- Child Education Plan: A plan designed to help parents save systematically for their child’s future education expenses

- Premium Waiver Benefit: A feature where future premiums are waived if the policyholder dies or becomes disabled

- Maturity Benefit: The lump sum or payouts received at policy end to fund education, marriage, or milestones

- Child ULIP: A market-linked child plan offering life cover with investment in equity or debt funds

- Money-Back Child Plan: A child plan that provides periodic payouts along with life insurance coverage

- Education Inflation: The yearly rise in education costs due to increasing tuition fees, living expenses, and academic charges

Child Insurance Table of Content

0

1

1.

What is a Child Education Insurance Plan?

0

2

2.

Child Insurance - Top Selling Plans

0

3

3.

How Does a Child Insurance Plan Work?

0

4

4.

Secure Your Child’s Education and Future Milestones

0

5

5.

Types of Child Education Plans

0

6

6.

Why Do You Need to Buy a Child Education Plan?

0

7

7.

Features of Child Insurance Plans

0

8

8.

Benefits of a Child Education Plan

0

9

9.

Tax Benefits of Child Education Plans

10

10.

How Much Should You Invest in a Child Education Plan?

11

11.

Child Education Calculator

12

12.

Best Child Education Plans and Investment Options (2026)

13

13.

Top Government Schemes for Child Education

14

14.

How to Choose the Best Child Education Plan?

15

15.

What is Not Covered in a Child Insurance Plan?

16

16.

How to Buy a Child Insurance Plan?

17

17.

Benefits of Early Planning for Your Child’s Future

18

18.

Claim Process for Child Insurance Plans

19

19.

Glossary

20

20.

Frequently Asked Questions (FAQs) for Child Insurance Plans

21

21.

Related Blogs

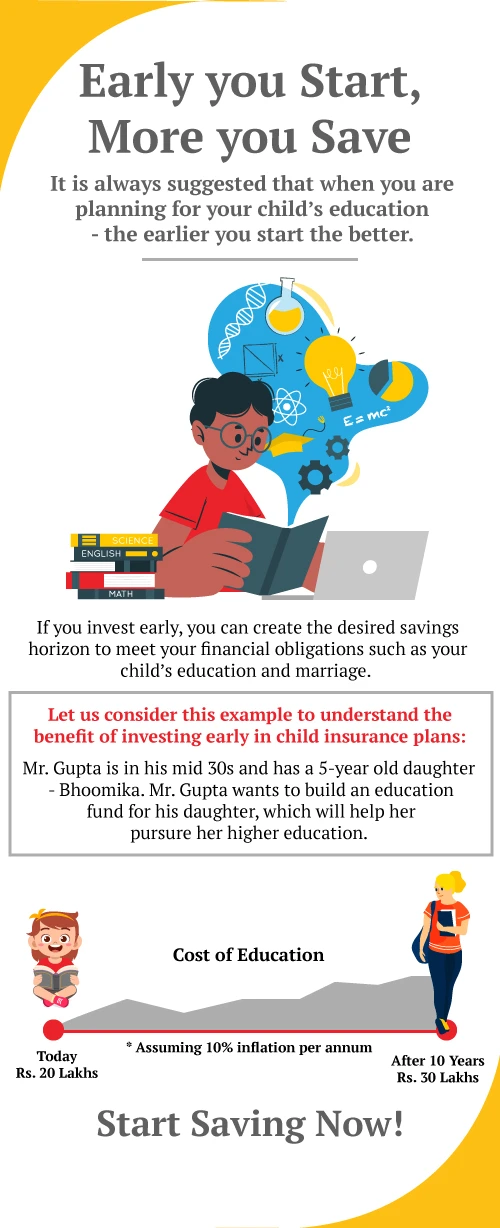

Planning for your child’s future is one of the most important responsibilities as a parent. From education to long-term life goals, financial needs grow over time. A child insurance plan helps you prepare for these expenses in a structured way while offering financial protection. In this blog, we explain how child insurance plans work, their types, benefits, and who should consider investing in them.

Key Takeaways

|

What is a Child Education Insurance Plan?

A child education insurance plan combines the features of a long-term investment option and life insurance. This combination offers financial safety to your child’s future through:

- Investment growth when you are alive and

- Insurance if you suffer a mishap on the way

Upon maturity, the child plan pays a lump sum amount, which can be used for the child’s higher education fees and marriage expenses. It offers the needed safety for a child’s future in case of your untimely demise or suffering a terminal illness.

While you are building the corpus to fulfil these goals for your child, the insurance plan provides a safety cushion to the corpus in case of your untimely demise. In the unfortunate event of your passing away before fulfilling the goal, the plan can invest the money on your behalf and give the maturity amount you originally aimed for your child.

We, at Canara HSBC Life Insurance, offer Child insurance plans that also offer periodic payouts of the corpus you have built to align with your child financial needs. These periodic payments can coincide with the crucial milestones of your child life, like education, marriage, etc.

Child Insurance - Top Selling Plans

We bring you a collection of popular Canara HSBC life insurance plans. Forget the dusty brochures and endless offline visits! Dive into the features of our top-selling online insurance plans and buy the one that meets your goals and requirements. You and your wallet will be thankful in the future as we brighten up your financial future with these plans.

Fixed Returns, Zero Risks & Worries

iSelect Guaranteed Future Plus

- 4 Plan options

- Life cover + Guaranteed benefits

- Accidental death benefit

- Premium protection cover

Don't Just Survive, Thrive

Guaranteed Assured INcome

- 3 Plan options

- Life cover + Guaranteed income

- Get Total Premiums at maturity

- Early income from 2nd policy year

Save, Dream, Plan. Live Peacefully

iSelect Guaranteed Future

- 5 Plan options

- Option to choose PPT

- Get Tax benefits

- Premium protection cover

How Does a Child Insurance Plan Work?

A child insurance plan helps you to secure the future of your child by ensuring that their goals are met even if you are not there.

Just like any other insurance plan, a child plan also requires you to pay regular premiums. The premiums you pay are allocated to your chosen funds in the child investment plan. You can choose various modes available to pay your premiums for the child policy. These are:

- Limited Pay: Pay for a limited time and enjoy the benefits of the policy

- Single Premium: Pay for a lump-sum premium for the whole policy at once.

- Regular Pay: Flexible payment schedules available on a monthly, quarterly, semi-annual, or annual basis.

For instance, Ajeet is starting to save for his 5-year-old daughter’s higher education and marriage. He plans to invest ₹ 10,000 monthly in a child savings plan with a life cover of ₹ 12 lakhs, for the next 15 years.

Case 1: If Ajeet survives the policy term

Ajeet will be entitled to receive the maturity benefit from the child savings plan. This is the fund value of the investments he has made into the child plan and any bonuses. Depending on the type of child insurance plan, Ajeet can either receive the lump sum or convert the sum into a regular payout.

Case 2: If Ajeet dies during the policy

If Ajeet does not survive the policy term, then his daughter will receive the death benefit. This will be higher than the sum assured or the fund value at the time of death. If Ajeet had opted for the premium protection benefit, the child investment plan would continue after paying the death benefit. His daughter will receive the maturity value upon the expiry of the plan.

Secure Your Child’s Education and Future Milestones

Enter OTP

An OTP has been sent to your mobile number

Didn’t receive OTP?

Application Status

Name

Date of Birth

Plan Name

Status

Unclaimed Amount of the Policyholder

Name of the policy holder

Policy No.

Address of the Policyholder as per records

Unclaimed Amount

Sorry! No records Found

Request Registered

Thank You for submitting the response, will get back with you.

Complaint Registered

. Please use this ID for all future communications regarding this concern.Request Registered

Thank You for submitting the response, will get back with you.

Thank you for your interest in our product. Our financial expert will connect with you shortly to help you choose the best plan.

Sorry

Types of Child Education Plans

A child education plan is a widely available financial product and most insurers offer it with different riders to appeal to a wide variety of customers.

- Child Endowment Plans: Child Endowment Plans offer a safe investment option for your money by offering guaranteed maturity benefits. These child investment plans are best when you know the amount that you will need for the goal.

Also, with guaranteed benefits and goal protection options, you can be sure to achieve your child's goal even if you are not around.

Child Endowment plans offer a savings avenue along with a life cover that ensures your financial goals are well-protected even in your absence.

- Child Money-back Plans: Child money-back plans offer a long-term, safe investment option for your child’s future. These plans are ideal for long-term financial goals, such as funding a four-year undergraduate degree.

Child Money-back plans also offer bonuses to aid the growth of your investment. These bonuses add to your plan’s maturity value.

These are some of the best child plans, as you enjoy the benefit of a life cover while getting a portion of the sum assured at regular intervals.

- Child Savings Plan: Child savings plans are generally ULIPs that give you more freedom as an investor. You can choose the amount of risk you want to take on the invested money. You can also use one or more automated portfolio strategies to benefit from market movements.

Some child plans also offer additional bonuses for long-term investors. You can withdraw money from the accumulated corpus after completing five policy years. Withdrawals are tax-free, so you can at any time after the lock-in period. Guaranteed Return Child Plans: Guaranteed return child plans offer a stable and low-risk way to build a corpus for your child’s future goals. These plans provide assured maturity benefits, so you know exactly how much you will receive at the end of the policy term, making financial planning more predictable.

Along with guaranteed returns, these plans also include life cover, ensuring your child’s goals remain protected even in your absence. They are ideal for parents who prefer certainty and disciplined savings over market-linked investments while securing their child’s future.

Why Do You Need to Buy a Child Education Plan?

A child education plan is an investment option designed to serve as a wallet for major life goals of a child. Be it higher education, hobby, or marriage a child insurance plan gives you the benefit of investing, growing and using your money as per your child’s needs.

One key reason to start early is rising education inflation. In India, education costs are growing at around 8-12% annually, meaning a ₹10 lakh course today could cost ₹25 lakh or more in the next 10-12 years.

This is where compounding makes a difference. For instance, investing ₹5,000 monthly at 10% returns can grow to around ₹10-12 lakh in 10 years, reducing future financial stress.

If you mean to provide for your child education goals the plans can work as child education insurance. The plan will help your child achieve the goal even if you cannot be there.

A few more important reasons to get a child insurance plan at the earliest are:

- Beat the inflation in higher education costs with investment as per your risk appetite using automated portfolio management options

- Prepare for an unexpected expense with an additional corpus for your child’s goal with bonuses and additional units

- Stop the unfortunate events like death and disability from harming your child’s future and plans

- Face financial emergencies or change of plans with partial withdrawal and loan facility from the plan

- Keep your child’s investment corpus safe from taxes with tax savings while investing and withdrawals

Features of Child Insurance Plans

Child insurance plans are designed to combine financial protection with long-term savings to support your child’s future goals. They offer structured benefits and flexibility to help parents plan confidently for key milestones.

Life Cover: Life cover is an integral part of most investment plans. A child saving plan also includes a cover on the life of the policyholder. This will protect the child’s dream in case anything happens to the policyholder during the term of the child's policy.

Goal Protection in Case of Death or Disability: The child investment plan will continue to invest the due premiums in your child’s goal after your untimely demise. This option ensures that your child can achieve their goal even after your death without having to pay any extra premiums.

Systematic Withdrawals: Child education plan and endowment plans offer the option of systematic withdrawal or automatic payments from the plan in the final few policy years. This allows your child to meet the financial needs which may arise gradually.

Bonus Additions: Participating child plans and Unit-Linked Plans offer rewards for staying invested for the long term. While ULIP will add units as loyalty additions and wealth boosters, endowment and money-back child plans accrue annual bonuses. These bonuses are payable with the maturity value of the child's policy.

Loans & Partial Withdrawals: Child endowment and money-back plans acquire cash value after two years of investment. Thus, in case of emergencies, you can take a loan against the policy without having to discontinue the policy. Child ULIPs, on the other hand, offer partial withdrawals after the five-year lock-in period.

Riders: Child insurance plans come with a variety of riders. The most prominent add-ons offered with child investment plans are critical illness cover, accidental death cover and the premium waiver option. Some insurers offer the premium waiver option as an in-built feature of the child policy. The critical illness cover protects against a set of terminal diseases, while the accidental death cover provides an additional sum in case of accidental death.

Choice of Funds: A part of the premium paid for a child insurance policy is invested in market-linked assets. The insurance company provides the policyholder with an option to choose from different funds. The funds under the child saving plan invest in equity, debt or money market instruments.

Premium Waiver Benefit: An important feature of a child insurance plan is the premium waiver benefit. In case the policyholder dies within the stipulated duration, the beneficiary gets the sum assured, and the insurance company continues to pay the remaining premiums till the maturity date.

Lump Sum Benefit: After your death, the death benefit is provided in a lump sum, i.e., the whole amount in a single payment.

Benefits of a Child Education Plan

Buying the right child education plan helps you build a secure financial foundation for your child while protecting their future against uncertainties. It ensures that important goals remain achievable through disciplined savings and long-term planning.

Corpus for Child's Education

The schools and the education system have been getting more and more advanced. Due to this, their fees are constantly rising. For higher education, the cost is even higher. So, it becomes important to plan the education of your child, keeping in mind the future costs.

That’s where a child education plan can help you. The premiums you pay over time are invested and can help create a corpus that will be sufficient to meet your child’s education goals, such as post-graduation and studying abroad.

Takes Care of your Child’s Medical Expenses

The primary focus of a child's insurance policy is to safeguard your child's future. But this is not the only way a child investment plan can help you.

It allows you to withdraw from your corpus from the child plan only after five years of starting the investment. The withdrawals are tax-free.

Financial Support to the Child in the Absence of a Parent

Even if you think that you will have enough to fulfil your child goals, life is unpredictable, and preparation is better. You can ensure that your child goals are financially protected, even if you are not there.

Child education plans come with life cover and premium protection. Your family is provided with a lump sum death benefit. Also, the premium protection feature of the best child investment plan ensures that your family doesn’t worry about the premiums, as they will be waived off and paid by the company.

Income Protection Cover for the Child

Lump-sum money will help you take care of the larger expenses. But other regular expenses happen more frequently. When you die, your income also stops. This can affect your family even more when you are the only breadwinner for the family.

Many child insurance plans offer regular payouts as well. After your death, your child will receive a monthly sum. This can help replace your income and make sure your child doesn’t suffer.

Acts as Collateral for Higher Education

Child insurance plans are an asset with a value which continues to increase until maturity. You can also use your child policies, especially child endowment plans, as collateral for a low-cost loan. This will help you secure a loan for your child for his education or even for their marriage later on.

Modification in Sum Assured

Some insurers allow the insured to increase the sum assured mid-way through the policy term without any change in the premium. Adjusting the sum assured of your child's investment plan as per your life stages and financial milestones can help you stay aligned with your goals.

Returns that can Beat Inflation

Child investment plans that we offer have portfolio investment options. You can invest in diversified portfolios of equity and debt securities through these plans.

Thus, your investments in a child plan can earn inflation-beating returns through market securities over the long investment period.

Tax Benefits of Child Education Plans

Child education plans not only help you build a corpus for your child’s future but also offer valuable tax benefits under the Income Tax Act, 2025.

Section 123 (previously known as Section 80C): Premiums paid towards a child education plan are eligible for tax deduction of up to ₹1.5 lakh per financial year, subject to specified conditions. This helps reduce your taxable income while you invest for your child’s goals.

Schedule II (Table S.No. 2) (previously known as Section 10(10D)): The maturity benefits received from the plan are tax-free, provided the annual premium does not exceed:

₹2.5 lakh for ULIP-based child plans

₹5 lakh for non-ULIP child plans

Additionally, the death benefit paid to the nominee is also fully tax-exempt, ensuring complete financial security. These tax benefits apply throughout the policy tenure, making child education plans a tax-efficient way to secure your child’s future while saving on taxes.

How Much Should You Invest in a Child Education Plan?

Before buying a child education plan, you must be sure of how much you should invest. Education, as we know, is getting costlier with each passing year. School fees are rising constantly. Also, if you want your child to go for higher education in the field of engineering or medicine, etc. then the cost is even higher.

Thus, to make sure your child can pursue what they want, your income may not be enough, and you need to invest in a child education plan as well. But how much should you invest?

Well, this depends on the educational course and institution you are targeting. You can plan your monthly savings into the child education plan accordingly.

Here are the steps you should follow to know how much to invest:

- Ascertain the goal you want to achieve

- Estimate the inflation rate at the time the child will attain education age

- Estimate the expected rate of return of the policy.

Education is one area with one of the highest inflation rates. Thus, it becomes even more important to plan for your child’s education as early as you can.

Child Education Calculator

A smart online tool that helps you easily navigate the costs of your child's future education, ensuring their dreams come true.

1

About my Child

2

My Child’s Dream and Needs

3

Additional Details

4

Our Recommendation

About my Child

My Child’s Dream and Needs

Additional Details

Our Recommendation

For example, suppose, you are planning for an MBA for your child, 10-15 years from now. Here’s what your child saving plan can look like:

Education Stage | Current Cost | Cost in 5 Years | Cost in 10 Years |

Primary Education (per annum) | ₹1.5 Lakhs | ₹2.4 Lakhs | ₹3.9 Lakhs |

Undergraduate (BBA/BCom/Law) | ₹8 Lakhs | ₹12.9 Lakhs | ₹20.8 Lakhs |

BTech (Private College) | ₹12 Lakhs | ₹19.3 Lakhs | ₹31.1 Lakhs |

MBA (Top Indian Institutions) | ₹25 Lakhs | ₹40.3 Lakhs | ₹64.8 Lakhs |

MBA Overseas | ₹80 Lakhs | ₹1.29 Crore | ₹2.07 Crore |

*Assuming an inflation rate of 10% p.a. for education costs.

Best Child Education Plans and Investment Options (2026)

Planning for your child’s education requires a mix of safety, growth, and flexibility. In 2026, parents can choose from a range of options, some of which offer guaranteed returns, while others provide market-linked growth. Selecting the right mix depends on your risk appetite, time horizon, and financial goals.

Here’s a quick comparison of some of the most popular options:

Investment Option | Lock-in Period | Returns | Tax Benefits | Ideal For |

5 years | Market-linked (varies) | Up to ₹1.5 lakh under Sec 123 (previously known as Section 80C); maturity tax-free under Schedule II (Table S.No. 2) (previously known as Section 10(10D)) | Parents seeking growth + life cover | |

Endowment Plan | ~2 years (policy term-based) | Stable/guaranteed + bonuses | Sec 123 + Schedule II (Table S.No. 2) | Low-risk investors wanting assured returns |

Sukanya Samriddhi Yojana (SSY) | Till age 21 / marriage | 8.2% p.a. (govt-backed) | Sec 123 + tax-free maturity | Girl child-specific long-term savings |

PPF (Public Provident Fund) | 15 years | 7–8% p.a. (govt-backed) | EEE (Exempt-Exempt-Exempt) | Safe, long-term wealth building |

Mutual Funds | No lock-in (except ELSS) | Market-linked | ELSS is eligible under Sec 123 | High-growth potential with flexibility |

Top Government Schemes for Child Education

Government-backed schemes are a reliable choice for parents looking to build a secure education fund with stable returns and tax benefits. These options focus on disciplined, long-term savings with minimal risk.

- Sukanya Samriddhi Yojana (SSY): This scheme is designed specifically for the girl child and offers attractive returns of around 8.2% per annum. It has a lock-in period until the child turns 21 years (or marriage after 18). Investments qualify for tax benefits under Section 123, and the maturity amount is tax-free. Ideal for long-term, secure savings for a daughter’s education and future.

- Public Provident Fund (PPF): PPF is a government-backed scheme available for any child, offering returns of around 7.1% per annum. It comes with a 15-year lock-in period and follows the EEE (Exempt-Exempt-Exempt) tax structure, making it highly tax-efficient. Ideal for parents seeking safe and consistent long-term growth.

- National Savings Certificate (NSC): NSC is a fixed-income investment option available for any child, offering returns of approximately 7.7% per annum. It has a 5-year lock-in period and provides tax deductions under Section 123. Ideal for medium-term goals with assured returns.

Scheme | Eligibility | Returns | Lock-in Period | Tax Benefits |

Sukanya Samriddhi Yojana (SSY) | Girl child | ~8.2% p.a. | 21 years (or marriage after 18) | Eligible under Section 123 |

Public Provident Fund (PPF) | Any child | ~7.1% p.a. | 15 years | Eligible under Section 123 (EEE benefit) |

National Savings Certificate (NSC) | Any child | ~7.7% p.a. | 5 years | Eligible under Section 123 |

How to Choose the Best Child Education Plan?

The best child education plan for you should be the one that can solve your purpose in the most optimal way possible. Some factors should be considered before you decide to buy a child plan.

Start Investing Early: Starting early gives your child savings plan ample time to grow your money. You also get more time to make adjustments and achieve a bigger goal than you initially intended.

Consider Inflation & High Education Cost: Inflation keeps raising the cost of your child’s future goals. However, planning your child plan investments with after-inflation costs would let you catch up to it in the long run.

Look for Premium Waiver Benefit: The premium waiver benefit allows your child's investment plan to continue without the need for additional premiums. This option comes into force if you suffer from a critical illness or accidental disability which affects your income. Such emergencies do not allow for death benefits, but they can affect your plans. However, with the premium waiver benefit, you can rest easy, as the child will receive the intended maturity value.

Consider the Premium Protection Option: If this feature is available in the plan, then the premiums will be taken care of even after you die. The company funds all the premiums that remain to be paid after your death under this option. Thus, the policy continues even after your death, and your child will get the maturity benefit as promised by the company.

This feature ensures your family does not have to worry about the premiums.Check for Partial Withdrawal Option: A partial withdrawal facility allows you to withdraw money from your fund. This comes in handy in times of emergencies when you are in need of quick cash. You should look for a policy that provides you with the option of partial withdrawals.

Option to Add Riders: Riders are the additional benefits offered over and above the policy, which enhance the scope of your existing policy. Riders cover those things that are not covered by the base policy. Some of the most popular riders include the following:

Critical illness rider

Accidental total & permanent disability rider

Though some riders are added by default in some policies, some add to the cost of your premium. You should choose the policy with the most available rider options to get the best from your policy.

Frequency of Premium Payment: There should be multiple options to pay your premium. You must be able to pay as you like. Many policies have the option of limited payment. This means you pay your premiums for a limited time and enjoy the benefits of the policy for a long time.

Check for Regular Payout Option: The purpose of the child insurance policy is to provide your child with the money, which will help in their education or other goals. This money should be present when needed.

Consider the Associated Charges in the Policy: This is also an essential factor to consider before buying a policy. The insurance provider levies charges for the maintenance of the policy. Some of the charges associated are:

Fund management charges

Premium allocation charges

Administration charges

Switching charges

Choose the policy that has the lowest charges involved.

- Terms & Conditions of the Child Insurance Policy: Understanding the benefits and exclusions of your child's policy allows you to ensure that the policy will be useful in every situation. For example, how much is the regular payment from the plan, which events are covered under the policy, etc?

What is Not Covered in a Child Insurance Plan?

There are certain things in the child insurance policy that are excluded from the policy. This means that these things are not covered, and the insurance company will not provide any benefit if death is due to anything that is excluded.

Suicide Exclusion: If the death is due to suicide or self-harm. If the death is due to suicide within 12 months of the commencement of the policy, then 80% of the premium paid or surrender value is paid.

Death Due To Drug Overdose: If you die due to the consumption of drugs that are not prescribed or excessive intake of alcohol, then no death benefit is payable.

Death Due to War: If you die due to war (declared or not) or any type of civil commotion, your family will not receive the death benefit.

Hazardous Activities: There are certain adventure sports that pose a risk to life, such as sky diving, mountaineering, scuba diving, etc. If you die due to participating in these games, then your coverage ceases to exist.

Taking Part in Criminal Activity: If you die while indulging in any activity that is considered criminal or illegal, then this will also not be covered in your child insurance plan.

How to Buy a Child Insurance Plan?

Buying a child insurance plan is a crucial financial decision that ensures your child’s future is secure, even in your absence. It requires thorough research and careful planning to select a policy that aligns with your long-term goals. Here’s a step-by-step guide to help you make an informed choice:

- Assess Your Financial Goals: Before selecting a plan, determine the financial milestones you want to secure for your child. Common goals include funding their higher education, covering medical emergencies, and ensuring financial stability in case of unforeseen circumstances. Estimate the future costs of these expenses, considering inflation, to get a realistic idea of how much coverage you need.

- Compare Different Plans: Child insurance plans come in various types, including traditional endowment plans, unit-linked insurance plans (ULIPs), and money-back policies. Compare policies based on:

- Coverage: Look at what financial risks are covered, including death benefits and maturity benefits.

- Premiums: Assess affordability and premium payment flexibility (monthly, quarterly, or annually).

- Maturity Benefits: Check how and when the policy pays out benefits, such as lump sums or periodic payouts.

- Waiver of Premium: Choose a plan that continues even if the policyholder (parent) passes away, ensuring the child still receives the benefits.

- Consider Flexibility and Investment Options: Some child insurance plans offer investment components that help grow your savings over time. Plans like ULIPs allow you to invest in equity or debt funds based on your risk appetite, while traditional plans provide guaranteed returns. Select a plan that offers flexibility in terms of switching funds, withdrawing funds when needed, and modifying coverage as per changing needs.

- Understand the Policy Terms and Exclusions: Before making a purchase, read the policy documents carefully to understand all terms and conditions. Pay special attention to exclusions, waiting periods, and conditions for claim settlements. This will help you avoid surprises in the future.

- Consult a Financial Advisor: If you are unsure which plan is best for your needs, seek professional advice. A financial advisor can help you assess different policies, compare investment returns, and choose the most suitable plan based on your financial situation and future goals.

- Finalise and Purchase the Policy: Once you have selected the right child insurance plan, complete the paperwork and ensure all details are accurate. Keep a copy of the policy documents and inform a trusted family member about it to facilitate easy access when needed.

By following these steps, you can select a child insurance plan that provides financial protection and security for your child, ensuring their dreams and aspirations are never compromised.

Benefits of Early Planning for Your Child’s Future

Starting early ensures greater financial stability for your child’s future. By investing in child insurance plans, education savings schemes, and other long-term financial instruments, you can build a strong financial foundation. Early planning provides higher returns, better investment options, and protection against unforeseen circumstances.

- More Savings Over Time: The earlier you start, the more you can save through compounding benefits and disciplined investments. Early investments allow you to accumulate a significant corpus over time, reducing financial burdens in the future.

- Increased Investment Options and Flexibility: Starting early provides access to a wider range of investment options, from mutual funds to unit-linked insurance plans (ULIPs). It also gives you the flexibility to adjust investments based on market conditions and changing financial goals.

- Secures Your Child’s Future and Reduces Your Stress: A well-planned financial strategy ensures your child’s future needs, such as higher education and healthcare, are covered. This proactive approach reduces financial stress and gives you peace of mind, knowing your child’s future is protected.

Claim Process for Child Insurance Plans

Understanding the claim process ensures that your family can access financial support quickly and without confusion during difficult times. Most insurers follow a simple and structured process to settle claims efficiently.

- Notify the Insurer: The first step is to inform the insurance company about the claim as soon as possible. This can usually be done online, through customer care, or by visiting a branch.

- Fill the Claim Form: Next, the nominee needs to fill out the claim form with accurate details such as policy information, cause of claim, and personal details.

- Attach Required Documents: Submit all necessary documents along with the form, including:

- Duly filled claim form

- Policy document

- Death certificate (if applicable)

- Identity and address proof of the nominee

- Submit the Claim: Once the documents are ready, submit the claim request either online or at the nearest branch of the insurer.

- Verification and Payout: The insurer will verify the details and documents submitted. Upon successful verification, the claim amount is disbursed to the nominee as per the chosen payout option (lump sum or income).

Glossary

Frequently Asked Questions (FAQs) for Child Insurance Plans

A child education plan is an insurance plan for and an investment asset to meet their educational goals. A small part of the child education plan is used to provide the financial security of insurance, while a bigger part is invested in market-linked instruments. This combination of insurance and market-linked portfolio investments ensures adequate safety for your child’s future.

Any parent with a child between 0 and 15 years should buy a child insurance plan. It gives inflation-beating returns for various needs of the child as they grow up. As a child grows up, their financial needs increase substantially.

Child plans are meant to build a financial buffer for your child’s future needs, so, it is important to have a fail-proof plan. A few things to consider while buying child plans are:

- Goal: It is pertinent to have a clear goal in mind as it determines the type and tenure of the policy. You should invest in a child plan as soon as the child is born. Starting early gives your investment a chance to grow and helps you prepare better for your child’s needs. Similarly, selecting a long-term policy protects your child for a longer term.

- Premium waiver: While buying a child plan, it is mandatory to check if the premium waiver facility is available or not. Not having a premium waiver option can leave your child vulnerable in your absence.

- Inflation: When you are investing for the long term, external factors like inflation cannot be ignored. Invest in ULIPs to generate inflation-beating returns.

- Bonus component: Along with the basic benefits of a child plan, insurance companies also offer additional benefits. Even though these benefits are small, they could add considerable value in the long run.

Eligibility for a child education plan varies by insurer. Typically, the parent must be 18 to 65 years old, with flexible maturity based on the chosen term. Generally, the maximum age of a child to buy a child plan may go up to 18-25 years of age, depending on the company's policies. Premiums often start from ₹5,000 per month or ₹50,000 per year, and policy tenures usually range from 5 to 30 years.

You need the following:

- Policy Form: Contains policy details.

- Proof of Address: Government-issued document (e.g., passport, Aadhaar).

- Proof of Income: Income verification.

- Proof of Identity: Government-issued document (e.g., PAN card, Aadhaar).

- Proof of Age: Birth certificate or educational documents.

Tax-Deductible Investment: Child insurance and education plans are life insurance plans. Thus, the money you invest in these plans is deductible from your taxable income under Section 123 (previously known as section 80C of the Income Tax Act. Every year you can claim a deduction of up to ₹1.5 lakhs by investing in these plans.

Tax-Exempt Partial Withdrawals: After the respective lock-in periods (for different types of child insurance plans) the ULIPs may allow partial withdrawals while other plans acquire cash value. So, in case of an emergency, you can withdraw money from the child plan without stopping your investment. Also, any payments made by the plan before maturity, as in endowment and moneyback child plans, are exempt from tax.

Tax-Free Maturity Value: Maturity proceeds from child education plans are also tax-free under Schedule II (Table S.No. 2) of the Income Tax Act, 2025. Only two of the following conditions may apply after the Union Budget of 2021:

The annual investment should not exceed 10% of the life cover in the plan

In the case of the ULIP child plan, the total investment (including other ULIPs) should not exceed ₹2.5 lakhs in a year (only applicable to plans starting after 1st Feb 2021)

While the cost of insurance depends on a host of factors such as tenure, coverage and the mode of payment. You can use the ‘child education planning calculator’ to get an idea of the cost of child education plans. The amount you will need to invest in your child’s education now depends on your child’s current age, the targeted institution and course fees. Also, before you start investing, make sure to account for inflation in the higher education costs. For example, if you intend

The right time to buy child plans depends on the financial goal and the type of policy. Child insurance policies are long-term instruments and to generate decent returns it is advisable to invest as early as possible. You can invest in child insurance policies even before the child is born. Child education policies are relatively short-term policies. Child education policies can be chosen according to the financial goal. You can invest in child education policy as soon as the child is born if you plan to fund their primary and secondary education through the policy. If the aim is to accumulate funds for the higher education of the child, then you can invest at a later stage. In any case, it is not advisable to invest after the child has turned 15.

A child insurance plan is the best investment option to provide for your child’s future under every circumstance. Child investment plans can offer you a market-linked return on investment along with a safety umbrella of a life insurance cover. Thus, they are the best investment modes to invest in your child’s higher education and marriage goals.

One of the defining features of child education policies is the partial withdrawal facility. Most insurance companies allow partial withdrawal from child education plans to take care of liquidity needs.

The policy for premature closure of the child education plan deposit differs from insurer to insurer. Some insurers allow premature closure of the child education plan deposit. If the account is closed before the lock-in period expires, the fund’s value minus the surrender charges id deposited in the discontinued policy fund. The amount earns a minimum of 4% interest and will be paid to you after the lock-in period is over. If the policy is surrendered after the lock-in period, the total fund value minus the surrender charges will be given to you. However, prematurely closing the child education plan can involve financial risks and may prevent you from achieving your intended goal.

If you have opted for the premium protection option, your policy will pay the minimum guaranteed sum assured to the nominees upon your death. But the investments in the policy will continue, where the insurer will bear all remaining future premiums.

However, if you have not opted for the premium protection benefit, the policy will pay the higher sum assured or the fund value upon your death. The policy terminates after paying the benefit.

5 Key Features of Top Child Plans in India 2026

28 July '26

8900 Views

7 minute read

Discover 5 must-have features in a child plan. Guaranteed education fund, flexibility, safety cover, growth options and tax benefits for smart planning.

Read More

Child Plan

Planning Your First Child: Financial Steps to Prepare in 2026

28 July '26

910 Views

8 minute read

Learn how to plan for your first child by preparing finances, managing expenses, choosing insurance and building savings for a secure future.

Read More

Child Plan

Why Child Education Plans Are Important for Long-Term Planning?

28 July '26

1023 Views

7 minute read

Reasons child education plans are considered important, covering rising education costs, financial preparedness, and structured long-term planning.

Read More

Child Plan

Sukanya Samriddhi Yojana 2026: Interest Rate, Calculator & Benefits

28 July '26

6889 Views

15 minute read

Check latest SSY interest rates, eligibility, tax benefits, maturity amount & Sukanya Samriddhi calculator for 2026.

Read More

Child Plan

How to Plan an Education Fund for Your Child?

28 July '26

1178 Views

10 minute read

Practical guidance on planning an education fund for your child, including savings methods, investment options, and future education cost planning.

Read More

Child Plan

Using Whole Life Insurance to Secure Your Child’s Future

28 July '26

2216 Views

12 minute read

Learn how whole life insurance helps secure your child’s future by offering lifelong coverage, financial stability and long-term support for education and goals.

Read More

Child Plan

Benefits of Investing in a Child Insurance Plan in 2026

28 July '26

3567 Views

7 minute read

Discover why a child insurance plan is essential. Learn how it offers investment growth, premium waivers, tax benefits, and financial protection for you.

Read More

Child Plan

4 Reasons You Should You Buy a Savings Plan for Your Child?

28 July '26

1113 Views

8 minute read

Explore 4 compelling reasons to invest in a child savings plan. Long-term financial security, education funding, tax benefits, and peace of mind for your child’s future.

Read More

Child Plan

What is a Child Education Insurance Plan?

28 July '26

1202 Views

8 minute read

Child education insurance plans secure your child’s learning and future. Discover why it is essential, how it works, and tips to choose the best policy.

Read More

Child Plan

Popular Searches

- Child Education

- Child Insurance Plan

- Children Money Back Policy

- Insurance Policy For Newborn

- Child Protection Rider

- How Child Insurance Works?

- Sukanya Samriddhi Yojana

- Child Insurance Calculator

- Buy Best Child insurance Plan

- Best Investment Plan for Girl Child

- Child Education Insurance Plan

- Best Fixed Deposit for Child

- Types of Child Insurance

- Child Education Insurance