loyalty additions.

For those nearing retirement, Smart Guaranteed Pension and Pension4Life provide assured, regular income independent of market conditions.

For earlier income needs, iSelect Guaranteed Future Plus starts payouts from the 2nd policy year.

The key is to treat retirement savings as a fixed monthly commitment. Starting early and investing consistently, even in smaller amounts, delivers better outcomes than irregular, large contributions later.

The treatment of your retirement fund in the event of death before withdrawal depends on the type of plan:

Life insurance pension plans (ULIPs and traditional plans): The nominee receives the death benefit, typically the higher of the fund value or sum assured, ensuring financial protection.

NPS: The entire accumulated corpus is paid to the nominee or legal heir as a lump sum, with no annuity requirement. This payout is tax-free.

PPF: The full balance is paid to the nominee upon death, regardless of the lock-in period. There is no need to wait for maturity.

EPF: The nominee receives the full EPF balance along with any applicable insurance benefit under the EDLI scheme (up to ₹7 lakh).

Keeping nomination details updated across all investments is essential to ensure smooth and timely transfer of funds, avoiding legal delays for the family.

Life is unpredictable, and so it is important to prepare for all eventualities. If you regularly save a substantial amount of your income for retirement, the corpus may expand to a comfortable level before retirement. In case you become disabled and are unable to contribute to the retirement plans, most plans will continue to multiply your savings. The amount already accumulated will continue to grow, and besides the existing plans, you can also choose to invest in pension schemes specifically designed for people with disability.

Investment in ULIPs like Promise4Growth Plus plan qualifies for tax deductions under Section 123 (former 80C) of the income tax law. The maturity benefits of ULIPs are also tax-exempt under Schedule II (Table S.No. 2) of the Income Tax Act 2025 (former section 10(10D) of the Income Tax Act, 1961). However, if the premium paid during the policy term is more than 10% of the sum assured, the maturity proceeds will be taxable.

The concept of early retirement is catching up fast in India, but there are no specified ages for early retirement. While in some Western countries the age between 35 and 45 is considered favourable for early retirement, in India, the ideal age is 45-50 years. With the right planning and investments, it is not very difficult to retire early.

At the age of 35-40, people generally have several responsibilities such as children’s education and various EMIs. It is difficult to spare a substantial amount of income for retirement. Depending upon the needs of the household and the lifestyle, one should aim to save around 40-50% of his/her income. Around 10% of the income should exclusively be allocated for retirement planning. Here are some tips to choose the best retirement plan.

Focus on your needs: It is easier to formulate a strategy when the goal is clear. Estimate the amount required to sustain your life. Take inflation into account and zero in on the targeted corpus.

Research thoroughly: Conduct thorough research before investing in any financial product. Read the terms and conditions properly and try to understand how an investment product fits your needs.

Consider different products: The market is awash with all kinds of investment products. Do not follow conventional advice, as the needs of every person are different. Take into consideration all the suitable products, conduct an objective analysis, and then invest.

Owning a house is a cherished dream for many. There are several ways to save for a new house, but in urgent cases, people may be tempted to withdraw from their retirement fund. There are various financial products for retirement planning, and all have different withdrawal rules. In the case of the National Pension Scheme, partial withdrawals for special purposes like buying a house are allowed only thrice during the policy tenure. However, to avail the withdrawal facility, you should be an NPS investor for at least 10 years, and you are permitted to withdraw only 25% of your contribution. If you have a PPF account, you can withdraw 50% of the accumulated amount, but only after staying invested for at least 6 years.

The quantum of monthly savings depends on the specific needs of the buyer. Financial advisors, however, suggest people save around 15% of their monthly income for retirement.

Retirement plans such as NPS have a very low entry threshold. It is also open to all, and anyone can open an NPS account and start saving.

The choice between paying off a student loan or starting a retirement account is not a difficult one. Starting early for retirement planning has its own advantages, but extending the student loan will increase the interest burden. You will have to find a balance between the two. Try to pay off the student loan as soon as possible, but do not hold back on investing in a retirement account.

Most people nominate their spouse to receive retirement benefits in their absence. But a spouse is not automatically entitled to be the beneficiary of a retirement account owned by the other spouse.

Gold is a safe investment asset, and investors often flock to the yellow metal to stabilise their portfolios. Holding a small quantity of gold can be considered, as the intrinsic value of gold remains intact. You can also choose to have an exposure to gold through ULIPs. ULIP funds invest in a variety of asset classes, and some fund options also have a small exposure to gold. You can choose fund options with gold to have a small and indirect investment in gold

While there are no explicit rules barring the use of a retirement account to finance real estate, it may not be advisable to do so. For instance, you are allowed to avail a loan from the PPF account from the third financial year. The loan can be used to finance real estate, but it would defeat the purpose of having a dedicated retirement account.

While there are no explicit rules barring the use of a retirement account to finance real estate, it may not be advisable to do so. For instance, you are allowed to avail a loan from the PPF account from the third financial year. The loan can be used to finance real estate, but it would defeat the purpose of having a dedicated retirement account.

The government has allowed all central government pensioners to open a joint account with their spouses

Vesting date or age signifies when your pension plan’s accumulation phase is over, and the distribution phase can begin. For example, in a deferred annuity plan, you may have a vesting date that is 10 to 30 years away, depending on your age at entry. You will continue to invest or stay invested till the vesting date. After the vesting date or age, you can start receiving the pension or withdraw the money from the plan.

The steps may differ from plan to plan. However, you can buy the online retirement plans following the steps below:

Retirement Calculator: Use a retirement calculator to estimate your corpus need and expected monthly investment amount to achieve it

Choose Plan: Select the online retirement plan you want to start investing in

Contact Information: Fill in the personal details, including the contact information. Make sure to put the correct e-mail ID that you can access, since all future communication about the policy will take place via e-mail.

Define Your Investment: Select the goal, investment term, investment frequency, and amount you want to invest (based on the calculator estimate)

Select Fund Allocation: Online retirement plans give you the option to invest in multiple assets, including equity funds. You can select the ratio in which your premium will be allocated to these funds as per your risk appetite. Then select one of the portfolio rebalancing strategies.

Select Withdrawal Plan: You can withdraw money based on a set milestone or systematically from the plan after the lock-in period. Select the options for withdrawal as per your plan.

Review Plan & Investment Details & Complete the Application Form

You can pay the premium amount before or after completing the application form to start investing.

The best time to plan your retirement is when you are planning your career. However, this may not be the time when you really start investing money for your retirement. You must start investing in your retirement plan as soon as you start earning.

Retirement is the only financial goal you cannot repair with other means of funding, like a loan. Thus, developing the habit of investing with every income you have is the best way to have a comfortable retirement.

Insurance allows your family, especially your dependent spouse, to continue living without financial worries if anything happens to you. Also, insurance may help you save enough for retirement in case of permanent disabilities. Additionally, life insurance retirement plans allow you to build a good retirement corpus with bonus additions.

Yes, you can change the nominee of the policy anytime you need. If you are using an Electronic Insurance Account (EIA) to manage your policies, you can change the nominees anytime from this account. Otherwise, you can contact the customer care to update the nominations on your policy

You can opt for auto-debit of the premiums from your savings account. You can also pay the premiums online using your debit card, credit card, or a payment wallet.

You can get a ₹1 Core pension plan using the online retirement calculator. The calculator will assess your eligibility and provide you with the probable monthly or annual investment to achieve the goal. If the amount seems feasible, you can complete the purchase online or set an appointment for a qualified advisor to help you in the process.

A pension is a type of fund created to assist you after retirement. Here, you are required to invest a certain sum regularly or in a lump sum during your working years. You then receive a regular stream of income from the fund you created to meet your expenses after retirement.

An annuity is a type of contract between you and the insurance company. In the contract, you agree to make payments, either in a lump sum or regularly, to the insurance company. In return, you receive regular payments from the insurance company for a specific term. This makes policyholders financially secure.

Yes, you can invest in multiple pension plans. Though there are limits prescribed to the amount you can invest yearly in the chosen pension schemes, if you are looking to get relief from taxes.

If you surrender your pension plan before maturity, the surrender value gets added to your taxable income. This income is subject to a charge under the appropriate tax bracket. Also, any tax exemptions you may have received, and the outstanding premiums, need to be paid back by you.

The New Pension Scheme or NPS is a government-created pension plan aimed at protecting the financial future of individuals once they retire. Also called the National Pension Scheme it is regulated by the Pension Fund Regulatory Development Authority of India (PFRDA). People falling between the age bracket of 18 and 60 years can invest in NPS.

New Pension Scheme offers varied investment opportunities, tax benefits, and is cost-effective as well.

There is no one ‘best’ retirement plan. Every investor looks for something different in a retirement plan than the other. Insurance companies offer a variety of retirement plans with different features. You should choose the plan that best suits your lifestyle, risk factors, etc

In a participating pension plan, you are entitled to receive the profits earned by the insurance companies as a bonus or dividend. Non-participating pension plans, on the other hand, do not involve bonuses as the profits are not shared with you in this plan. Both plans, however, provide guaranteed life cover.

You can choose from a range of options to pay your retirement plan’s premiums. Some of the ways are Cheque deposits, net banking, credit/debit cards, e-wallets, electronic clearing service (ECS) wallets, etc.

3 Signs of Secure Retirement Planning - Plan a Stable Future

31 July '26

1102 Views

6 minute read

Understand the key signs of secure retirement planning. Learn how savings, smart investments, and financial discipline help build a stable retirement.

Read More

Retirement Plan

What Post-Retirement Taxes Should You Be Aware of in India?

31 July '26

5909 Views

7 minute read

Learn about three key taxes retirees should know, tax on pension income, interest from savings, and gains from withdrawals -plus tips to plan tax-efficient retirement income.

Read More

Retirement Plan

How to Withdraw Pension Contribution Online? Step-by-Step Guide

31 July '26

895 Views

11 minute read

PF withdrawal online - Know the eligibility criteria for withdrawing EPF online and the process of pension withdrawal online.

Read More

Retirement Plan

EPF Tax Rules: Tax on Provident Fund Withdrawals Explained

31 July '26

1245 Views

7 minute read

Understand EPF tax rules for provident fund withdrawals. Check when EPF withdrawals are taxable, exemptions, and how tenure affects tax liability.

Read More

Retirement Plan

What Are the Best Investment Options for Indian Retirees?

30 July '26

897 Views

8 minute read

Explore safe and income-focused investment options for retirees, including SCSS, PMVVY, annuities, mutual funds and deposits, with guidance on risk, returns and taxation.

Read More

Retirement Plan

How to Avoid Running Out of Money After Retirement?

30 July '26

904 Views

7 minute read

Learn how to avoid running out of money during retirement by planning expenses, managing savings wisely, preparing for medical costs and ensuring a steady income for life.

Read More

Retirement Plan

Best Insurance Plans to Consider After Retirement in India

30 July '26

892 Views

7 minute read

Understand insurance Plans after retirement. Compare plans that help manage healthcare costs, protect savings, and support financial stability.

Read More

Retirement Plan

5 Reasons to Use ULIPs for Building a Retirement Corpus

30 July '26

8508 Views

11 minute read

Learn five strong reasons why ULIPs are suitable for building a retirement corpus, offering long-term growth, flexibility, disciplined investing and life cover.

Read More

Retirement Plan

When Should You Buy an Annuity Plan in India?

30 July '26

1050 Views

9 minute read

Learn the ideal age to buy an annuity plan, factors that influence timing such as retirement goals, income needs, interest rates, and how early purchase can impact payouts.

Read More

Retirement Plan

Popular Searches

- Retirement Calculator

- Best Retirement Plan

- Senior Citizen Card

- Saral Pension Plan

- NPS Withdrawal

- Pension4Life Plan

- Retirement Planning

- 5 Retirement Tips

- National Pension Scheme

- NPS Pension Calculator

- Types of Pension Plan

- Guaranteed Pension Plan

- Is Pension Taxable

- How to Check Old Age Pension Status

- Benefits of Pension Plan

- How GST Applies to Pension Plan?

- Tax Planning for Retirement

- Types of Retirement Plans

- Guaranteed Pension Plans

- Retirement Income Plans