- Gross Total Income: Gross Total Income is the total income earned in a year before claiming any deductions or exemptions

- Taxable Income: Taxable Income is the income left after all eligible deductions are reduced from gross income

- Standard Deduction: Standard Deduction is a flat reduction allowed from salary income without submitting any expense proof

- Health and Education Cess: Health and Education Cess is an additional 4% charge on income tax to fund public health and education

- Tax Deduction: Tax Deduction reduces taxable income by allowing certain expenses or investments under the Income Tax Act

Browse article by category

0

1

1.

What are Tax-Saving Plans?

0

2

2.

Save Taxes While Building Long-Term Wealth

0

3

3.

Why Should You Invest in Tax-Saving Plans?

0

4

4.

How to Save Tax with Saving Plans?

0

5

5.

Income Tax Investments Under Section 80C

0

6

6.

Tax Savings - Top Selling Plans

0

7

7.

Income Tax Investments Under Section 80D

0

8

8.

Income Tax Saving Tips

0

9

9.

What is the Maximum Amount You Can Save in Taxes?

10

10.

Without Tax Saving Investments

11

11.

With Tax Saving Investments

12

12.

Glossary

13

13.

Tax Saving Investments – FAQs

14

14.

Recent Blogs

Paying taxes is a part of earning, but smart planning can help you keep more of what you earn. By understanding how different tax-saving sections work, you can legally reduce your tax outgo while building long-term financial security through well-chosen investments.

Key Takeaways

|

What are Tax-Saving Plans?

Tax-saving plans are financial products where an investor can claim tex benefits on eligible investments under the Income Tax Act, 1961. Under the Sections 80C and 80D of the Indian Income Tax Act, an individual can claim a deduction on the premium payment made or the investment done. These investments can consist of funds such as Equity Linked Saving Scheme, Life Insurance Plans, Public Provident Funds, Fixed Deposits, and Bonds. To ease the income tax burden on taxpayers, Indian tax laws provide several tax-saving avenues, with eligible investments and deductions being among the most commonly used options.

You must file your annual income tax return to claim the tax deductions. Most tax-saving investments will reduce your gross total income. Individuals, HUF and NRI taxpayers can use tax-saving investment plans eligible under section 80C to save direct income tax.

Save Taxes While Building Long-Term Wealth

Enter OTP

An OTP has been sent to your mobile number

Didn’t receive OTP?

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder as on

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Sorry ! No records Found

Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Why Should You Invest in Tax-Saving Plans?

On the income that is earned, we are required to pay taxes if this income exceeds a prescribed threshold limit. Tax planning can help reduce the burden of taxes that fall on an individual and maximise their savings. There are many financial instruments that help in saving taxes. A good investment provides tax savings, safety of investments, returns and liquidity. An ideal financial instrument will help you save taxes at the same time as it reaps benefits in the form of decent returns and the flexibility to withdraw funds. By investing in tax-saving plans, individuals also inculcate a habit of saving over time.

How to Save Tax with Saving Plans?

There are various other provisions in the Income Tax Act 1961 as well, which provide for more deductions.

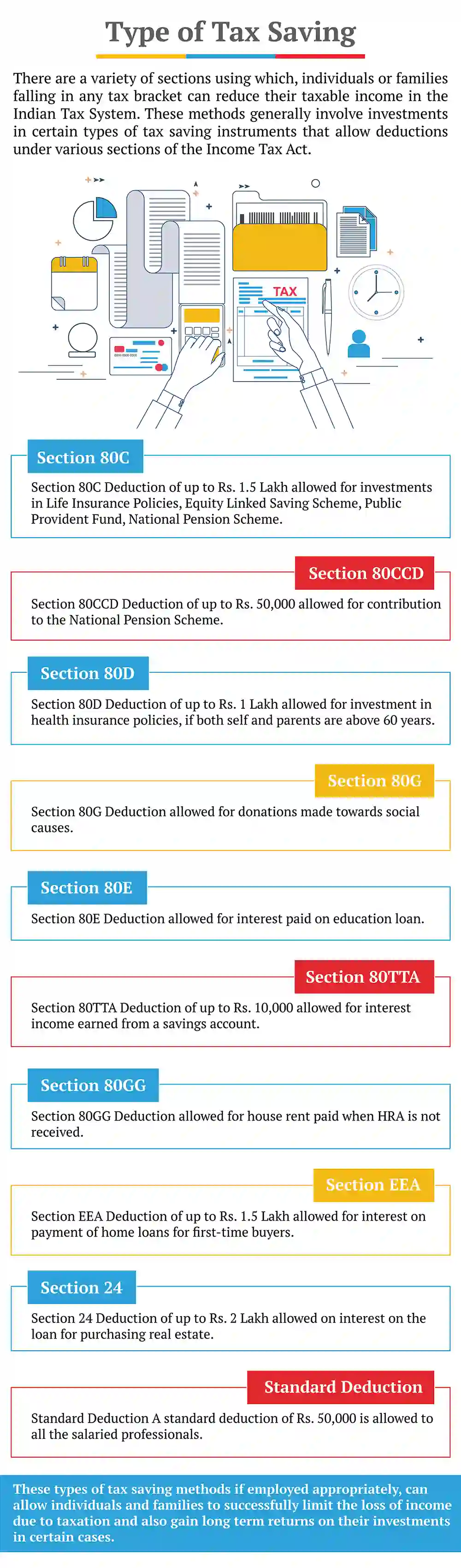

Section 80C, 80CCC and 80CCD(1) allow an aggregate deduction upto ₹ 1.5 lakh per financial year on eligible investments. These sections cover a wide variety of investment options, ranging from a simple life insurance plan to a hybrid ULIP among others.

Similarly, under Section 80E, taxpayers can claim a deduction for the interest paid on an education loan for higher education.

Section 80G provides for tax deduction on the amounts paid by you as donations to charities, social organisations, relief funds etc.

You can plan to save taxes using tax saving financial instruments with the following steps:

- Avoid last-minute decisions and plan your tax savings at the start of the financial year.

- The earlier you start, the more time you allow your tax-saving investments to grow and help fulfil your goals.

- Decide on the goal that you want to achieve through your investment.

- Make a note of your current expenses that are eligible for tax deductions. The payments applicable under section 80C include

- Tuition fees for up to two children

- EPF contribution

- Principal repayment of the home loan

- Premium payment for life insurance

- Investments in PPF, ELSS, Sukanya Samriddhi Yojana, NPS (80C/80CCD(1))

After assessing the current deductions, take into account the risks involved and the risks that you can take.

After considering both the goal and the risk you can take, choose the investment. For example, for long-term retirement savings with tax benefits, the National Pension Scheme (NPS) or the Public Provident Fund (PPF) may be ideal.

Did You Know?

The government kept interest rates on key small savings schemes unchanged for the March 2026 quarter to support stable, long-term tax-saving investments

Source: Economic Times

Income Tax Investments Under Section 80C

For those wondering what is Section 80C-, it is a provision under the Income Tax Act 1961 that allows a tax deduction of up to ₹ 1.5 lakh on eligible investments.

Most of the investments such as NPS, PPF, Sukanya Samriddhi Yojana, Equity Linked Savings Scheme, (ELSS), and Unit Linked Insurance Plans (ULIP) are covered under section 80C.

| INVESTMENTS | RETURNS | LOCK-IN PERIOD |

|---|---|---|

| ELSS Mutual Funds | Market-linked; varies with equity performance | 3 years |

| National Pension Scheme (NPS) | 8-10% long-term; depends on equity/debt allocation | Till Retirement |

| Unit Linked Insurance Plan (ULIP) | Market-linked; depends on fund choice | 5 years |

| Public Provident Fund (PPF) | 7.1% p.a. (tax‑free) | 15 years |

| Sukanya Samriddhi Yojana (SSY) | 8.2% p.a. (tax‑free) | 21 years |

| National Savings Certificate (NSC) | 7.7% p.a. (taxable) | 5 years |

| Senior Citizen Saving Scheme (SCSS) | 8.2% p.a. (taxable) | 5 years |

| Bank FDs | 7.5% p.a. (taxable) | 5 years |

| Insurance | Guaranteed benefits + Bonus | Varies by policy |

| Pension Plans | 6 - 8% p.a. (depending on the type of plan) | Varies by policy |

Note:

Returns on market-linked instruments such as ELSS, NPS, and ULIPs fluctuate based on underlying assets.

PPF, SSY, and NSC are tax-free saving schemes, offering EEE (Exempt-Exempt-Exempt) status, i.e., principal, interest, and maturity amount are tax-free.

Interest from Bank FDs is taxable; senior citizens can use Section 80TTB to claim a deduction of up to ₹50,000 on interest income.

All instruments listed can help you reduce taxable income and are considered tax-saving investments under the Section 80C deduction list.

Equity-Linked Saving Scheme (ELSS)An ELSS is a tax-saving, open-ended mutual fund scheme that invests at least 80% of its assets in equities. It is one of the most effective tax-saving investments for investors with a high-risk appetite. The main incentive in an ELSS fund is the possibility of a high long-term returns due to heavy investment in equity. Contributions to ELSS are eligible for deductions under Section 80C, up to ₹1.5 lakh per year. The actual tax savings depend on your income tax slab; for example, an individual in the highest tax slab could save up to ₹46,800 in taxes on a ₹1.5 lakh investment. ELSS funds have a mandatory lock-in period of 3 years, the shortest among tax-saving instruments under 80C, which allows both liquidity and tax efficiency. |

National Pension Scheme (NPS)

|

Unit-Linked Insurance Plan (ULIP)ULIPs are a combination of insurance and investment. This means that the premium paid towards the policy goes partly towards life insurance and the rest is invested in diversified funds. You can invest in equity, debt, or money market funds, as per your risk appetite. These are one of the best tax-saving investments allowing you the flexibility of: Premiums paid towards ULIPs are eligible for tax deduction under Section 80C, subject to an overall limit of ₹1.5 lakh, provided the policy conditions are met. ULIPs have a mandatory lock-in period of five years. Maturity proceeds and death benefits may be tax-exempt under Section 10(10D), subject to applicable premium and policy conditions as per current income tax rules. |

Public Provident Fund (PPF)PPF is the best tax-saving investment with a sovereign guarantee on returns. You can borrow from the fund balance starting from the third financial year of the account. After five continuous financial years of investment, you also have the option of partial withdrawals in accordance with eligibility rules. The tax savings under PPF extend to both the returns and the interest earned on deposits. PPF falls under the Exempt-Exempt-Exempt category. Interest and maturity value are also tax-free. Thus, PPF accounts are one of the best tax-saving plans, as the account also has no maximum age for maturity. |

Sukanya Samriddhi YojanaSukanya Samriddhi Yojana is a small savings scheme, backed and promoted by the Government of India. As a parent or legal guardian of a girl child below the age of 10, you can open a Suknya Sammriddhi Account in a post office or authorised bank in the name of the child. The scheme aims to encourage parents to save for the education and future needs of a girl child from an early age. It also offers tax benefits in the form of the Exempt-Exempt-Exempt (EEE) category. The investments made into the scheme are eligible for deductions under Section 80C up to Rs 1.5 lakhs. The interest earned and maturity values are also tax-free under prevailing income tax laws. |

National Savings Certificate (NSC)National Savings Certificate (NSC) is a fixed-income investment scheme backed by the Government. of India. It is suitable for investors looking to invest a lump sum amount. with assured returns, as the interest rate is fixed at the time of investment and remains unchanged until maturity, does not have a maximum investment limit. Investments made in NSC qualify for tax deduction under Section 80C up to ₹1.5 lakh in a financial year. The interest earned on NSC is taxable; however, the interest accrued for the first four years is deemed to be reinvested and is also eligible for deduction under Section 80C. The interest earned in the fifth year is taxable. |

Senior Citizen Saving SchemeSenior Citizens Savings Scheme (SCSS) is another government-backed savings instrument for Indian citizens above the age of 60 years, and for eligible retirees aged 55-60 years, subject to prescribed conditions. Aimed at providing a reliable source of regular income to senior citizens after retirement, the scheme offers quarterly interest payments. The investments made towards SCSS can be claimed as a deduction under section 80C of the Income Tax Act. The Interest under SCSS is taxable and bank/post offices will deduct tax @10% under section 194A if annual interest exceeds ₹ 50,000. However, where the person has income below the minimum threshold limit and provides form 15H, interest can be received without a TDS deduction. |

5-Year Bank Fixed DepositBanks and post-office provide a 5-year tax-saving fixed deposit. As per Section 194A of the Income Tax Act of 1961, the interest earned on these FDs is taxable if it crosses ₹ 5,000 (₹ 10,000 for senior citizens) mark. Often, tax is deducted at the source for the same. However, senior citizens can use these FDs to create tax-free pension income of up to Rs 6.5 lakhs a year. |

Life Insurance PolicyLife insurance plans are perhaps the best tax-saving investment options with guaranteed benefits. At the same time, the life cover enhances the financial safety of the family while you are still earning money. The premium you pay for a life insurance plan is eligible for a deduction under Section 80C, up to Rs 1.5 lakh. The amount received on maturity or the death of the policyholder is also exempt from tax in the hands of the beneficiaries. |

Pension PlansPension plans are annuity-based plans which help senior citizens and retiring investors invest their retirement corpus for a reliable income stream. Such plans act as a financial safeguard for individuals post-retirement. Since investment into pension plans also qualifies for tax deduction these are also the best tax-saving investments for retired investors or those close to retirement. Pension plans from life insurers also provide pension security for your spouse with a life cover. Alternatively, you can also purchase a joint life pension plan with guaranteed pension income for life. |

Tax Savings - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Family Shield: Enhanced Protection

iSelect Smart360 Term Plan

- 3 Plan options

- Life cover till 99 years

- Steady income benefit

- Block your premium at inception

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Start Young, Pay Less, Stay Secured

Young Term Plan

- Life cover till 99 years

- Coverage for spouse

- Block your premium rate

- Covers 40 critical illness

Income Tax Investments Under Section 80D

| Section | Deduction Limit | Amount in Rs |

|---|---|---|

| 80D | When health insurance is for insured below 60 years | 25,000 |

| When health insurance is for insured 60 years or above | 50,000 | |

| Total for self and family and senior parents | 75,000 | |

| 80DD | When the taxpayer or dependent suffers from at least severity of 40% disability | 75,000 |

| When the taxpayer or dependent suffers from at least severity of 80% disability | 1,25,000 | |

| 80DBD | Patients below 60 years of age | 40,000 |

| Patients of age 60 years and above | 1,00,000 |

Health InsuranceHealth insurance is a critical component of a sound financial portfolio, as medical emergencies can significantly impact financial stability. But the benefits of a health insurance policy are not just limited to this purpose. Under Section 80D of the Income Tax Act, 1961, a deduction of up to Rs 25,000 is allowed in a year in terms of the premium paid towards a health insurance policy of self, spouse, children. An additional deduction of up to ₹25,000 is available for premiums paid for parents, which increases to ₹50,000 if the insured parents are senior citizens. Where both the taxpayer and parents are senior citizens, the maximum deduction can go up to ₹1,00,000 in a financial year. |

Deduction on Preventive Healthcare Check-upsPreventive healthcare check-ups refer to the pre-emptive measures taken to keep diseases and ailments at bay. Deduction up to ₹ 5,000 is allowed for preventive health check-ups for self, spouse, children or parents which is a part of the overall deduction one can claim under Section 80D. |

Deductions on Health Insurance Premium Paid for ParentsAn individual can claim a deduction of up to ₹ 25,000 for insurance of self, spouse, and dependent children. Additionally, a deduction is allowed on the insurance of your parents as well. If parents are below 60 years of age, the deduction is capped at ₹ 25,000, whereas in case of parents aged 60 or more, the cap is at ₹ 50,000. |

Deduction for Rehabilitation of Handicapped Dependent RelativeSection 80DD covers expenditure on medical treatment, rehabilitation, and training of disabled dependents. The section provides for a deduction up to ₹ 75,000 for a disability that is classified in 40%-80% range. If such dependant is a person with severe disability, deduction amount can be claimed up to ₹ 125,000. |

Deduction for Medical Expenditure on Self or Dependent Relative for the Treatment of Specified Diseases under Section 80DDBThis is to be seen separately for each case. In case of individuals and HUFs below age 60, the deduction is capped at ₹ 40,000. The amount being the expenses incurred towards the treatment of specified medical diseases or ailments for the individual or any of their dependents. For a HUF, such a deduction is available with respect to medical expenses incurred towards these prescribed ailments for any of the HUF members. In case of senior citizens and super senior citizens, deduction of up to ₹ 1 lakh can be claimed. In case of reimbursement by an insurer or employer reduces the deduction claim. Proper prescriptions and proofs should be furnished. |

Income Tax Saving Tips

The goal of tax planning is to maximise tax savings. Since there are multiple investment options for the same tax-saving provision, it is important to build the investment portfolio in a way that makes use of all the available tax exemptions.

Income Tax Saving Investments for Young Unmarried Tax-PayersAs a youngster in your 20s and early 30s, and unmarried you can make great use of aggressive tax-saving schemes to grow your wealth. Additionally, you need to focus on building a good financial safety net for your family and parents. There are several tax-saving investment plans for you in this category:

|

Income Tax Saving Investments for Single-Income CouplesIf you are married, have a child and only one of the partners is earning, your investment strategy should match your financial goals and family needs. Recommended options include:

|

Income Tax-Saving Options for Double-Income CouplesIf you are married and both you and your spouse earn, you can jointly claim deductions with the right investments:

|

Tax-Saving Investment Options for Senior CitizensNearing retirement, we must shift our focus towards ensuring financial stability and especially towards maximizing savings. Consider these tax-saving investments:

|

Tax Saving Options for Family Business OwnersFamily-run businesses and enterprises are liable to pay income tax on their revenues generated, which can be a considerable sum. They must therefore take benefit of tax deductions and exemptions available to minimise their tax liability as a company:

|

What is the Maximum Amount You Can Save in Taxes?

The Income Tax Act provides multiple tax-saving sections that allow you to invest in tax-saving options and reduce tax liability. Popular sections to find your tax-saving investments are Section 80C, 80D, 80CCD (1B), and 24 (b).

Each section has a prescribed limit, and the total tax saving depends on the amount you invest and your eligibility.

The following table lists the limits under these sections for investments and expenses that a taxpayer can voluntarily incur:

| Deductions | Max Amount (Rs.) |

|---|---|

| Standard deduction | 50,000 |

| Section 80C* | 150,000 |

| Section 80D (for insured <60 years) | 25,000 |

| Section 80CCD(1B) NPS | 50,000 |

| ction 24(b) – Home loan interest (self-occupied) | 200,000 |

| Total | 4,75,000 |

*The total deduction amount in aggregate under sections 80C, 80CCC and 80CCD (1) cannot exceed Rs 1.5 lakhs

Shubham is a Digital Manager in a reputed firm and has a gross income of Rs 10 lakhs for FY 2024-25 (AY 2025-26). He has also reported TDS payments of ₹55,000.

- Rs 45,500 + cess payable as income tax if he uses minimum tax deduction investments

- Rs 55,000 receivable as an income tax refund if he utilises maximum tax-saving investments

This serves as a simple 80C deduction example, showing how eligible investments reduce taxable income and overall tax liability.

Without Tax Saving Investments

| Without Tax Saving Investments | ||

|---|---|---|

| Gross Total Income (after TDS & HRA deduction) | 100000 | |

| Less: Standard Deduction | -50,000 | |

| Less: Tax Saving Investments U/S 80C | 0 | |

| Less: Tax Saving Investments U/S 80CCD(1B) | 0 | |

| Less: Tax Saving Investments U/S 80D (for family & parents) | 0 | |

| Less: Tax Saving Investments U/S 80TTA | -10,000 | |

| Less: Tax Saving Investments U/S Sec 24B | 0 | |

| Net Taxable Income | 9,40,000 | |

| Tax Liability | ||

| Add: For income up to Rs 2.5 lakhs | 0 | |

| Add: For income above Rs 2.5 lakhs but below 5 lakhs | 12,500 | |

| Add: For income above Rs 5 lakhs | 88,000 | |

| Total Tax on Income (cess extra) | 1,00,500 | |

| Less: Rebate under section 87A (for taxable income below 5 lakhs) | 0 | |

| Less: TDS deductions | 55,000 | |

| Tax Payable / Refund | 45,500 | |

Note: Health and Education Cess of 4% is applicable on the total tax payable.

With Tax Saving Investments

| With Tax Saving Investments | ||

|---|---|---|

| Gross Total Income (after TDS & HRA deduction) | 10,00,000 | |

| Less: Standard Deduction | -50,000 | |

| Less: Tax Saving Investments U/S 80C | -1,50,000 | |

| Less: Tax Saving Investments U/S 80CCD(1B) | -50,0000 | |

| Less: Tax Saving Investments U/S 80D (for family & parents) | -75,000 | |

| Less: Tax Saving Investments U/S 80TTA | -10,000 | |

| Less: Tax Saving Investments U/S Sec 24B | -2,00,000 | |

| Net Taxable Income | 4,65,000 | |

| Tax Liability | ||

| Add: For income up to Rs 2.5 lakhs | 0 | |

| Add: For income above Rs 2.5 lakhs but below 5 lakhs | 10,750 | |

| Add: For income above Rs 5 lakhs | 88,000 | |

| Total Tax on Income (cess extra) | 10,750 | |

| Less: Rebate under section 87A (for taxable income below 5 lakhs) | -10,750 | |

| Less: TDS deductions | -55,000 | |

| Refund Receivable | -55,000 | |

Planning your taxes in advance can make a meaningful difference to both your savings and long-term financial stability. By understanding how different deductions and exemptions work, you can reduce your tax liability while aligning your investments with future goals. Choosing the right mix of tax-saving options and tax-free investments in India allows you to optimise returns, improve cash flow, and approach tax planning with greater clarity and confidence.

Glossary

Tax Saving Investments – FAQs

First of all, your gross total income is taken into account and all applicable deductions/exemptions are deducted out of it, the resultant amount is the net income, upon which the Income Tax is calculated, on the basis of income tax slabs that are announced each year in the Union Budget.

The amount of tax you can save depends on your investments and financial profile. Section 80C allows deductions up to ₹1.5 lakh, potentially saving up to ₹46,800* per year, depending on your tax slab. Other deductions, like health insurance premiums and loan interest, also reduce your tax liability.

*Calculated at the highest tax slab of 31.2% (including 4% cess) for an individual with taxable income up to ₹50 lakh on life insurance premiums of ₹1.5 lakh.

The best tax-saving investment would be an investment which offers the flexibility of investments, withdrawals and asset allocation as per your risk appetite. ULIPs, Guaranteed Saving Plans, ELSS, PPF, etc, are some of the best tax-saving options in India you can invest in.

If the interest earned or maturity value of your investment is tax-free you may not need to pay a tax on your investment. However, many tax-saving investments under section 80C do not offer tax exemption on accrued interest or maturity. Thus, you can choose the tax saving investments where accrued interest, partial withdrawals and maturity are tax-free.

You can choose investments that are tax-exempt: not an exhaustive list, but includes Equity Linked Saving Scheme (ELSS), Public Provident Fund (PPF), life insurance plans, Unit Linked Insurance Plans (ULIPs), Sukanya Samriddhi Yojana, Senior Citizens Savings Scheme (SCSS), National Pension Scheme (NPS), Bank Fixed Deposits.

You can claim almost any tax deduction under sections 80C and 80D without showing or submitting a receipt. However, you should keep the receipts safe until your income tax return has been accepted by the income tax department. In the case of other tax-saving deductions, you may need to show receipts and other documents with your ITR.

There is no limit to the number of tax-exempt investments one can have in a financial portfolio. However, it is important to note that there is a limit to how useful any instrument can be for the purpose. This is because the amount of deduction that can be claimed for specific instruments is capped at a maximum value. At the same time, keep your financial portfolio balanced so that it also provides safety, returns and liquidity.

The maximum limit of investment that will reap the benefits of deduction from taxable income under Section 80C is Rs 1.5 lakh.

Investing in a health insurance plan for family and parents, and investing an additional Rs 50,000 into an NPS Tier-I account are a few ways you can save tax beyond Rs 1.5 lakhs. Other tax-saving options include buying or constructing a house with a home loan. You can claim an additional deduction of up to Rs 2 lakhs on the interest paid for the loan.

Apart from Section 80C, various deductions and exemptions has been provided under the provision of Income Tax Act, 1961 like deduction under section 80D can be claimed for the payment of health insurance, deduction upto Rs 50,000 on home loan interest under Section 80EE. Any donations you make to charitable institutions are also allowed as deduction under Section 80G, subject to condition prescribed therein.

You can easily lower your tax on income by investing in tax-saving investment plans. A few great tax saving options are ULIP and life insurance plans, NPS tier-I account, PPF, Senior Citizen Saving Scheme, etc.

This way, you can reduce the amount of your taxable income. Besides, you can claim deductions on your taxable income on account of expenses such as repayment of home loan principal, child’s education fee, expenses during home purchase etc. You should start learning about tax-saving options in India. Tax-saving investments and expenses can reduce your total tax liability every year.

You can reduce your tax liability to zero if you utilise the common tax saving investments and sections such as section 80C, 80D, 80CCD and 24B deductions to the limits. Additionally, complete deduction requires you to claim both 24B and HRA simultaneously. This is only possible if you are paying both rent and home loan EMIs. If you are in this situation, your tax liability can go down to zero.

First of all, make investment of Rs 1.5 lakh in investments instruments covered under Sections 80C to reduce your taxable income. Claim deductions for the interests paid on home loan and/or education loan if any. Get a health insurance policy and claim for other medical expenditure like preventive medical healthcare check-up, expenditure on rehabilitation of handicapped dependent relative, among others. Mainly, the idea should be finding out which tax saving avenues fit well with your larger financial goals and invest in them!

FD interest or fixed deposit interest income gets taxed as per the income slab rates of individual taxpayer. Banks or post offices deduct tax or TDS when the aggregate interest income on all fixed deposits exceeds Rs 40,000 per financial year. The limit is Rs 50,000 in case of senior citizens.

First of all, make use of the Rs 1.5 lakh deduction allowed under Section 80C. This can be done by making investments in life insurance premium, Equity Linked Saving Scheme (ELSS), Public Provident Fund (PPF), Unit Linked Insurance Plans (ULIPs), Sukanya Samriddhi Yojana, Senior citizens Savings scheme, National Pension Scheme (NPS), among others.

Second, make use of the deductions available in respect of health insurance and other medical expenses. Under Section 80D of the Income Tax Act, 1961, a deduction of up to Rs 25,000 is allowed in a year in terms of the premium paid towards a health insurance policy of Self and your family i.e., Spouse and children. This can include preventive healthcare check-ups too upto Rs 5000/-. Under section 80D you can also claim additional deduction upto Rs. 25000/- (Rs. 50000 in case of senior Citizen) for health insurance of your parents.

Recent Blogs

What is Gratuity? A Comprehensive Guide for Employees

31 July '26

2913 Views

12 minute read

Discover the essentials of gratuity, its importance for employees, and key insights. Learn more at Canara HSBC Life Insurance for a secure financial future.

Read More

Tax Saving

How to Save Income Tax in India: Best Tax Saving Options in 2026

31 July '26

1610 Views

10 minute read

Reduce your income tax legally with simple strategies for FY 25-26, Section 80C deductions, exemptions, and planning tips to maximise yearly tax savings.

Read More

Tax Saving

Is Education Loan Tax Free: Eligibility for Tax Deduction

31 July '26

2937 Views

7 minute read

Learn the tax benefits available for education loans under Section 80E of the Income Tax Act in India. Learn strategies to maximize your tax savings with simple rules.

Read More

Tax Saving

Best Method to Save Tax in India: Top Tax-Saving Methods for 2026

31 July '26

1912 Views

6 minute read

Explore the best tax-saving methods in India for the income group of 5-15 Lac, including deductions under Sections 80C, 80D, and more.

Read More

Tax Saving

Are You Overpaying Tax as a Salaried Individual? Find Out

31 July '26

1539 Views

7 minute read

Did you know salaried individuals often overpay tax without realising it? Discover common reasons & smart tips to avoid overpaying taxes in India.

Read More

Tax Saving

Complete Guide to File ITR for Salaried Employees in India

31 July '26

195 Views

5 minute read

A comprehensive ITR guide for salaried Employees for AY 2025-26. Learn about form selection, deductions, and simple steps for online filing.

Read More

Tax Saving

Can You Claim Tax Deduction if Life Insurance Premium Is Paid by Family?

31 July '26

1243 Views

6 minute read

Find out if you can still claim life insurance premium tax deductions when your premium is paid by a family member. Know the eligibility and rules under Section 80C.

Read More

Tax Saving

Achieving Tax Saving Goals through Tax Saving Investments

30 July '26

910 Views

4 minute read

Discover 3 key financial goals you can achieve with tax-saving investments. Learn how to save taxes while building wealth and securing your financial future.

Read More

Tax Saving

Old vs New Tax Regime: Things You Need to Know

30 July '26

6798 Views

10 minute read

Explore the new tax regime vs the old one and choose what suits you best. Learn key differences and gain valuable insights with Canara HSBC Life Insurance.

Read More

Tax Saving

Popular Searches

- Tax Planning

- Income Tax Calculator

- TDS Vs TCS

- Section 80C

- What Is ITR

- Tax Concepts

- Section 80D

- Section 24

- 80DDB

- What is MAT?

- ITR-3 Form

- Term Insurance Tax Benefit

- TDS for Professional Fees

- Income Tax Slab FY 2025-26

- HRA Calculator

- TDS on Rent

- What is Income Tax Return?

- Income Tax for NRI

- How to File Income Tax?

- Section 80C Tax Benefits

- Old vs New Tax Regime

- LTCG Tax on Investments

- Tax Saving Options for Salaried

- Income Tax Rebate under 87A