Written by : Knowledge Centre Team

2025-11-16

2906 Views

11 minutes read

Share

Managing your money is more than just saving or investing. It involves making smart choices that support your needs today and your goals for tomorrow. If you want to grow your wealth and secure your future, you must understand how portfolio management and financial planning work. This blog helps you explore both concepts, understand how they differ, and learn how to use them together to build a strong financial foundation for yourself and your loved ones.

Key Takeaways

|

Portfolio management means actively balancing risk with potential returns by choosing the right mix of assets that match your risk appetite.

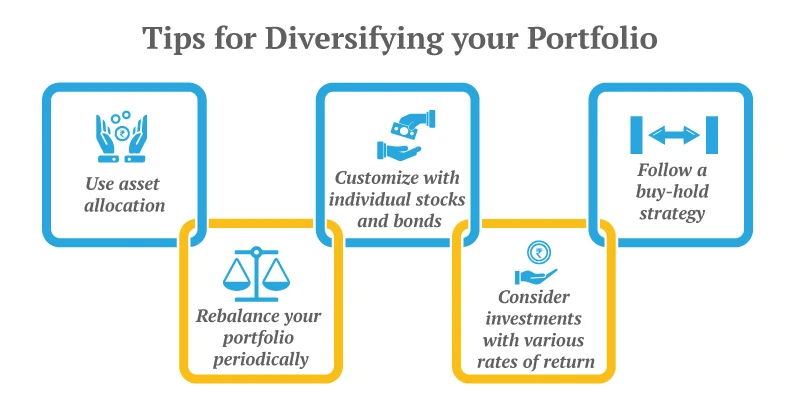

You may decide to manage your investments yourself or work with a professional portfolio manager. In both cases, success depends on how well you understand the essentials like choosing the right asset classes, diversifying smartly, and regularly reviewing and adjusting your investments.

For Example, Mr A is a 35-year-old working professional who wants to build wealth for his child’s education over the next 10 years. He invests 60% in equity mutual funds for high growth, 30% in debt instruments for stability, and 10% in gold for diversification. Every year, he reviews and rebalances his portfolio to maintain this mix.

Learn More - Ways of Portfolio Management in ULIPs

An OTP has been sent to your mobile number

Sorry ! No records Found

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Creating a balanced and diversified portfolio helps you meet your financial goals while reducing risks. With proper portfolio management, you can invest smarter, stay on track, and make your money seamlessly . Here are the key benefits:

Financial planning is the process of setting financial goals and building a structured approach to achieve them. It helps you understand where you stand today, what you want in the future, and how to bridge the gap using available financial tools. Financial planning can be your guide at every life stage, like saving for your child’s education, buying a house, or retiring early.

Example: Fatima, a 30-year-old working woman, started a financial plan with her advisor. She set a goal for early retirement and began saving systematically in mutual funds, while also investing in term insurance. Five years later, she had not only built wealth but also secured her future.

A financial plan is your roadmap to a secure and purposeful life. It helps you align your spending with your values, prepare for life’s surprises, and grow your wealth over time. Some of the key benefits are as follows:

Here’s your step-by-step retirement planning guide.

The difference between portfolio management and financial planning is as follows:

| Aspect | Portfolio Management | Financial Planning |

|---|---|---|

Purpose and Focus | Managing current investments for optimal returns and diversification | Setting long-term financial goals and creating strategies to achieve them |

Time Horizon | Focused on present or near-future asset performance | Oriented towards long-term milestones and security |

Professional Guidance | Typically involves an investment or portfolio manager | Guided by a financial advisor or planner |

Process Involved | Evaluating and adjusting investments to optimise returns and manage risk | Assessing income, expenses, savings, and devising a holistic financial roadmap |

Assessment Scope | Considers only investment assets | Encompasses overall financial health, including cash flow, insurance, taxes, etc. |

Dynamism | Highly dynamic, continuous monitoring and frequent adjustments | More stable and periodic review, mostly updated due to life changes |

Portfolio management helps you make smart investment choices in the present, while financial planning ensures your entire financial life is aligned with future goals.

If you want true financial freedom, you must combine both. Let your financial plan define your goals, and your portfolio strategy work to achieve them. With the right balance of planning and execution, you can confidently secure your present and build a future that matches your dreams.

Disclaimer - This article is issued in the general public interest and meant for general information purposes only. The views expressed in this blog are solely those of the writer and do not necessarily reflect the official policy or position of Canara HSBC Life Insurance Company Limited or any affiliated entity. We make no representations or warranties of any kind, express or implied, about the completeness, accuracy, reliability, suitability, or availability with respect to the blog or the information, products, services, or related graphics contained in the blog for any purpose. Any reliance you place on such information is therefore strictly at your own risk. You should consult with a qualified professional regarding your specific circumstances before taking any action based on the content provided herein.

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.